IDFC FIRST Bank Launches FD-Backed Hello Cashback Card With UPI Rewards Focus

.png&w=3840&q=75)

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

IDFC FIRST Bank has launched an FD-backed RuPay credit card that targets UPI-heavy users, offering up to 5% cashback with a ₹10,000 entry deposit.

IDFC FIRST Bank’s new Hello Cashback Credit Card is being positioned as a low-barrier, FD-backed RuPay card for people starting their credit journey. The card is issued against a fixed deposit starting at ₹10,000, with the credit limit linked to the deposit amount.

The bank is also pitching everyday rewards, including cashback on online spends and UPI payments, at a time when UPI continues to post record monthly numbers. For consumers who have struggled to get an unsecured card due to limited credit history, this product creates a direct entry route, but its real value depends on caps, exclusions, and how users spend.

What Is Driving Attention Right Now?

The immediate talking point is access. IDFC FIRST Bank’s own product page says the card does not require income proof or credit history, and is open for 18 to 80 years with an India residency requirement, as long as the FD is created and maintained.

Here is a quick, factual snapshot of how the card is structured.

This is essential because it ties credit availability to collateral, while using cashback to keep the product attractive for daily QR-led payments.

What The Card Actually Offers?

The headline offer is cashback. The bank’s product page lists 3% cashback on online spends up to ₹10,000 per statement cycle and 5% cashback on incremental online spends above ₹10,000. It also offers 1% cashback on UPI spends done via the IDFC FIRST Bank app, in-store swipes, and several essential categories such as utilities, education, insurance, rent, FASTag and railways.

The cap is where many users will do the math. The bank’s product guide shows that online cashback is capped at ₹1,000 per statement cycle and total cashback is capped at ₹1,500 per statement cycle. It also flags that online spends in essential categories and fuel will not count towards the ₹10,000 online spends milestone.

Another operational point: the bank’s feature document says cashback is credited after the payment due date, and paying at least the Minimum Amount Due on time is required to remain eligible for cashback for that cycle.

The annual fee waiver thresholds are also straightforward: 100% reversal at ₹2,00,000 annual spends, and 50% reversal between ₹1,00,000 and ₹2,00,000.

What Led To This Launch?

Banks have been chasing credit growth on top of UPI behaviour. NPCI’s official UPI monthly dashboard shows that January 2026 recorded 21,703.44 million transactions worth ₹28,33,481.22 crore.

Mainstream reporting has also underlined the pace: The Economic Times reported January 2026 at 21.7 billion UPI transactions and ₹28.33 lakh crore, and quoted Worldline CEO Ramesh Narasimhan saying, “UPI's growth momentum continues to strengthen.”

On the credit side, government-linked datasets have tracked RuPay credit card-linked UPI adoption since launch in September 2022, with year-wise volume and value disclosed through Parliament records.

This is also why “secured” cards are being pushed harder. With an FD as collateral, approvals are easier, and the card can still report repayment behaviour, helping customers build a usable credit profile over time.

For broader context on IDFC card offers and deals coverage, one industry page many readers use is LoansJagat IDFC credit card offers explainer.

What Key Stakeholders Are Saying?

From the bank’s side, Shirish Bhandari, Head – Credit Cards, FASTag & Loyalty, IDFC FIRST Bank, said the product is aimed at “digitally savvy customers beginning their credit journey” and highlighted the ₹10,000 entry threshold and “flexible annual fee waivers.”

From the payments ecosystem, the UPI growth narrative remains strong. The Economic Times carried the Worldline CEO’s view that UPI momentum is strengthening, reinforcing why banks are building credit products around UPI habits.

Consumer viewpoint is split: cashback looks attractive, but caps and category rules will decide whether users feel the payout in real monthly spending.

Conclusion

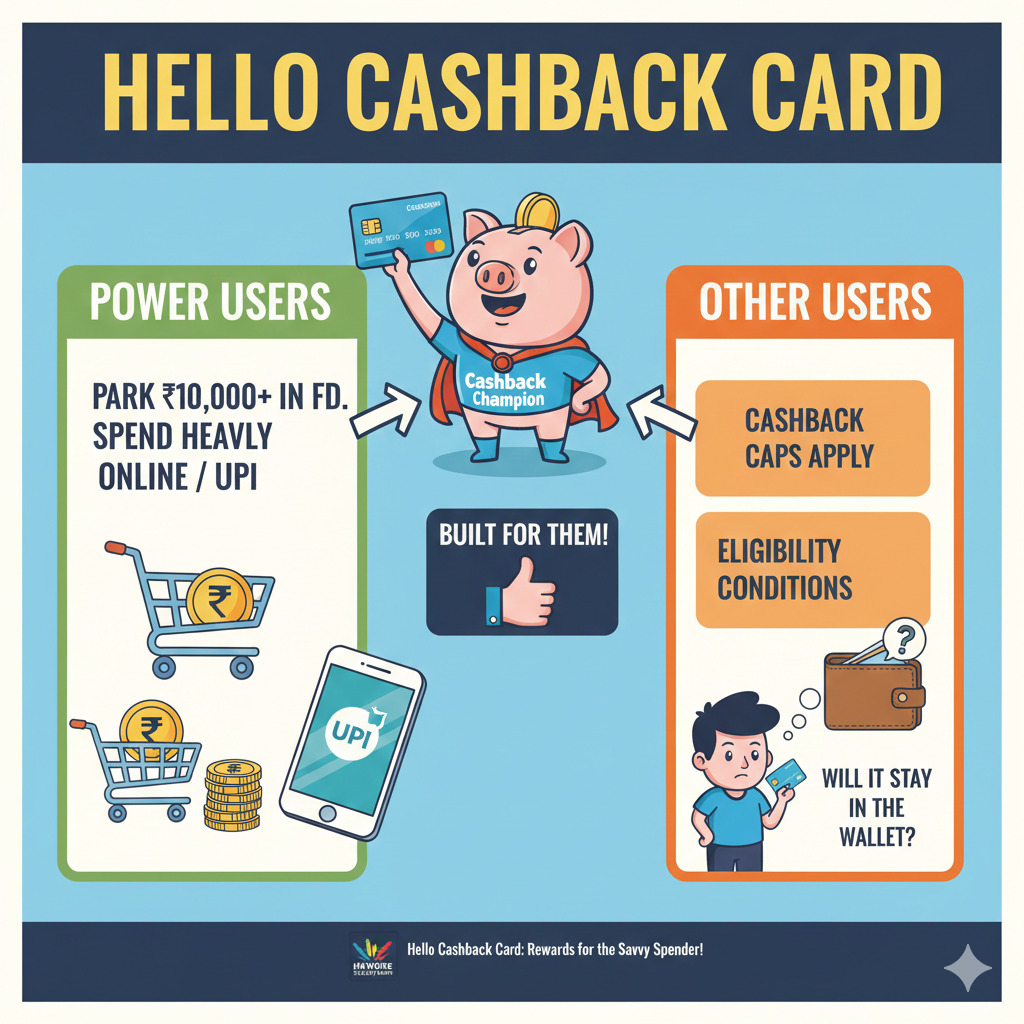

The Hello Cashback Card is built for users who can park ₹10,000+ in an FD and spend heavily online or via UPI. For everyone else, the cashback caps and eligibility conditions will decide whether the card stays in the wallet.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article