Home Loan Balance Transfer Gains Momentum After 125 bps Repo Cuts

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

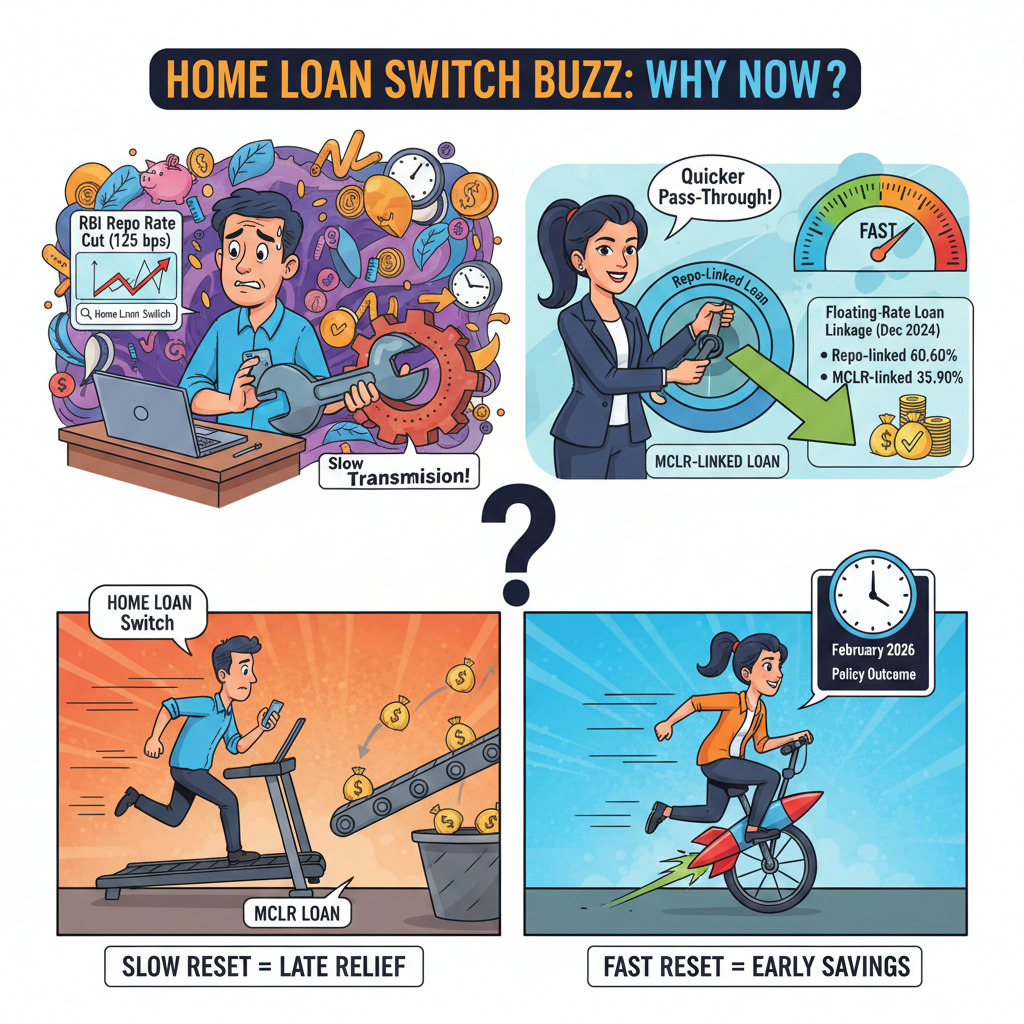

After RBI’s cumulative 125 bps repo cuts since February 2025, borrowers are chasing lower home-loan rates, but transmission gaps are pushing refinancing and switches.

Home-loan borrowers are back in negotiation mode. The trigger is the cumulative 125 bps repo rate cut since February 2025, but the benefit is not landing equally across borrowers. Banks have flagged that deposit shortfalls and tight liquidity are slowing lending-rate reductions, even after rate cuts.

Some borrowers are also stuck on slower-reset loan benchmarks, so their EMI relief arrives late or not at all. That is why “home loan switch” and “balance transfer” searches are spiking ahead of the February 2026 policy outcome.

What Is Driving The Home Loan Switch Buzz Now?

Borrowers want quicker pass-through of lower rates. A key split is the benchmark type. As per RBI data reported by Business Standard, 60.6% of outstanding floating-rate loans were linked to the repo rate as of December 2024, while 35.9% were linked to MCLR.

Read More - Home Loan Balance Transfer Explained

Repo-linked loans typically reprice faster than MCLR loans, so many borrowers are checking if a switch can reduce interest outgo over the remaining tenure.

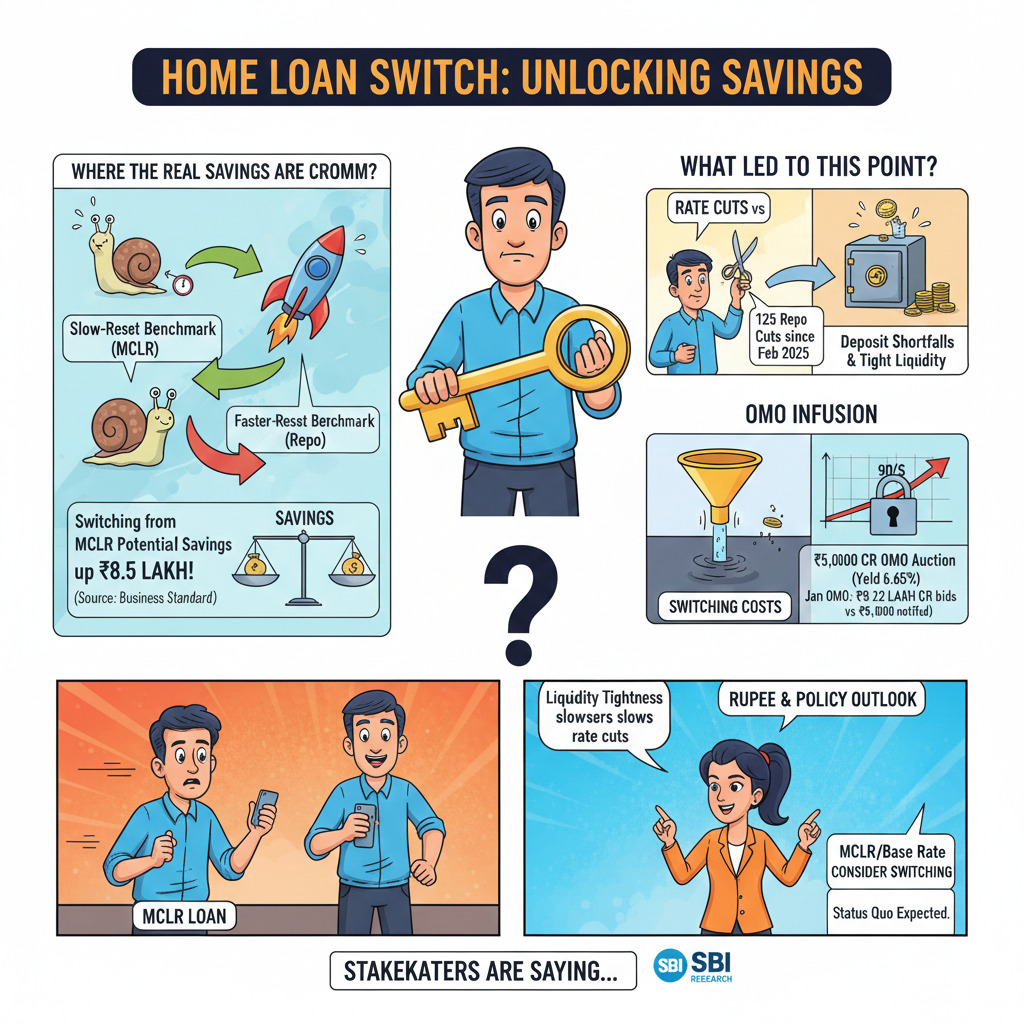

Where The Real Savings Are Coming From?

The strongest savings show up when a borrower moves from a slower-reset benchmark to a faster-reset benchmark, or negotiates a lower spread. When the rate reduction happens early enough in the remaining tenure, the interest component drops sharply across years.

A prior Business Standard report pegged the potential benefit clearly: borrowers on MCLR or base rate loans could save up to ₹8.5 lakh by switching to repo-linked loans, as per experts quoted in the report. The same story also flagged that borrowers should weigh savings versus switching costs.

For borrowers trying to understand why EMIs have not changed despite rate cuts, LoansJagat has also pointed to the reset cycle and benchmark mechanics. For switch options and process, its balance transfer explainer is commonly referenced by borrowers.

What Led To This Point (Previous Developments)?

The rate-cut cycle has been active, but transmission has been uneven. Reuters noted that lenders have struggled to cut lending rates because deposit growth has lagged credit demand, even after the 125 bps repo reduction since February 2025. That is also why banks have been pushing for liquidity-related regulatory relief, according to the same report.

Also Read - How to Transfer a Personal Loan to Another Bank

Liquidity operations have been in focus too. The Economic Times reported that an OMO auction of ₹50,000 crore saw better-than-expected demand, with the 10-year benchmark yield falling 4 bps to 6.65%, citing CCIL data. In an earlier OMO, participants offered ₹1.22 lakh crore for a notified ₹50,000 crore purchase.

Ahead of the February policy, the rupee’s move also fed into rate expectations. Reuters reported strong resistance around 90 per dollar, with the policy rate expected to hold at 5.25%.

Now, the market’s recent policy and liquidity signals are in one place.

These signals shape how quickly banks reprice loans and how aggressively borrowers chase refinancing.

What Stakeholders Are Saying?

Lenders have told Reuters that liquidity tightness and deposit constraints are making rapid lending-rate cuts harder, even after repo reductions. On the borrower side, experts quoted by Business Standard have urged those on MCLR or base rate loans to consider switching.

SBI Research expects a status quo at the upcoming policy, as reported by Upstox.

Conclusion

The refinancing pitch is simple: when benchmark type and reset cycles delay relief, switching can unlock meaningful savings.

Borrowers are now comparing spreads, reset dates, and switching costs more closely than ever in a 5.25% policy-rate environment.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article