DRT Allows SBI To Sell Hypothecated Car Over Loan Default

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

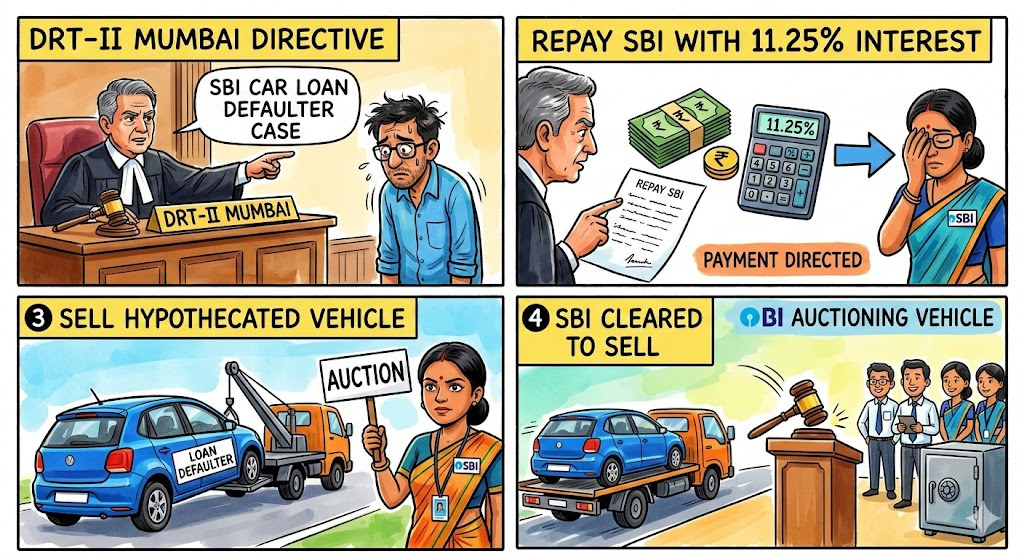

DRT-II, Mumbai has directed a car loan defaulter to repay SBI with 11.25% interest, and cleared the bank to sell the hypothecated vehicle.

What Is The Issue?

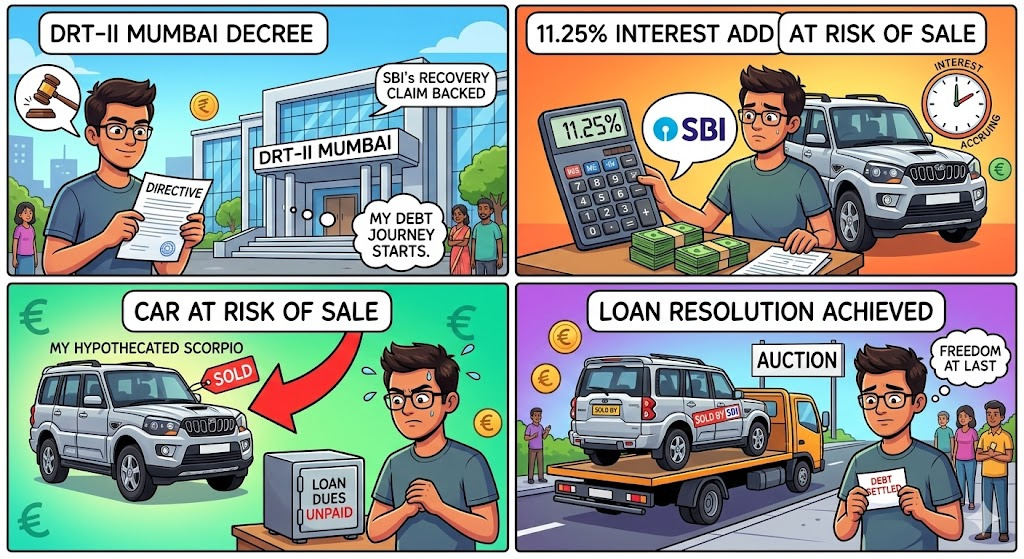

A repayment default in an SBI-linked car loan has ended in a recovery order from the Debts Recovery Tribunal (DRT)-II, Mumbai. The loan, originally sanctioned by the erstwhile State Bank of Bikaner and Jaipur (later merged with SBI), was backed by a hypothecated Mahindra Scorpio EX 9-seater.

The borrower, Nityanand Pawaskar, allegedly stopped servicing EMIs, and the account was classified as NPA on 01/01/2013. SBI approached the Tribunal to recover outstanding dues and enforce its security over the vehicle.

Key Ruling And What It Means For Borrowers

Read More : Shriram Finance Car Loan Interest Rate

DRT-II, Mumbai (Presiding Officer Harish Kumar Kaushik) allowed SBI’s recovery claim and ordered repayment of ₹10,74,796 (amount stated as due as on 04/03/2014) along with future simple interest at 11.25% per annum from 24/03/2014 (filing date) till realisation, plus costs.

It also backed SBI’s right to sell the hypothecated vehicle if the borrower fails to redeem it as per law. A Recovery Certificate was directed to be issued for execution before the Recovery Officer.

Before the timeline, here is the case in numbers and dates.

These figures set the base for enforcement, because the Tribunal treated the vehicle as security for the adjudicated sum.

What The Tribunal Order Says?

SBI’s case was that the borrower availed the car loan and executed loan and security documents, including the loan-cum-hypothecation agreement and EMI debit authorisation. The bank said the instalments were not paid as agreed, leading to classification of the account as NPA on 01/01/2013.

The Tribunal noted that despite service, the borrower did not appear and was proceeded ex parte. With the bank’s evidence remaining unrebutted, DRT-II ordered repayment and permitted recovery through sale of the hypothecated vehicle if dues are not cleared through lawful redemption. The Recovery Certificate direction strengthens the execution route, since it allows the Recovery Officer to act for recovery under the Tribunal’s mechanism.

How The Story Developed Earlier

The case facts track back to the sanction on 22/12/2011, when ₹10,00,000 was approved at a floating 11.5% rate, to be repaid across 84 EMIs of ₹17,387 beginning Jan 2012. The vehicle, a Mahindra Scorpio EX 9-seater, was hypothecated to the bank as security.

After the NPA date of 01/01/2013, SBI quantified dues at ₹10,74,796 as on 04/03/2014 and filed the recovery application on 24/03/2014, seeking future interest at 11.25% per annum. The Tribunal’s final direction broadly matches the claim in the report: repayment of the stated amount with future simple interest at 11.25% and permission to sell the hypothecated vehicle if the borrower fails to redeem it.

Also Read : 7.45% Se Car Loan? Reality Check

This DRT order comes at a time when hypothecation linked paperwork is already under spotlight. Separate reporting has highlighted the government’s move to make hypothecation removal on RCs more seamless once a loan is fully repaid, signalling tighter system-level handling of lender liens and closures.

LoansJagat has also flagged the borrower-side pain point, noting that even after loan closure, hypothecation can continue to show on the RC unless the prescribed removal process is completed, which can affect resale and ownership clarity.

A quick view of the practical outcomes is below.

For borrowers, it is a reminder that a secured vehicle can be proceeded against once default is established and recovery steps are triggered.

What Stakeholders Are Saying?

SBI’s stand, as recorded in reports, was straightforward: dues were outstanding, the account had turned irregular, and the bank sought recovery with 11.25% future interest along with enforcement of the hypothecated security.

The borrower’s viewpoint did not come on record in the Tribunal proceedings cited, as the respondent did not appear and the case proceeded ex parte.

From the consumer side, LoansJagat’s reporting around hypothecation removal stresses that the lender’s lien remains visible on RC records until the closure and termination workflow is completed, which is why enforcement risk stays real when dues are unresolved.

Conclusion

DRT-II, Mumbai has backed SBI’s recovery claim with 11.25% interest and allowed sale of the hypothecated Mahindra Scorpio if dues remain unpaid.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article