RBI Holds Rates: How 5.25% Repo Affects Home Loans And Deposits

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

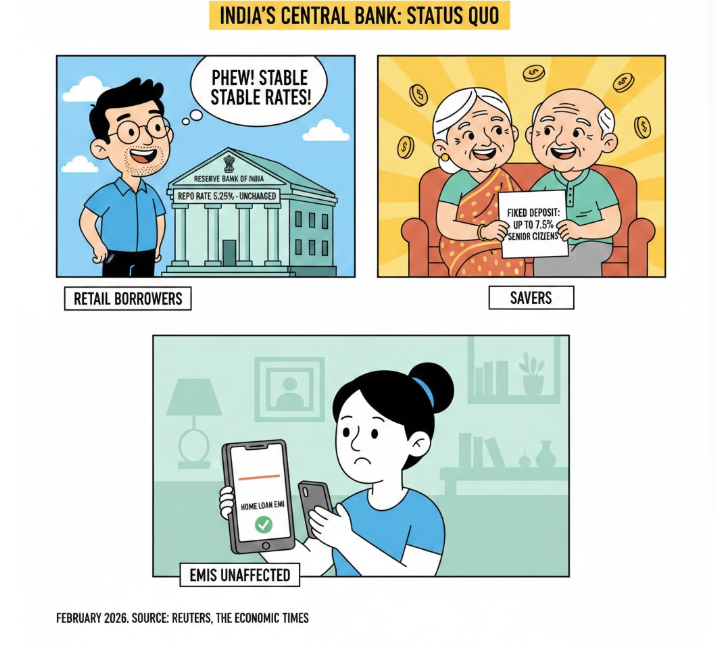

The RBI’s latest policy kept the repo rate at 5.25%, so borrowers get stability on EMIs while savers watch FD rates for the next bank repricing cycle.

India’s central bank has opted for a status quo on interest rates in February 2026, holding the repo rate at 5.25% and retaining a neutral stance. For retail borrowers, that usually means no sudden movement in floating loan EMIs unless their bank resets the rate or changes the spread.

For savers, it keeps the current FD-rate environment largely intact, with some banks still offering up to 7.5% for senior citizens on long tenures. The decision also comes when bond yields remain sticky even after rate cuts since early 2025, shaping how quickly cheaper credit reaches consumers.

Why The Rate Pause Is In Focus?

The issue is simple: households were watching for another cut, but the RBI chose stability. The policy decision kept repo at 5.25% and continued with a neutral stance, signalling that the next move depends on inflation and growth prints, not market expectations.

For borrowers, a pause often means the interest rate does not automatically fall further, so EMIs may not reduce immediately. ABP Live’s personal finance explainer also flagged that EMIs are unlikely to rise on a pause, while FD rates may remain range-bound in the near term. For savers, it is a reminder to lock returns carefully because banks can reprice deposits quickly once liquidity improves.

The Real Impact On EMIs, FDs And Monthly Cashflows

For most home loans that are repo-linked, the rate typically resets as per the benchmark cycle. With the benchmark unchanged, many borrowers should see stability rather than instant relief.

A similar tone runs through consumer coverage like LoansJagat, which noted that home loan rates staying steady can support housing demand.

Here is a quick, practical mapping of what households usually feel after a pause.

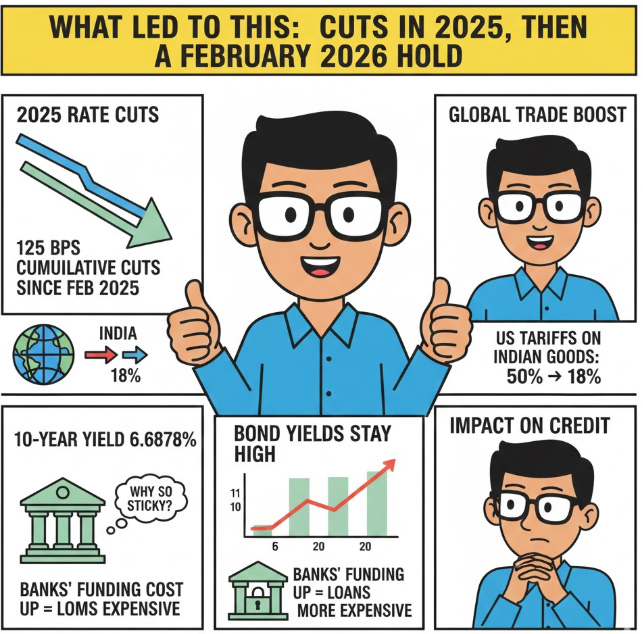

What changes the real experience is transmission. A major reason EMIs and loan rates do not fall uniformly is that government bond yields can stay high even after repo cuts. The Economic Times report, citing an Ambit Capital note dated February 13, 2026, said yields have not declined in line with the 125 bps repo-rate reduction since February 2025, partly due to a credit-deposit gap that slows pass-through.

On deposits, FDs remain attractive for many retirees and conservative savers. The Economic Times reported on February 14, 2026 that some banks were offering up to 7.5% for senior citizens on a 10-year tenure, with a maximum deposit cap of ₹3 crore in the examples cited.

What Led To This: Cuts In 2025, Then A February 2026 Hold

The current pause is easier to read with the recent policy path. Reuters’ January poll coverage highlighted cumulative cuts of 125 bps since February 2025, which set the backdrop for expectations of a hold through 2026.

In February 2026, Reuters also pointed to a more supportive external outlook after trade developments, including a cited tariff reduction on Indian imports into the US from nearly 50% to 18% under an expected deal timeline.

Bond market behaviour has also shaped expectations. Reuters reported on February 13, 2026 that the 10-year benchmark yield rose to 6.6878%, and participants were discussing buybacks as yields stayed elevated, with the spread over repo widening to over 150 bps.

That matters for borrowers because high yields influence banks’ funding and the broader cost of long-term credit.

Before the wrap, a quick snapshot of the headline rate and macro projections reported widely after the decision.

These projections feed into household expectations: low inflation supports purchasing power, but if yields stay firm and banks guard margins, loan-rate cuts take longer to show up in EMIs.

What Stakeholders Are Saying

Governor Sanjay Malhotra said external headwinds have intensified, while trade developments improve the outlook, as Reuters captured in its policy-day coverage. On markets, The Economic Times reported the RBI signalled it would take pre-emptive liquidity steps to support policy transmission even while holding the repo.

On the saver side, The Economic Times’ FD coverage shows banks are still competing for long-tenure deposits with senior rates up to 7.5%, which depositors are tracking closely.

Conclusion

The pause keeps near-term EMIs predictable, but it does not guarantee cheaper loans quickly if yields stay elevated. For savers, the better play is comparing FD tenures and locking rates selectively while offers last.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article