Gen Z Turning 30 Faces Money Gaps: 6 Financial Moves That Matter

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Gen Z’s oldest cohort is nearing 30 in 2026. Digital-first banking is common, but emergency buffers and credit discipline are still weak for many.

Pew Research Center defines Gen Z as those born from 1997 onwards, putting the oldest of the cohort at 29 in 2026. In late 20s, money gaps start showing up faster, especially during job switches, rent jumps, medical bills, or family responsibilities.

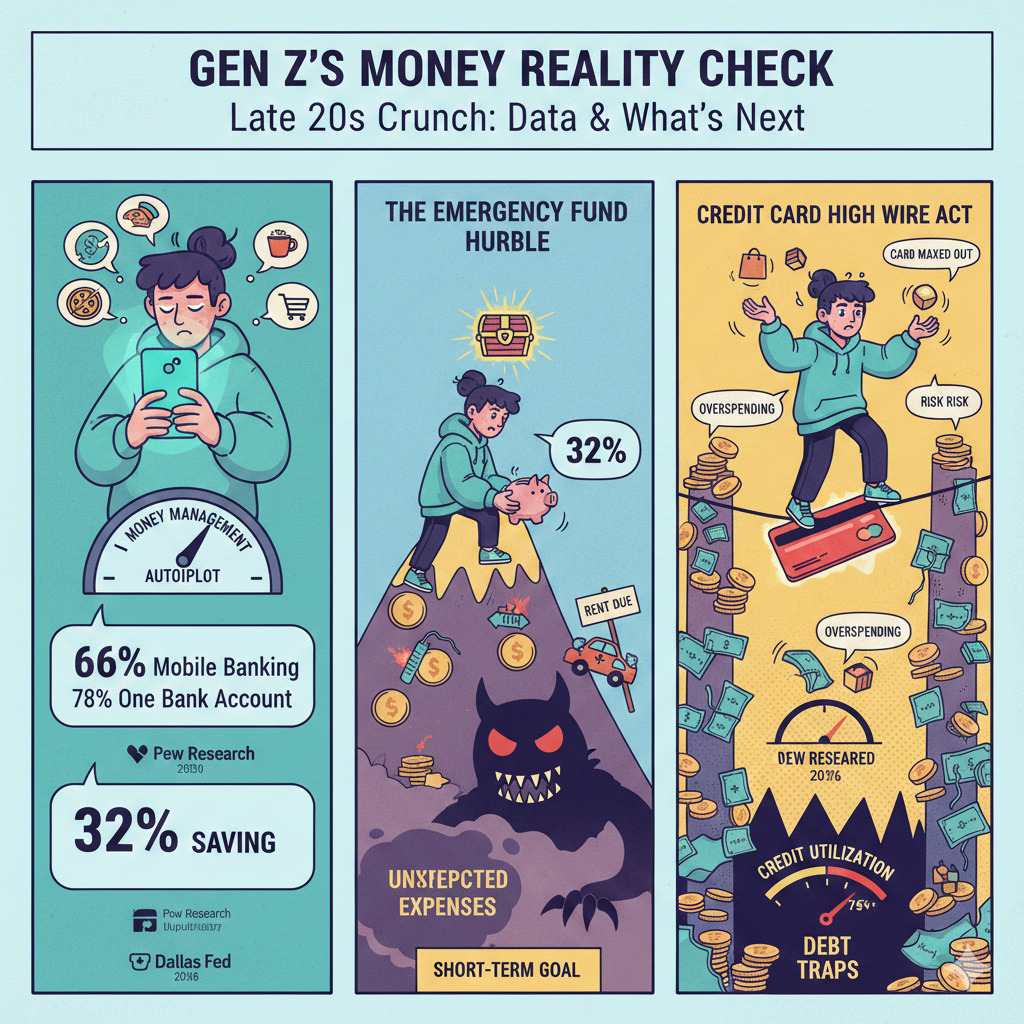

A YouGov report dated November 18, 2025 flags how Gen Z handles money: 66% use mobile apps as their primary banking method and 78% keep only 1 bank account. It also says only 32% are saving for an emergency fund, despite it being the top short-term goal for this group.

The Late-20s Money Crunch Gen Z Is Feeling

The issue is not about being careless. It is about money getting managed on autopilot. When banking happens mostly through apps, savings and repayments depend on defaults, reminders, and habits. YouGov’s Nov 18, 2025 study shows 24% of Gen Z admit they do not have a budget, and 12% say they overspend even after budgeting.

Credit risk also rises when spending is funded through cards. The Federal Reserve Bank of Dallas, in a post dated February 20, 2025, noted Gen Z borrowers in Texas have a bigger share of cards highly utilised, at 75% of credit limits or above, compared to other generations.

For Indian readers, the pattern is familiar. Digital payments reduce friction, but they can also hide leakage from subscriptions, food delivery, and short-term credit.

Read More - Growth at Indian Banks Reaches 10.8%

Before the fix, here is the data shaping the story.

This is why the next set of moves focus on buffers, repayment hygiene, and simple automation.

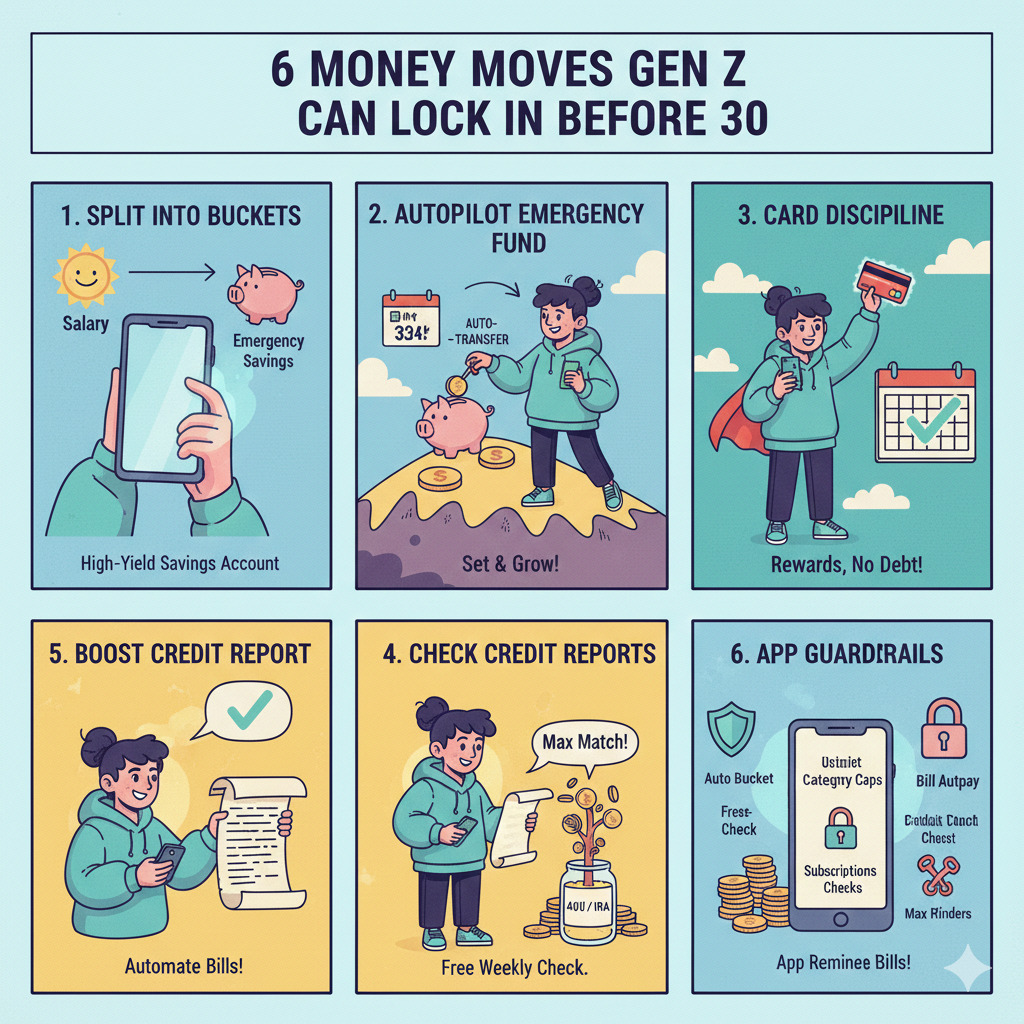

6 Money Moves Gen Z Can Lock In Before 30

The main story is practical. Gen Z already banks on the phone, so the upgrades should also be phone-friendly, with rules and automation.

Move 1: Split cash into buckets using a high-yield savings account (HYSA). Keep salary inflow separate from emergency savings. For US readers, FDIC’s explainer updated April 1, 2024 reiterates deposit insurance coverage of $250,000 per depositor, per FDIC-insured bank, per ownership category.

Move 2: Build an emergency fund with autopilot transfers. YouGov’s Nov 18, 2025 report says only 32% are saving for an emergency fund. Start with a starter buffer, then scale to a monthly-expense target.

Move 3: Use credit cards for rewards, but pay in full. myFICO explains payment history is 35% and amounts owed is 30% of the score components. (Page does not show a clear publish date; accessed Jan 30, 2026.)

Move 4: Check credit reports regularly. The official portal AnnualCreditReport.com states free weekly online credit reports are available. (Page does not show a clear publish date; accessed Jan 30, 2026.) The US FTC consumer alert dated January 4, 2024 also notes this weekly access was made permanent.

Move 5: Raise retirement contributions when possible. The IRS press release IR-2025-111 dated November 13, 2025raised the 2026 401(k) limit to $24,500 and IRA limit to $7,500.

Move 6: Use apps for bill timing, not just spending. Automate bill payments, set low-balance alerts, and create sinking funds. LoansJagat, in a post dated March 26, 2025, warns that using credit cards or personal loans in emergencies can mean 24% to 36% annual interest, which is exactly what an emergency fund helps avoid.

Also Read - Women Investors Rising In India

Here is a quick checklist, designed for fast action.

These steps keep the daily system simple, while reducing the chances of expensive borrowing.

How This Shift Built Up Over the Past Few Years

The timeline shows why Gen Z is at this point. Pew’s January 17, 2019 explainer set the widely used definition of Gen Z beginning 1997 onwards, separating it from Millennials.

As digital banking became routine, the “1 account, app-first” pattern got stronger.

By September 18, 2025, The Economic Times wrote that over 90% use mobile banking apps and 84% rely on UPI-based payment systems daily, with awareness of BNPL and robo-advisory products at over 70%.

At the same time, credit stress has been rising in pockets. The St. Louis Fed blog dated May 9, 2025 noted credit card delinquency rates rose over multiple quarters, and tracked increases of at least 40.6% in relative terms across geographies since mid-2021.

Retirement rules also shifted. US media including Axios covered the IRS limit hike on November 13, 2025, highlighting the higher $24,500 401(k) ceiling for 2026.

What Stakeholders Are Saying Right Now?

A USAA campaign quoted by the San Antonio Express-News on August 10, 2025 carried a clear warning. USAA Bank President Michael Moran said many Gen Zers “are lacking a crucial understanding” of how credit affects long-term financial health.

Regulators are also pushing monitoring and safeguards. The FTC’s January 4, 2024 alert encouraged consumers to use free weekly credit reports for routine checks.

Conclusion

Gen Z’s money toolkit is strong, but the basics need tighter systems. A cleaner savings setup and stricter credit habits can reduce stress before 30 hits fully.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article