.png&w=3840&q=65)

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

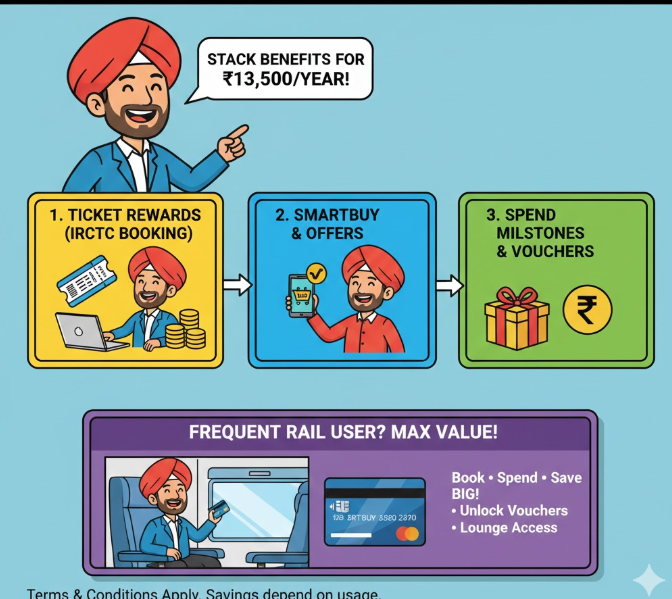

HDFC Bank’s IRCTC co-branded card is being promoted as saving up to ₹13,500 a year. The headline figure is conditional, built from rewards, cashback, fee waiver, vouchers and lounge value.

The IRCTC HDFC Bank Credit Card is back in focus after recent explainers flagged HDFC Bank’s claim of “save up to ₹13,500 annually”. What is being advertised is not a direct discount on every ticket.

HDFC’s own Value Chart shows the ₹13,500 as an illustration based on ₹2.4 lakh annual spends and assumes the cardholder uses multiple benefits, including SmartBuy cashback, quarterly vouchers and 8 complimentary IRCTC Executive Lounge accesses that HDFC values at ₹3,200.

For regular rail users, the decision comes down to one question: can the traveller actually meet the spend thresholds and benefit caps that sit behind the marketing line?

HDFC’s “up to ₹13,500” stack is made up of several buckets. The bank’s Value Chart lists reward value on IRCTC, SmartBuy cashback, a quarterly voucher track, fee waiver value and lounge value.

Below is the exact HDFC illustration, with each component and the annual value shown by the bank.

After adding it all, HDFC labels the total as ₹13,500 on ₹2,40,000 annual spends. In practical use, the realised value depends on how often the traveller books rail tickets through the right channels and how consistently they hit quarterly milestones.

The official FAQ spells out the earning structure: 5 Reward Points per ₹100 spent on IRCTC’s ticketing website or Rail Connect app, and 1 Reward Point per ₹100 on other spends.

On top of that, the card supports an additional 5% cashback for IRCTC bookings routed through HDFC Bank SmartBuy, which is also the route used for “Points + Pay” redemptions.

HDFC also offers a 1% transaction charges reversal on transactions done on the IRCTC website and Rail Connect app, which is one reason the offer looks unusually high versus regular cashback cards.

But the fine print is where outcomes change sharply. Caps apply to both reward accrual and cashback, and the FAQ restricts redemption through SmartBuy to up to 70% of fare plus IRCTC service charges.

Here is a quick view of the big caps and conditions that decide whether the claim is achievable.

The “up to” messaging becomes easier to read. A traveller who books frequently via IRCTC and SmartBuy, and also hits spend milestones, can add up multiple benefits in a year.

A traveller who only books tickets occasionally may only see the base IRCTC rewards and a small fee-related benefit.

The card’s broader pitch has been consistent since launch. In March 2023 coverage, HDFC Bank and IRCTC positioned it around “exclusive benefits and maximum savings” on bookings through IRCTC’s ticketing website and Rail Connect app, with joining benefits and lounge access.

A similar account in the same period reported HDFC Bank’s payments head saying the card would focus on savings tied to IRCTC channels and added lounge access at railway stations.

The current spike is more about packaging. A recent article revived the ₹13,500 figure using HDFC’s value chart and highlighted the combined effect of 5X rewards, SmartBuy cashback, and 1% transaction charge waiver.

In parallel, comparison chatter is rising because other railway-linked cards also market rail rewards, pushing travellers to compare caps and fee structures rather than just headline rates. A LoansJagat explainer on the SBI IRCTC RuPay Credit Card is one such reference point readers are using.

In the launch coverage carried by Financial Express, the joint messaging from HDFC Bank and IRCTC said the card will provide “exclusive benefits and maximum savings” for IRCTC website and Rail Connect app bookings.

Separately, Times of India’s report quoted HDFC Bank executive Parag Rao describing the focus on benefits tied to IRCTC booking channels, along with lounge access at railway stations.

On the consumer side, product explainers from platforms such as Paisabazaar continue to present the card mainly as a low-fee option for frequent train travellers, with 5X rewards and rail lounge access as key hooks.

The ₹13,500 figure is achievable only when multiple benefits are stacked and caps are managed, not from ticket rewards alone.

For frequent rail users who book through IRCTC and SmartBuy and hit spend milestones, the card can deliver meaningful annual value.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors |