Home Loan Prepayment Vs Investing: 2026 Tax Impact

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Home loan borrowers in India are re-checking the prepay vs invest call after Budget 2026 clarified the ₹2,00,000 interest cap for self-occupied homes.

With FY-end planning picking up, many salaried borrowers are trying to decide where the next bonus or surplus SIP money should go. A home loan prepayment delivers a guaranteed saving by cutting future interest, while investments offer potentially higher returns but with market risk and liquidity trade-offs.

Budget 2026 has added a new layer to this decision by clarifying how pre-construction or pre-possession interest fits into the home loan deduction framework under the new Income-tax Act, 2025. Multiple tax experts and lenders are now advising borrowers to stop making date-driven moves and compare numbers calmly.

The Core Issue For Home Loan Borrowers

Should surplus cash reduce the principal outstanding, or should it stay invested for long-term goals? The answer changes based on the borrower’s tax regime, loan stage, and investment risk appetite.

Hindustan Times recently flagged that borrowers should not rush into prepaying only because March 31 is close, and should compare the home loan’s effective cost with post-tax returns from alternatives.

What Are The Latest Tax Clarity Changes In The Calculation?

Budget 2026 amended Section 22(2) of the Income-tax Act, 2025 to state clearly that prior-period interest (interest before possession) is included within the ₹2,00,000 overall deduction limit for a self-occupied home. The Economic Times report published 06/02/2026 notes this was meant to remove ambiguity created by the new law’s earlier wording, and align it with the long-followed treatment under the older framework.

Hindustan Times, in its report published 06/02/2026, explained the practical implication for under-construction buyers: prior-period interest can still be claimed in 5 equal annual instalments after possession, but the annual claim continues to sit within the same ₹2,00,000 cap for self-occupied property.

Here is what typically drives the “effective cost” calculation for borrowers using deductions.

The borrower takeaway is simple: if a borrower is already close to the deduction ceiling, extra prepayment does not automatically create extra tax relief. It may still reduce interest, but the tax benefit will not keep expanding.

What Happened Earlier And Why It MATTERS Now?

This clarification is not being positioned as a new benefit. It is being positioned as a continuity fix.

The Times of India, in a report published 03/02/2026, said Budget 2026 “put speculations to rest” on the tax treatment of pre-construction interest, and reiterated that the deduction continues as earlier, claimed post-possession over 5 years, with the self-occupied cap at ₹2,00,000. It also highlighted a growing pattern in Tier-1 cities where families book under-construction homes and carry long interest periods before possession.

The same TOI report quoted tax professionals saying the proposal clarifies interpretation rather than increasing the quantum. It also carried a sharper warning: since pre-construction interest is not deductible in the year it is incurred, delays in possession delay the tax benefit too, and if a project collapses, the tax benefit can be lost entirely.

Separately, the Hindustan Times report published 11/01/2026 used a borrower example to show how tax-year timing influences behaviour. It cited a Kolkata borrower with a ₹40,00,000 home loan who made a partial prepayment of ₹2,00,000 as the year-end approached, aiming to optimise Sections 80C and 24(b) within existing limits. The same piece stressed that March-end does not change the economics of the loan, it only affects accounting cut-offs.

LoansJagat has also warned against rushing into prepayment purely for the FY-end, arguing borrowers may lose flexibility if they lock in funds without a liquidity plan. ()

Here is a quick checklist Indian borrowers are using to avoid a decision driven by noise.

Prepaying can still be a strong call, but the reason should be interest savings and cash-flow comfort, not a panic around the date.

What Stakeholders Are Saying

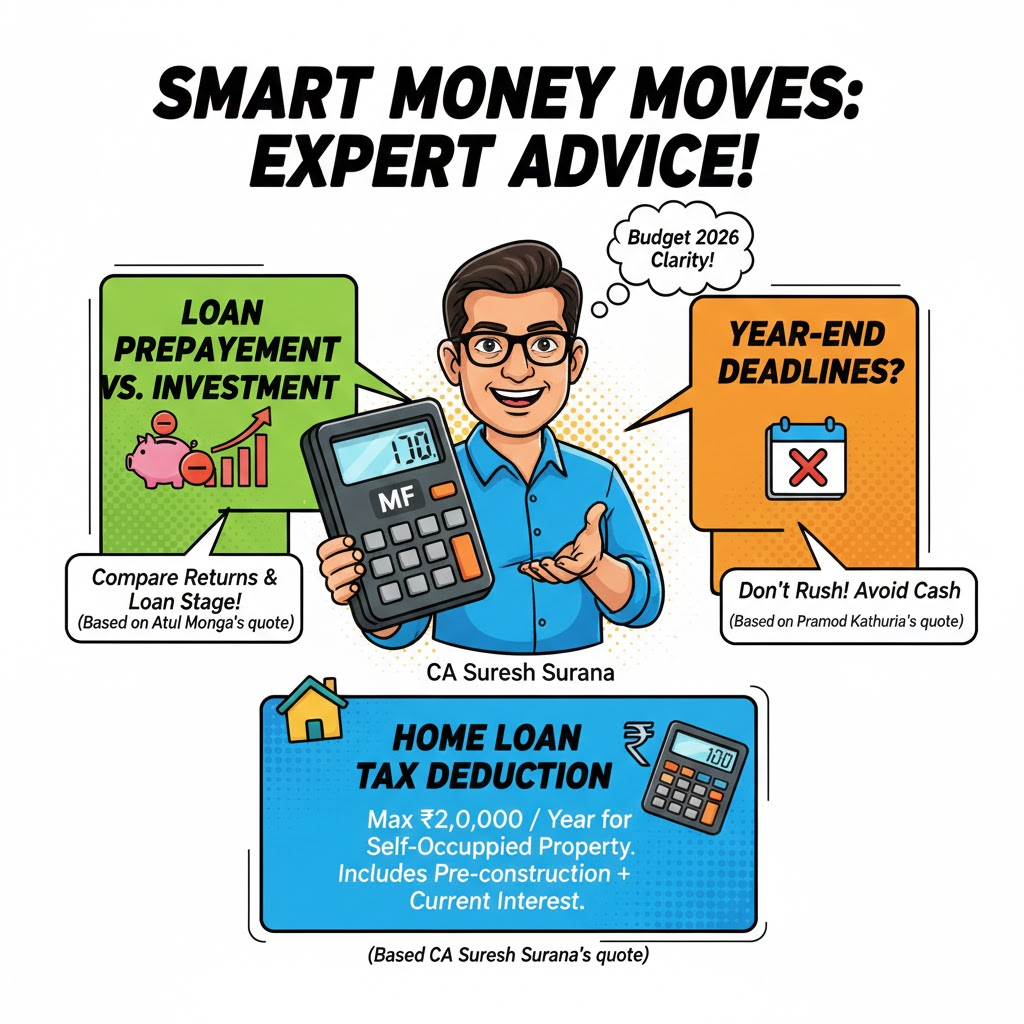

Atul Monga, CEO and co-founder, BASIC Home Loan, told Hindustan Times that if surplus funds earn less than the borrowing cost and the borrower is early in the loan cycle, prepayment can be better. Pramod Kathuria, founder and CEO, Easiloan, said the year-end date decides accounting cut-offs and should not force a cash-tight borrower into prepayment.

On the tax change, CA Suresh Surana told The Economic Times that current-year interest and prior-period interest together cannot exceed ₹2,00,000 in any tax year for a self-occupied property.

Conclusion

Budget 2026 has reduced confusion around the ₹2,00,000 cap, but it has not made prepayment “mandatory”. Borrowers who run a clean post-tax comparison and protect liquidity will likely avoid regret.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article