By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

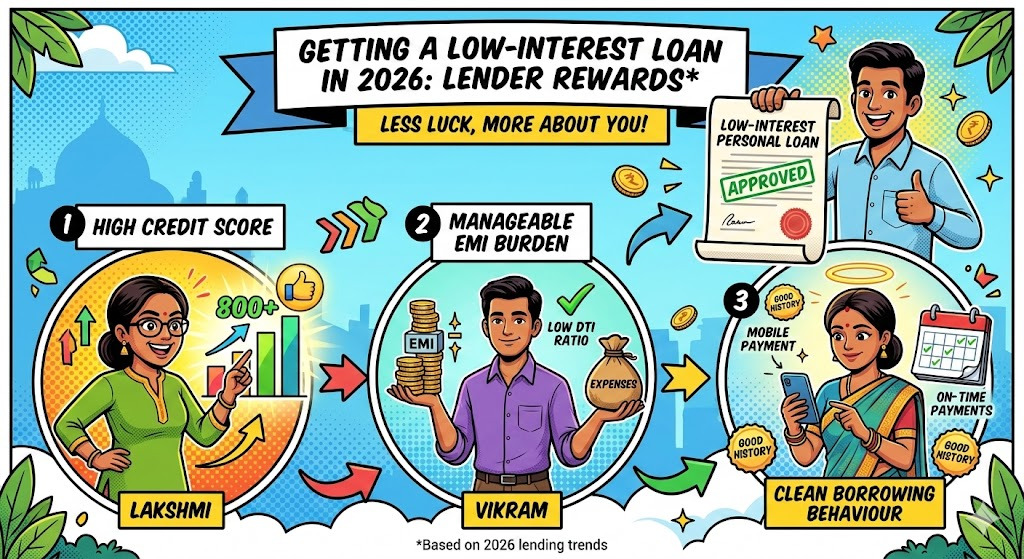

Getting a low-interest personal loan in 2026 is less about luck and more about credit score, EMI burden and clean borrowing behaviour that lenders reward consistently.

Personal loans are quick, unsecured and widely available, but rates in 2026 continue to swing sharply from borrower to borrower. Lenders price these loans on risk, so a small slip like high card utilisation, too many recent enquiries, or heavy existing EMIs can move an applicant out of the best slab.

The Economic Times, in an update dated 02 May 2025, lists credit score, loan amount, income stability and broader market conditions as key factors behind personal-loan pricing.

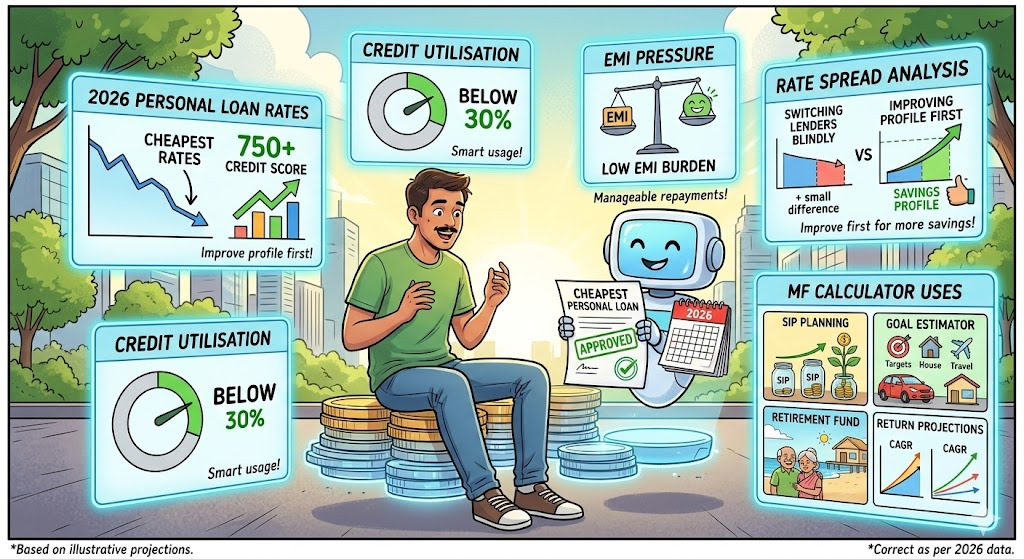

Across banks and NBFCs, borrowers typically lose the best offers due to 3 repeat issues: credit score below the “preferred” band, high utilisation on credit cards, and repayment stress from existing EMIs. Mint’s credit-profile guide published 29 Dec 2025 calls out keeping credit utilisation below 30% and paying all EMIs on time as basics for a stronger profile.

Another Mint piece updated 18 Sept 2025 repeats the same threshold and adds spacing out new applications by a few months to avoid repeated enquiries.

Read More : How to Calculate Interest Rate on Loan?

Separately, The Economic Times article dated 03 Apr 2025 also flags stable income and reduced debt as practical ways to improve eligibility and terms.

For borrowers chasing the lowest personal-loan rate, the immediate playbook is clear: push the credit score into the premium band, reduce EMI pressure, and apply only when the profile looks clean.

Mint’s reporting consistently uses 750+ as a strong zone for better deals and approvals. Mint also outlines practical steps like disputing report errors, keeping utilisation below 30%, and limiting fresh credit applications.

Before comparing lenders, borrowers need a quick way to prioritise fixes. The table below simplifies what usually moves the interest rate.

Here is a borrower-first checklist that lenders price into the final rate.

A clean profile also helps negotiation. Mint’s piece dated 06 Jan 2026 notes that borrowers can try renegotiation or a balance transfer after building a steady repayment record.

After the checklist, the next practical step is benchmarking “headline rates” versus what average borrowers actually get.

The story behind 2026 personal-loan pricing is the spread between “best available” deals and average borrowing costs. Business Standard’s lender table updated 02 Oct 2025 shows public ranges such as 10.05%–15.05% with indicative EMIs ₹10,636–₹11,908, and processing fees that can go up to 1.5% in some cases.

A LoansJagat report dated 19 Feb 2026 highlights “mean” pricing disclosures that many borrowers overlook. It reports SBI’s “Mean ROI 12.68% (Q4 FY25)” and an effective rate band of 10.00%–15.00% (effective from 15.08.2025). The same LoansJagat report also cites Axis Bank’s effective ROI band of 9.99%–22%, with a Mean Rate 11.84% for loans disbursed during Jul 2025–Sep 2025.

These disclosures show why borrowers with weaker profiles rarely land the lowest advertised rates.

*T&C Apply

Rishabh Goel, Founder and CEO of Credgenics, told Mint that a score like 657 signals moderate risk and needs corrective action such as on-time repayments, utilisation below 30%, fixing report errors and limiting new applications.

In a Hindustan Times report dated 25 Oct 2025, Kukreja is quoted saying banks view a 750+ score as “low risk”, which can support quicker approvals and lower rates.

In 2026, the cheapest personal-loan rates are still going to borrowers with 750+ scores and utilisation below 30%, with low EMI pressure.

The rate spread in public disclosures makes one thing clear: improving the profile first often saves more than switching lenders blindly.

Related Financial News | |||