Best Loan Repayment Strategy to Become Debt-Free Faster: Smart Methods Explained

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Insights

- Borrowers pay significantly higher interest when credit cards and personal loans run together, as interest rates on unsecured loans can go above 30% annually.

- The risk of missed payments increases when managing multiple EMIs, which can negatively impact credit scores and increase total repayment cost.

- Debt consolidation reduces financial stress by combining multiple loans into a single EMI, which makes repayment faster and more disciplined.

Yeh dukh(EMI) kaahe khatam nahi hota be? Is this your thought when EMI gets debited from your account every month? Don’t turn your loan into a lifetime subscription and take steps for the best loan repayment strategy to become debt-free faster!

A loan repayment strategy defines how a borrower prioritises loans, manages EMIs, and reduces total interest paid over time. Repayments happen randomly, and high-interest loans continue to grow silently without a strategy. The best loan repayment strategy is a structured approach to repay loans faster while reducing interest burden and mental pressure.

Shaleen’s Loan Problem!

Shaleen is 32 years old and works in a private company. He earns ₹85,000 per month and lives a stable life.

At this stage, Shaleen is focused on planning a secure future for his family. He wants to save for his children’s education and long-term stability. He used different credit options over time to meet earlier family needs and responsibilities.

Now, Shaleen wants to close his existing loans so that his income can be directed towards his family’s future instead of ongoing EMIs.

Read More : Never Pay Off Your Loans

Shaleen’s Current Loan Profile

Shaleen pays three EMIs every month. The credit card balance reduces very slowly because of the high interest. Shaleen now wants to understand which loan to close first and how to become debt-free faster.

Traditional Loan Repayment Methods and Their Challenges

Most borrowers usually explore traditional repayment approaches that promise faster loan closure but come with practical challenges.

- Snowball Method: This method focuses on closing the smallest loan first. It provides emotional motivation, but often increases overall interest cost.

- Avalanche Method: This method focuses on closing the highest-interest loan first. It saves more interest but requires patience and strict discipline.

This comparison is widely known as the snowball vs avalanche method India. While both methods work, they require managing multiple loans simultaneously, which remains stressful for borrowers like Shaleen.

Loan Refinance vs Prepayment - What Fits Shaleen’s Plan?

Shaleen wants to reduce loan stress without using up his savings as he focuses on his family’s future. Loan prepayment requires a large lump sum and can affect long-term family goals.

Loan refinance replaces existing loans with better terms and manageable EMIs.

Also Read : Loan Repayment Hacks

Balance Transfer vs Refinance - Shaleen’s Choice

Shaleen considers balance transfer and refinancing to reduce high credit card interest. Balance transfer offers short-term relief but comes with uncertainty after the offer period. Refinance provides stable EMIs and long-term clarity.

The refinancing through debt consolidation provides Shaleen a clear and predictable repayment path.

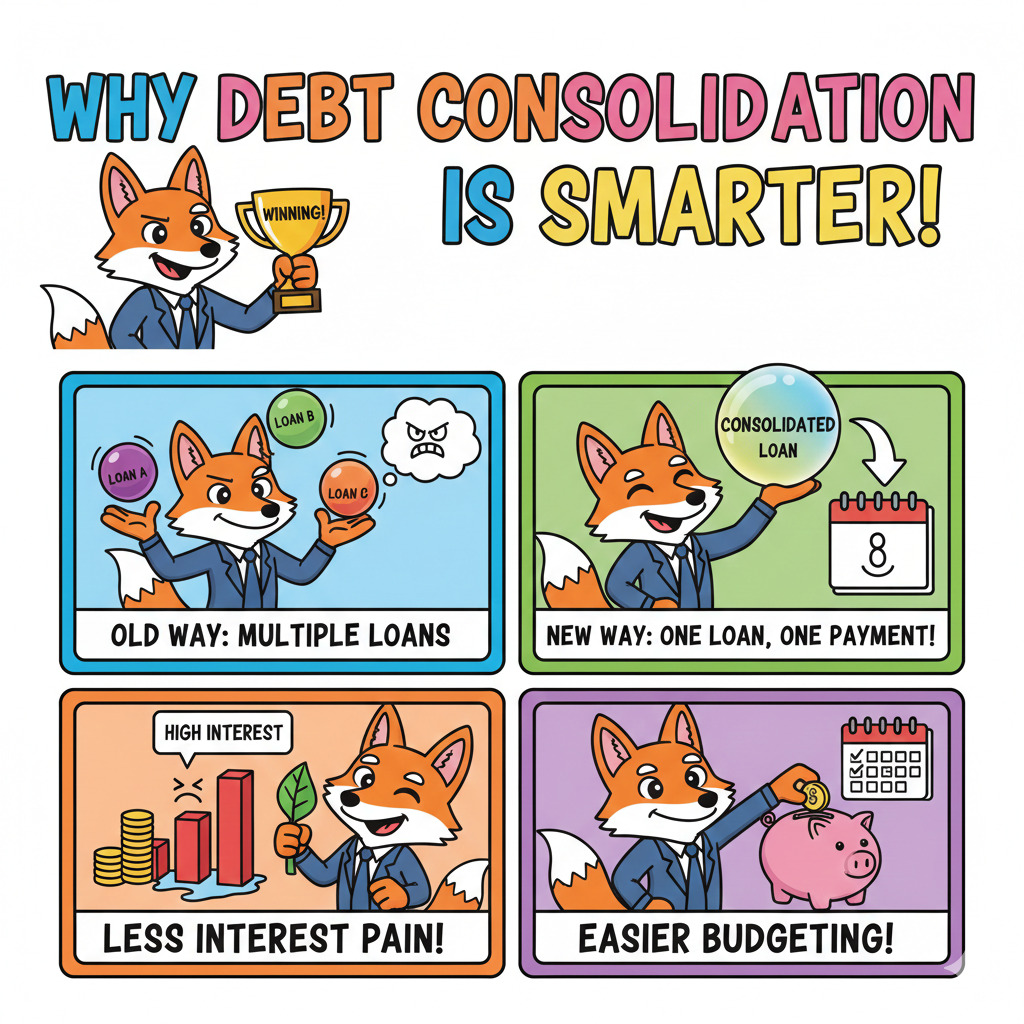

Why Debt Consolidation Becomes a Smarter Solution?

Debt consolidation combines multiple high-interest loans into one single loan with a lower interest rate and one EMI. People manage one structured repayment instead of juggling different lenders and due dates instead of juggling different lenders and due dates.

Shaleen’s Situation With and Without Consolidation

Debt consolidation helps Shaleen reduce interest costs and regain control over monthly cash flow.

Bonus Tip: India’s 2026 Union Budget prioritises medium-term debt consolidation and infrastructure growth, highlighting a focus on reducing overall debt and improving financial stability.

How You Can Become Debt-Free Faster Like Shaleen!

Shaleen can achieve faster debt freedom by following a structured repayment plan that focuses on simplicity, discipline, and long-term stability.

- High-interest loans are combined into one structured loan, which immediately reduces repayment complexity and interest burden.

- A single monthly EMI makes budgeting easier and removes the stress of tracking multiple due dates.

- Any extra amount paid goes directly towards the principal, which helps the loan close faster and lowers total interest paid.

- New credit usage is avoided during the repayment period, which ensures debt does not rebuild and progress stays on track.

Shaleen shortens his loan tenure and frees up income to focus on his family’s future instead of ongoing EMIs by staying consistent with this approach.

Conclusion

It is possible to become debt-free faster when loans are managed with a clear and structured strategy. You should choose the right repayment method, understand refinancing options, and use debt consolidation to reduce the interest burden and simplify EMIs. Take the first step today and plan loan repayment smartly.

FAQs Related to Loan Repayment Strategy

1. What is debt consolidation?

Debt consolidation means combining multiple loans or credit card dues into one single loan with one monthly EMI. It helps reduce interest burden and makes repayment easier to manage.

2. Which is the best debt consolidation company to pay off debt?

The best debt consolidation company is one that offers transparent interest rates, no hidden charges, flexible tenure, and proper guidance based on income and credit profile. Borrowers should always compare official lender terms before choosing.

3. Can I get a debt consolidation loan with bad credit and no collateral?

Yes, some lenders offer unsecured debt consolidation loans even with lower credit scores. Interest rates may be higher, but these loans help avoid payday loan traps and do not require assets like a car or house as collateral.

4. Should I take a debt consolidation loan to pay off credit cards?

A debt consolidation loan can work well if its interest rate is lower than credit card rates and the fees are reasonable. It is especially useful when multiple cards have high interest and repayments are not reducing balances effectively.

5. Will debt consolidation hurt my credit score in the long run?

Debt consolidation does not harm a credit score in the long run if EMIs are paid on time. In fact, regular payments and lower credit utilisation can gradually improve credit health.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article