Liquidity Tightness Hits Banks As Loan Demand Rises

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

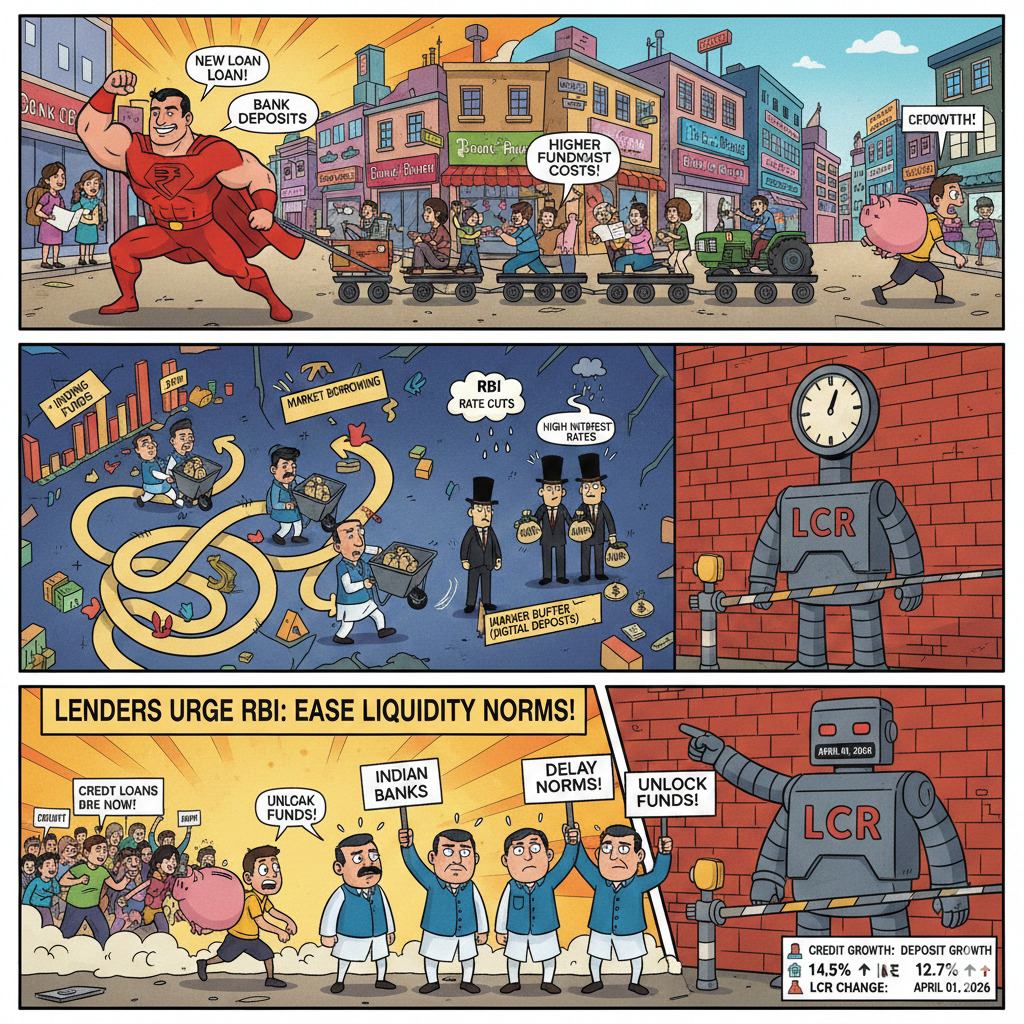

Indian banks want looser liquidity rules as loan demand rises faster than deposits, raising funding costs and complicating rate cuts for borrowers.

Indian lenders are urging the central bank to ease liquidity-related requirements as credit demand stays strong, but deposits are not keeping pace. The gap is forcing banks to depend more on market borrowing, keeping funding costs elevated even after policy rate cuts.

Indian Lenders Call for Postponement of LCR Buffer Norms

Reuters reported on February 05, 2026 that lenders have sought a delay in new Liquidity Coverage Ratio norms due April 01, 2026, along with other relaxations to unlock funds for lending. At the same time, liquidity support steps announced in late 2025 have not fully eased pressures in short-term money markets.

Banks point to the widening credit-deposit mismatch, which is raising competition for deposits and increasing reliance on certificates of deposit (CDs).

The mismatch is central to lenders’ pitch: more lending headroom is needed, without pushing deposit rates sharply higher.

What Is Driving The Current Squeeze?

Banks are seeing strong loan appetite, while deposit growth remains slower, tightening available funds in the system. Reuters noted lenders find it difficult to reduce lending rates despite 125 basis points of repo rate cuts since February 2025, as liquidity is tighter and bond yields remain high.

The drain is also linked to foreign exchange operations that absorb rupee liquidity, according to the same report. The immediate concern is the upcoming April 01, 2026 LCR implementation, which banks say could force higher liquid-asset holdings at a time when credit demand is rising.

What Banks Are Asking For?

Lenders have put a set of specific demands on the table. First is a request to delay the revised LCR norms due April 01, 2026, particularly the 2.5% additional buffer on digitally-linked deposits.

Second is a proposal to treat part of banks’ cash reserve ratio balances as eligible high-quality liquid assets for LCR, which would provide relief without changing reserve requirements.

Third, lenders want more flexibility to reclassify bond holdings between held-to-maturity and trading buckets to improve balance-sheet management in a high-yield environment.

Banks are also seeking approval to raise longer-tenor bulk deposits via CDs. Reuters reported on January 20, 2026 that banks want CDs with maturities up to 3 years, compared to the current up to 1 year, to reduce rollover pressure and funding volatility. Treasury teams argue the heavy use of short-tenor CDs has become expensive as supply rises.

Liquidity actions announced earlier have helped, but lenders say they need more durable support. For instance, a LoansJagat report dated December 23, 2025 said the RBI planned to inject ₹2.90 lakh crore into the banking system through liquidity measures.

How This Has Evolved Over Time?

The liquidity debate has been building since the central bank began tightening how banks account for run-off risks from digital deposits. By April 2025, reports highlighted that banks were required to assign an additional 2.5% buffer rate on digitally enabled deposits, with the changes set to take effect from April 01, 2026. Outlook Business carried the update on April 22, 2025, reflecting the direction of travel towards stricter liquidity resilience rules.

Despite these steps, the credit cycle stayed strong. Informist reported on January 10, 2026 that bank loan growth hit an 18-month high of 14.5% as of December 31, 2025, underscoring why lenders are pushing for regulatory flexibility now.

Banks say the current combination of regulatory tightening, elevated yields, and deposit competition is keeping borrowing costs sticky on the ground.

What Stakeholders Are Saying?

Bank treasury officials told Reuters they want permission for longer-tenor CDs up to 3 years to reduce rollover pressure and smooth asset-liability management.

Market reports such as 5paisa have also echoed the banking sector view that easing liquidity rules could unlock funds for lending amid strong demand and slower deposit growth.

Conclusion

If regulators allow temporary flexibility, banks may gain funding relief and price loans more competitively. If not, deposit rate competition and market borrowing are likely to stay intense.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article