Credit Limit Hike: Pros, Cons, Credit Score Impact Explained

.png&w=3840&q=75)

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

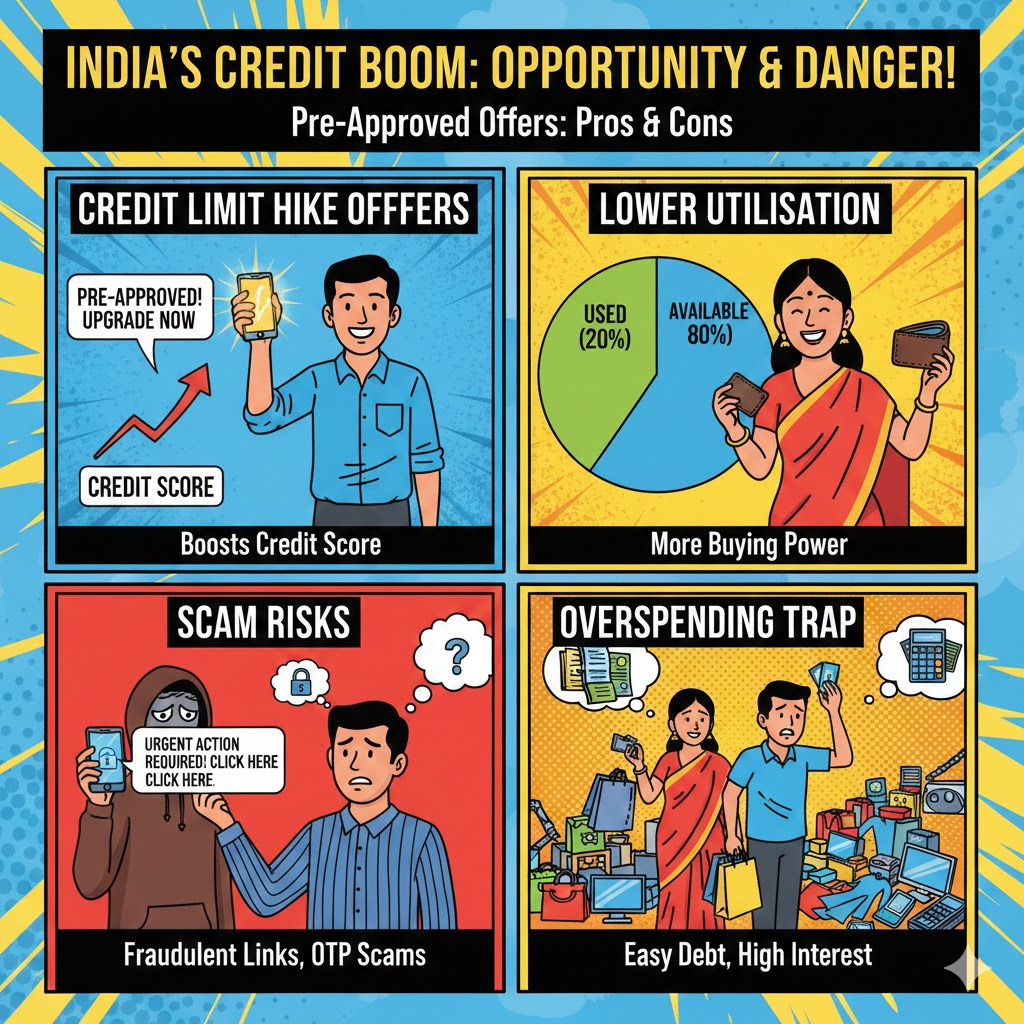

More Indians are getting “pre-approved” credit limit hike offers. It can lift credit scores by lowering utilisation, but scams and overspending risks are rising.

Credit card limit enhancement offers have become routine across banking apps and call centres. For many users, the pitch is simple: a higher limit means more flexibility and a better credit score.

The fine print is behavioural and security-related. If spending rises with the new limit, interest costs can snowball. If the offer arrives through a link, it can be a fraud attempt posing as a bank “KYC” or “limit increase” request.

Recent reports from Moneycontrol and Mint also underline the same trigger point: utilisation above 30% is where people start considering a hike.

What Is The Issue With Credit Limit Hikes?

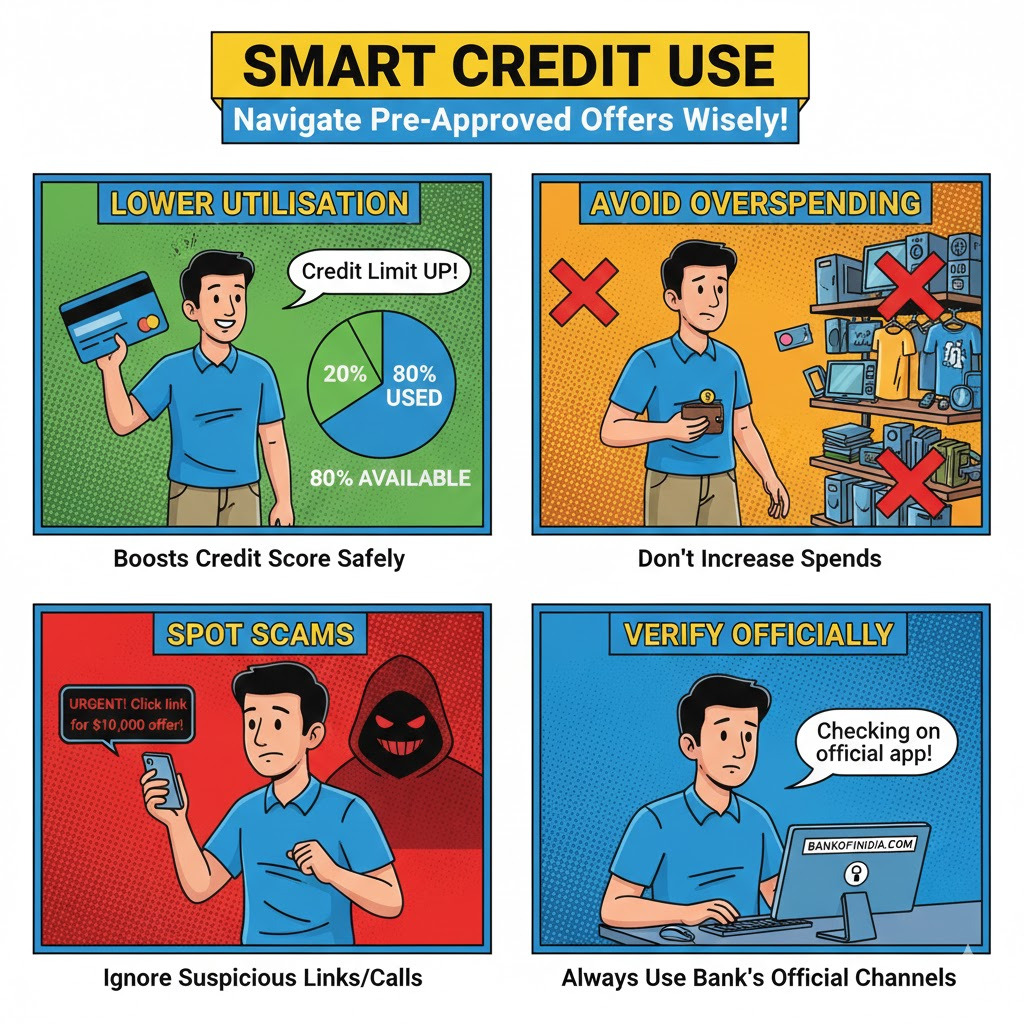

The core issue is not the higher limit itself. It is how it changes behaviour and exposure. On the positive side, a limit hike can reduce the credit utilisation ratio if the user keeps spending steady, which may support a stronger credit profile.

Mint notes that utilisation of 30% or lower is generally seen as good in credit-score calculations. On the negative side, higher limits can tempt higher swipes, and fraudsters are using “limit extension” as a scam hook.

How A Higher Limit Helps Or Hurts In Real Life?

Moneycontrol, in its February 19, 2026 explainer, gives a clear illustration of how scores can benefit when spending stays flat. If a user spends ₹30,000 a month on a card with a ₹50,000 limit, utilisation sits at 60%. If the limit rises to ₹1,00,000, utilisation drops to 30%, which is viewed as healthier.

Mint’s September 4, 2025 report adds that lenders see lower utilisation as a sign of better credit management and reduced repayment risk. But the flip side is simple.

If the bigger limit becomes a bigger lifestyle, the benefit disappears and repayment stress rises. Axis Bank’s guidance lists improved utilisation and flexibility as key pros, but flags overspending risk as the standout con.

A limit hike works best for disciplined pay-in-full users, and it works badly for minimum-due patterns.

What Has Happened Earlier?

Cybercrime reporting shows why “limit increase” messages should be treated cautiously. A Times of India report from Visakhapatnam, dated February 21, 2026, says a little more than 30 people were duped and over ₹20 lakh was siphoned off in a month using the limit extension and KYC pitch. Victims reported losses like ₹60,000 and over ₹80,000 after clicking links.

A separate The Times of India report from Kolkata, dated February 19, 2026, details a “help call” that led to ₹3.87 lakh being debited in 2 transactions via a fraudulent website.

On the credit-health side, mainstream personal finance writing has stayed consistent: keep utilisation around 30%. Mint’s April 15, 2025 report explicitly says users should consider a limit enhancement if utilisation exceeds 30% regularly. HDFC Bank’s April 30, 2025 explainer also highlights keeping usage below 30% to support the credit score.

Here is a quick checklist readers are using:

The security rule is blunt: no OTP, no unknown links, no remote app installs.

What Stakeholders Are Saying?

Police quoted in the Vizag report advised users to verify any such offers directly with the bank before acting, especially when a link is involved.

Banks emphasise discipline: Axis flags score benefits through better utilisation but warns against overspending. Mint adds that lenders view lower utilisation as reduced repayment risk.

The LoansJagat site’s report April 4, 2025 guide shares an example where a user’s limit rose to ₹1,50,000 and the score moved from 750 to 770 in 3 months, presented as an illustrative case, not a promise.

Conclusion

A credit limit increase is useful when it lowers utilisation without raising spends. If the “offer” arrives via link or repeated calls, the safer move is to ignore and verify on official channels.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article