RBI Repo Rate February 2026: Will Home Loan EMIs Fall After MPC Decision?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Markets expect a February pause at 5.25%, but home loan EMIs may not soften quickly. Transmission, reset dates, and refinancing options will decide relief.

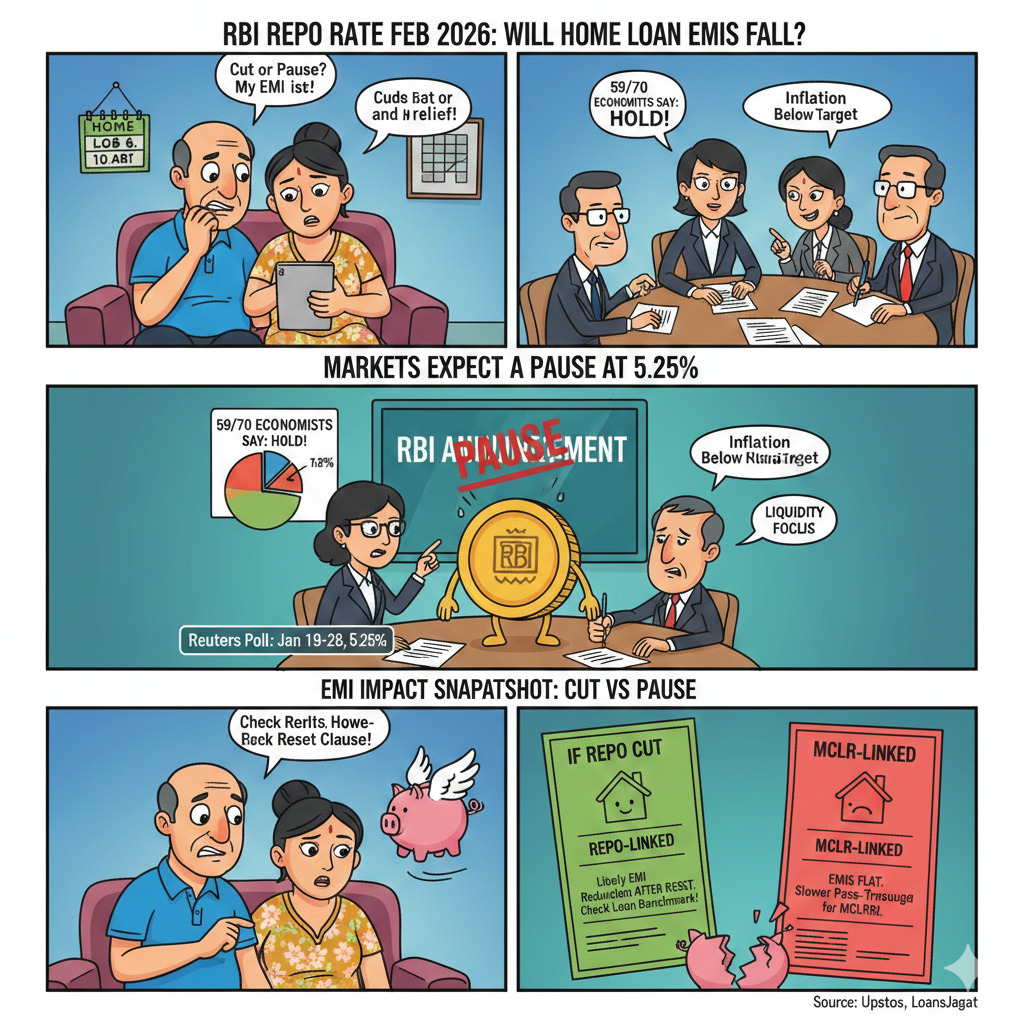

The policy decision is due on February 6, 2026 at 10:00 am, after the February 4 to 6 review. The repo rate is currently 5.25%, and borrowers are tracking whether another cut comes or whether the central bank pauses after aggressive easing since early 2025.

Most economist polls are leaning towards a hold, even as inflation remains far below the medium-term comfort zone. For home loans, the bigger story is not just the headline rate, but how fast banks pass it on to retail borrowers.

What Is At Stake For Borrowers And Lenders?

A repo pause typically means no automatic EMI drop for floating-rate borrowers in the immediate cycle. A cut, if it happens, can reduce the interest rate after the next reset for repo-linked loans.

But borrowers on MCLR-linked loans often see slower pass-through. Lenders, meanwhile, face profitability pressure in a falling-rate environment, with rating agency commentary already flagging margin compression risk if yields soften faster than deposits reprice.

February 2026 Rate Call And EMI Impact Snapshot

Most street expectations point to a hold at 5.25%. A Reuters poll conducted January 19–28, 2026 reported 59 of 70economists expecting rates to stay unchanged, with the broader view that the easing done since February 2025 should be allowed to transmit.

Moneycontrol’s poll-based reporting also flagged a similar base case: a pause with focus shifting to liquidity and transmission.

Some consumer-focused explainers still discuss the chance of a last 25 bps move, and LoansJagat has framed it as a “cut vs pause” setup for borrowers ahead of the announcement.

Read More - RBI Cut the Repo Rate By Another 25bps

If there is no fresh cut, Upstox expects home loan and other retail rates to broadly stay at current levels, with banks possibly passing earlier reductions gradually.

The table below sums up the likely outcomes.

After the outcome, borrowers should check the loan benchmark and the reset clause first, not just the headline move.

How The Cut Cycle And Inflation Prints Shaped Expectations?

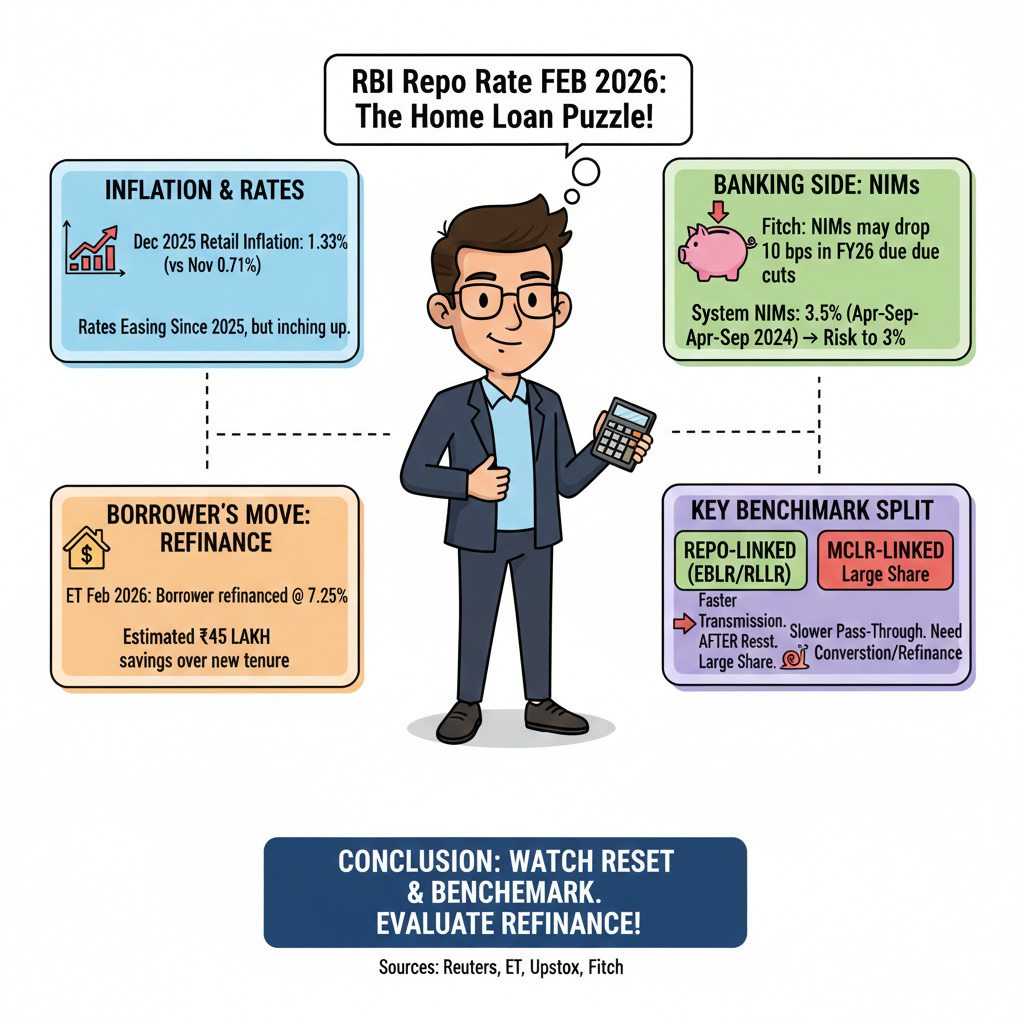

Rate expectations are being shaped by a year of easing and still-soft inflation. Reuters has reported that December 2025 retail inflation rose to 1.33% from 0.71% in November 2025, while the Reuters poll expectation was 1.5%. This followed an earlier phase where inflation prints were unusually low, and the trend is now inching up from the bottom.

On the banking side, Fitch commentary reported by Reuters estimated Indian banks’ net interest margins may see a 10 bps hit in FY26 due to rate cuts. It also noted system NIMs averaged 3.5% in April–September 2024, with a risk of trending towards a longer-term 3% zone if yields ease further and liquidity stays tight.

For borrowers looking beyond EMIs, refinancing has become a practical lever. An Economic Times report dated February 2, 2026 cited a borrower securing a refinance offer at 7.25% and estimating savings of ₹45 lakh over the new tenure after switching.

Here is the key benchmark split borrowers should know.

This is why some borrowers see relief quickly, while others do not.

Also Read - Bank Loan Write Offs India And Growth Impact

What Stakeholders Are Signalling

Reuters January-end poll suggested the dominant call is a steady 5.25% through 2026, implying limited near-term triggers for EMI cuts. () Upstox said if there is no fresh cut, retail lending rates are likely to remain at current levels, with gradual pass-through only.

Conclusion

If the repo is held, borrowers should watch their lender’s reset schedule and benchmark type for real EMI movement, not the headline. Those stuck on higher spreads may evaluate conversion or refinance offers.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article