By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

India’s gold-loan book is swelling fast. Higher gold prices are pushing up ticket sizes, while banks and NBFCs chase secured retail growth.

India’s gold-loan book is swelling fast. Higher gold prices are pushing up ticket sizes, while banks and NBFCs chase secured retail growth.

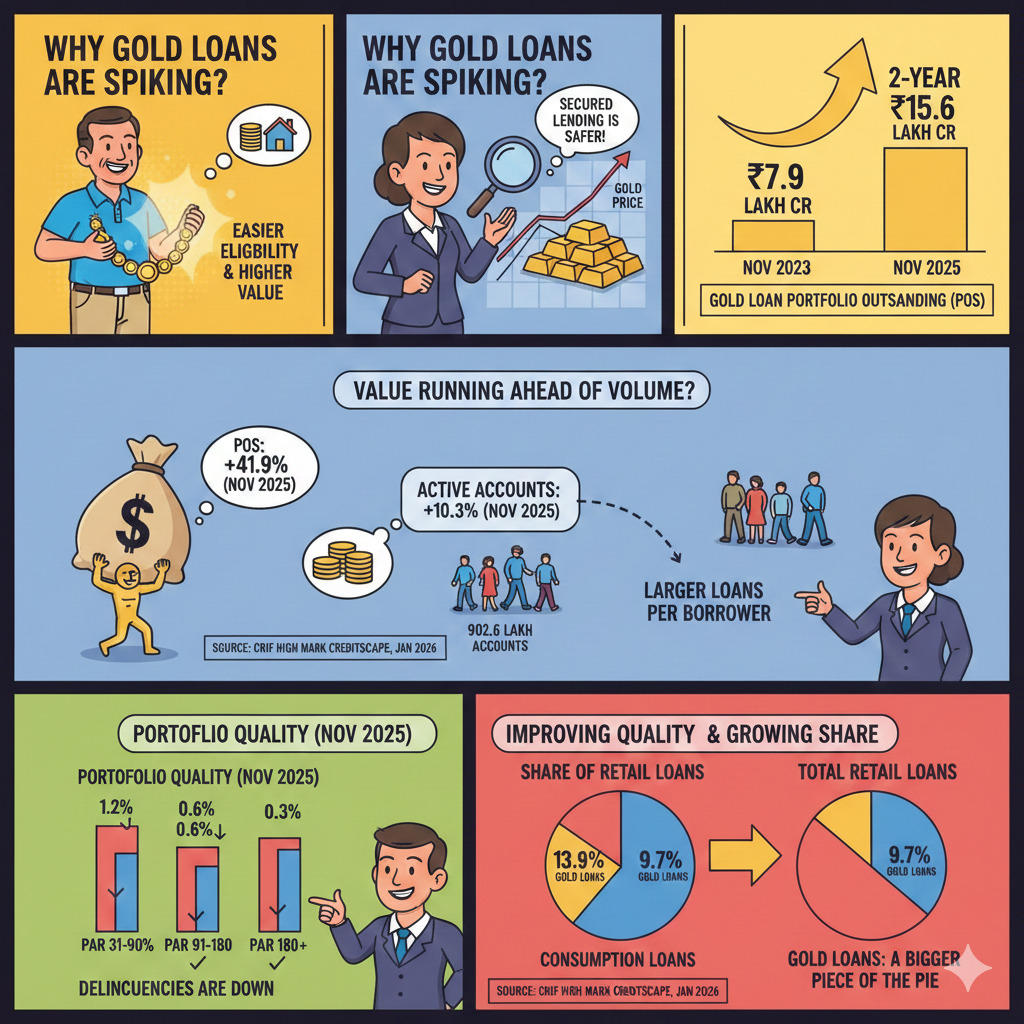

Gold-backed borrowing is getting bigger and more mainstream in retail credit. The latest CRIF High Mark CreditScape, “Gold Loans in India (Data as of Nov 2025)”, dated January 2026 shows the gold-loan portfolio outstanding (POS) at ₹15,60,000 crore (Nov 2025), up from ₹7,90,000 crore (Nov 2023).

That is close to a 2-year doubling. The push is coming from rising gold prices, easier borrower eligibility due to higher collateral value, and lenders leaning towards secured lending.

The headline growth is strong, but the more telling detail is the gap between value and volume. While POS grew 41.9% YoY in Nov 2025 (after 39.0% YoY in Nov 2024), the number of active gold-loan accounts rose only 10.3% YoY to 9,02,60,000. That points to larger average loans per borrower, not just a sudden flood of new accounts.

Read More - Bandhan Bank Gold Loan Interest Rate

The CRIF High Mark report also notes portfolio quality improving with early delinquency PAR 31–90 at 1.2% (Nov 2025), down from 1.6% (Nov 2023). Later buckets are lower too, with PAR 91–180 at 0.6% and PAR 180+ at 0.3% in Nov 2025.

Gold loans are also taking a bigger share in the wider retail pie. As of Nov 2025, they form 13.9% of total consumption loans and 9.7% of total retail loans by POS, with consumption loans at ₹1,12,20,000 crore and retail loans at ₹1,60,00,000 crore. All of this is laid out in the January 2026 CreditScape report.

The value is running far ahead of account growth, and lenders are still comfortable with asset quality in this segment.

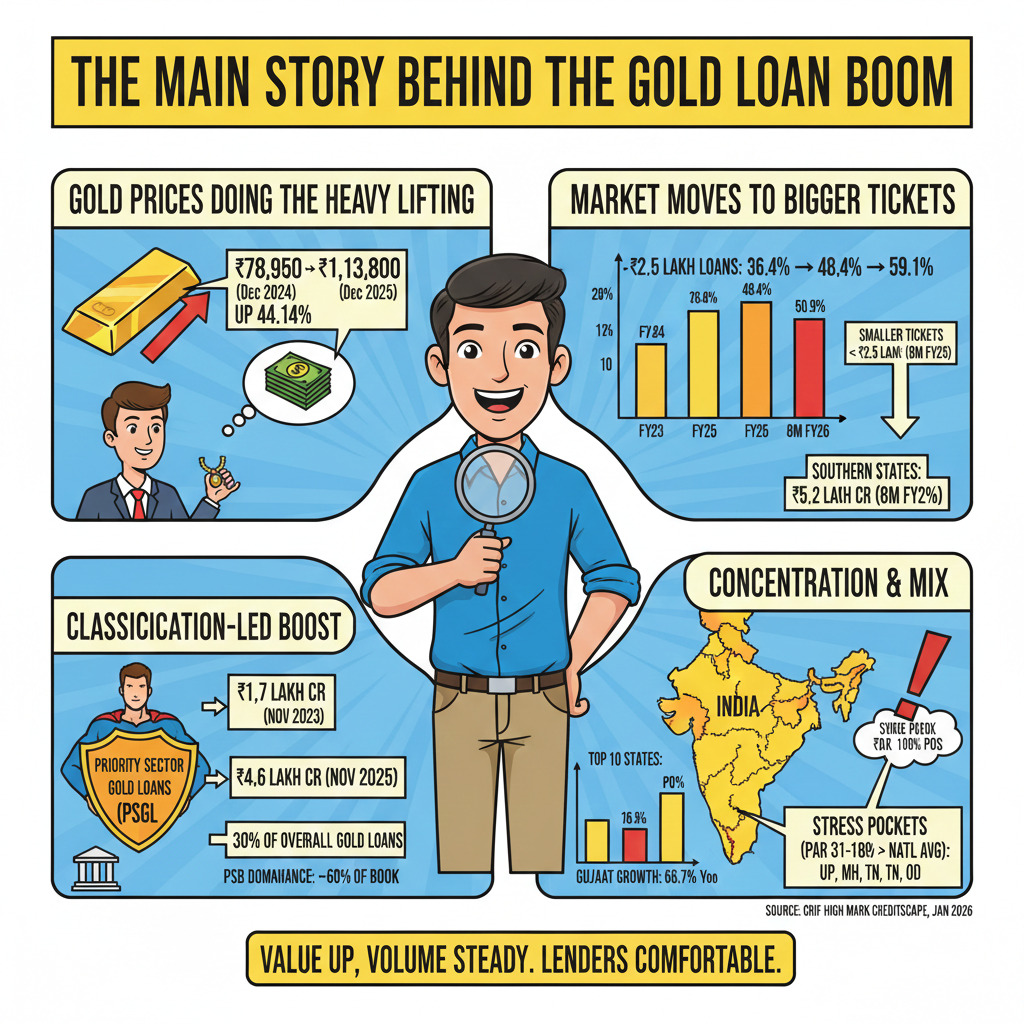

A lot of this story is gold prices doing the heavy lifting. One recent report pegged gold prices up 44.14% in 2025, reaching ₹1,13,800 per 10 grams, versus ₹78,950 on 31-12-2024.

That kind of jump increases the loan amount a borrower can raise against the same jewellery, even when lender policies stay tight. The CreditScape report shows the market moving towards bigger tickets too.

Loans above ₹2,50,000 formed 36.4% of origination value in FY23, rising to 48.4% in FY25, and 59.1% in 8M FY26. Smaller tickets below ₹2,50,000 fell to 40.9% in 8M FY26.

There is also a classification-led boost. Priority sector gold loans (PSGL) stood at ₹4,60,000 crore (Nov 2025), about 30% of overall gold loans, up from ₹3,80,000 crore (Nov 2024) and ₹1,70,000 crore (Nov 2023).

This shift is also being picked up by news desks. Business Today, published 2026-01-28 highlighted PSB dominance at nearly 60% of the outstanding book while citing the same CreditScape dataset.

The build-up started showing in 2025 itself, as the banking system gold-loan outstanding climbed sharply. A data-based update in late 2025 reported gold loans outstanding at ₹2,94,000 crore as of 25-07-2025, up 122% YoY, and linked the move to lenders trying to build a more secured retail book.

Then came the bigger headline prints. By end-November 2025, reports said bank gold loans grew 125% YoY, far above overall bank credit growth of 11.5%.

At the macro level, global gold prices staying elevated has added to the tailwind. A Reuters report said analysts expect gold to remain supported in 2026 due to geopolitical risk and central bank buying, even as volatility stays high.

Within India, the CreditScape report shows the growth is not evenly spread. The top 10 states account for 90.8% of POS, with southern states at >75%. Tamil Nadu alone stands at ₹5,20,000 crore, or 33.2% of POS (Nov 2025).

Gujarat led growth among top states at 66.7% YoY. It also flagged stress pockets where PAR 31–180 is above the national average, specifically Uttar Pradesh, Maharashtra, Tamil Nadu and Odisha.

Before the second table, here is the lender-and-location mix that explains where the book is sitting today.

The picture is clear: PSBs dominate by value, specialised NBFCs remain strong on account volumes, and the south continues to anchor gold lending.

Lenders are pitching gold loans as a secured retail product that helps balance risk when unsecured segments cool. Analysts tracking gold prices expect continued support in 2026, which keeps collateral values firm.

Borrower-side commentary is also turning policy-aware, with LoansJagat noting Budget 2026 may focus on safer, cheaper access in Tier-2 and Tier-3 markets as demand rises.

Gold loans are rising fast because gold prices are high and ticket sizes are getting bigger. The next print will depend on price trends, lender discipline, and borrower repayment comfort.