Home Loan Tax Deductions For First-Time Buyers: Key Rules

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Buying a first home is also becoming a tax decision. With Budget 2026 clarifying pre-EMI treatment and the new regime limiting deductions, many borrowers are recalculating savings.

First-time homebuyers often assume the home-loan tax break will automatically reduce their tax outgo. In practice, the benefit depends on 2 decisions: whether the buyer files under the old tax regime or the new one, and whether the property is self-occupied or let-out.

The Income Tax Department has clearly stated that under the new regime, interest on borrowed capital for a self-occupied property is not allowed as a deduction from house property income. That single line changed the maths for many salaried buyers who had shifted to the new regime by default.

Why Are First-Time Buyers Rechecking Deductions?

The core issue is not the home loan itself, it is the regime choice and proof trail. Under the old tax regime, the typical home-loan relief comes from Section 80C (principal-linked) and Section 24(b) (interest-linked).

Read More - Home Loan Interest Deduction

Under the new regime, the self-occupied interest deduction is not allowed, which wipes out what many borrowers consider the biggest benefit. This is why a buyer who is paying large interest in the early years of the loan often sees a sharper tax difference between regimes. Also, buyers of under-construction homes face a documentation gap, because pre-EMI interest is not claimed the same way as regular interest after possession.

Before getting into the details, here is the regime impact in one glance.

This table is the pivot. Once the regime is clear, the filing becomes far less confusing.

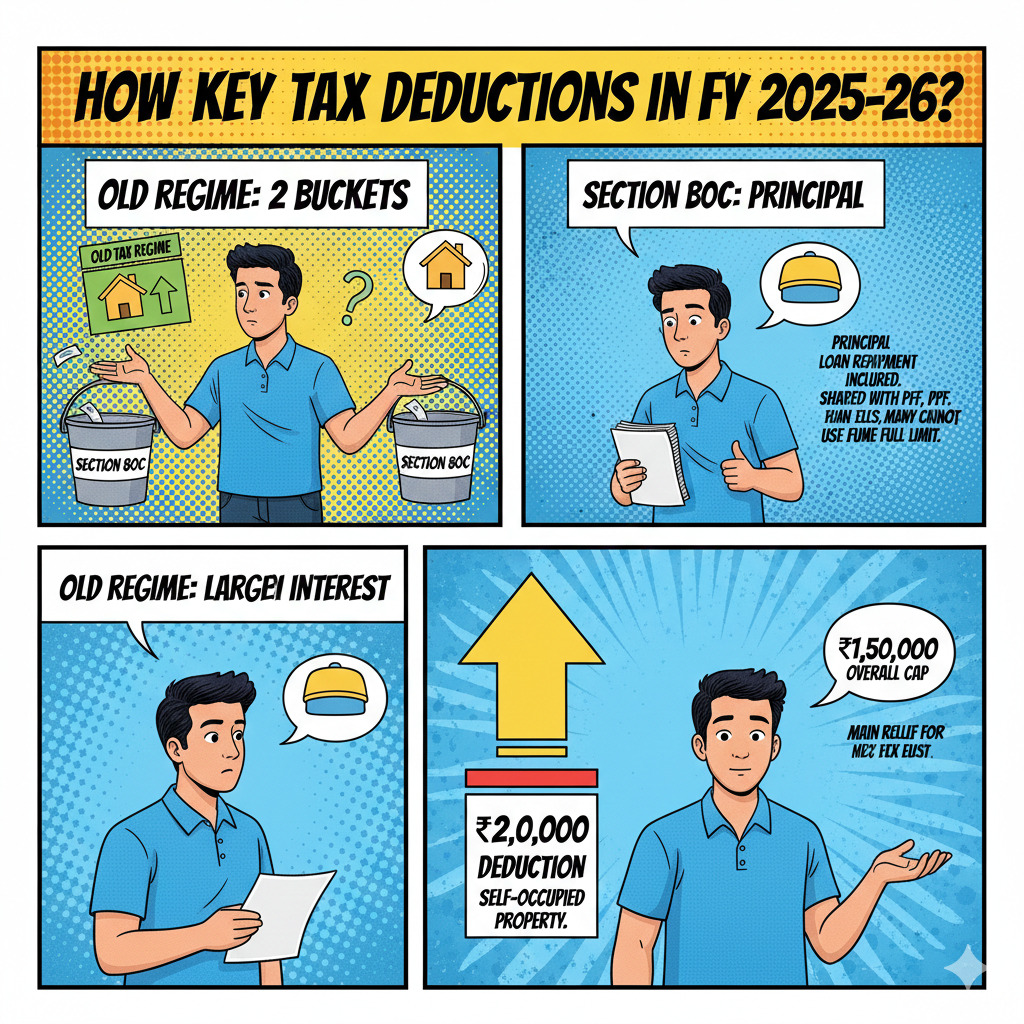

How The Key Deductions Work In FY 2025–26?

For buyers choosing the old regime, the usual tax relief is split into 2 buckets.

Section 80C allows deductions up to ₹1,50,000 (overall cap) and includes eligible items like the principal part of the home loan repayment. Since this cap is shared with PF, PPF, ELSS and other investments, many buyers cannot use the full limit for principal.

Section 24(b) is the main relief for interest. Multiple credible explainers continue to report the self-occupied interest deduction limit at ₹2,00,000 under the old regime framework.

Here is a section-wise map for quick reference.

Employers usually ask for an annual interest certificate and possession-related proof for under-construction cases, so borrowers need paperwork ready well before proof-submission deadlines.

What Changed Over Time And Why It Still Trips Buyers?

In recent years, 2 developments have kept home-loan deductions in the news cycle.

First, the new tax regime has become the default for many taxpayers, and official FAQs have repeatedly highlighted that self-occupied home-loan interest is not allowed as a deduction in the new regime. This has led to a visible spike in regime comparisons during ITR season, especially among young salaried buyers who are paying higher interest in the initial loan years.

Second, Budget 2026 has clarified the tax treatment of pre-construction or pre-EMI interest. Coverage by Economic Times reported that Budget 2026 revised Section 22(2) of the Income Tax Act context to clarify that pre-EMI interest is included within the total deduction limit for home loan interest, and the ₹2,00,000 cap remains for self-occupied property under the old regime.

Also Read - Tax Treatment of Pre-Construction

Similar reporting by Hindustan Times pointed out that prior-period interest can be claimed in 5 equal instalments after completion or possession, but it sits within the same overall cap.

Times of India also reported that the pre-construction interest benefit remains intact and continues to be spread over 5 years post-possession, addressing fears of a sudden withdrawal.

Alongside this, policy updates around the new Income Tax Act, 2025 and its rollout from 01 April 2026 have kept taxpayers alert on compliance and forms.

What Tax Dept, CAs And Lenders Are Pointing Out?

The Income Tax Department’s FAQ is blunt: interest on borrowed capital for self-occupied property is not allowed under the new regime, so taxpayers wanting that deduction must opt for the old regime.

Chartered accountants quoted in recent Budget 2026 coverage have also stressed that pre-construction interest is claimed after possession in instalments, and not as a full deduction in the year it is paid.

Lenders and platforms continue to push documentation discipline; LoansJagat’s explainer reiterates the headline limits of ₹2,00,000 under Section 24(b) and ₹1,50,000 under Section 80C as the common filing anchors.

Conclusion

For first-time buyers, the biggest tax swing comes from choosing the correct regime and keeping possession and interest proofs in order. Budget 2026’s pre-EMI clarity reduces ambiguity, but it also makes the cap discipline more important.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article