How Much Home Loan Can You Get In 2026? Eligibility Rules Explained

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

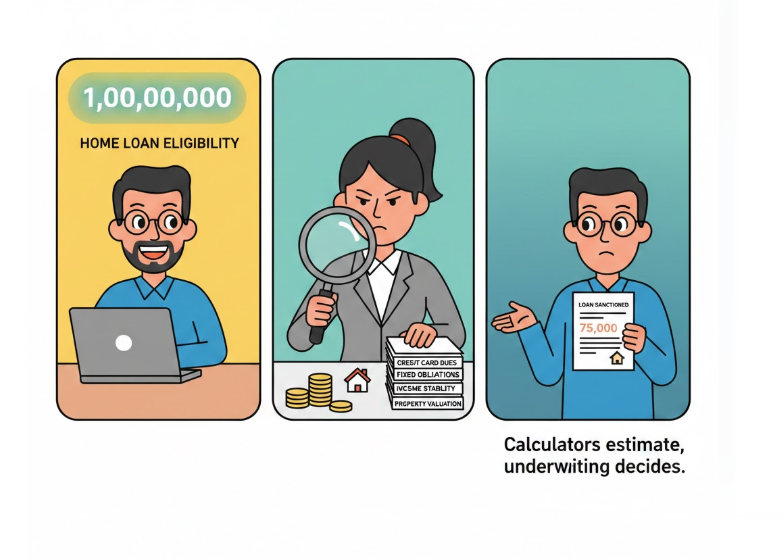

In 2026, home loan “eligibility” looks generous online, but final sanction often drops after banks apply FOIR filters, valuation checks, and LTV discipline.

Borrowers are seeing wide gaps between what a home loan eligibility calculator shows and what lenders finally sanction. The difference usually appears after the bank verifies fixed obligations, credit card dues, income stability, and property valuation.

Recent scrutiny around high-value loans has also pushed tight checks on Loan-to-Value, especially beyond ₹75 lakh. At the same time, benchmark-linked rate movements and MCLR resets keep changing EMI calculations, which impacts eligibility outputs across portals and bank sites. The result is simple: calculators estimate, underwriting decides.

Why Do Online Eligibility Numbers Look Bigger?

Most calculators assume a clean income profile and a high EMI capacity, then convert that EMI into a loan amount using a chosen rate and tenure. In reality, lenders cut the usable income if bonuses are irregular, cash flows are uneven, or documentation is thin. They also count existing obligations more strictly than borrowers expect, including credit card dues.

Even the interest rate range selected inside a calculator changes the number sharply. Axis Bank’s eligibility calculator itself shows floating rates in the 8.75% to 9.15% band, which shifts EMI-to-loan conversion instantly.

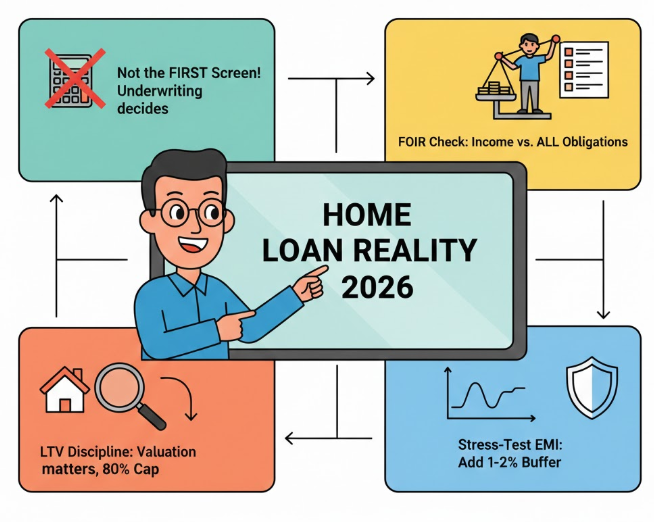

How Banks Actually Arrive At The Sanction?

Banks start with repayment comfort, not the property price. They check FOIR, which is the share of monthly income already locked into fixed obligations. IndusInd Bank describes FOIR as a lender metric that factors existing commitments like rent, loan repayments and credit card dues, and says lower FOIR improves capacity for a new EMI.

Bajaj Finserv’s explainer similarly defines FOIR as fixed obligations divided by income and flags it as a key eligibility filter.

Then comes the property filter. Loan-to-Value is where many approvals shrink, especially after valuation. A National Housing Bank-linked compliance push has kept LTV discipline in focus, with an The Economic Times report saying some lenders were pulled up for high-value loans being disbursed at up to 90% LTV despite a 75% cap.

The typical gap is best seen in what calculators ask versus what underwriting verifies.

For borrower journeys, marketplaces also influence expectations. LoansJagat’s eligibility calculator is widely used as a quick estimator, but the final number still depends on the lender’s checks and valuation outcome.

What Changed Over The Past Year?

The underwriting tone hardened after supervisory action around LTV practices. NHB’s public “Penalties” page lists cases where lenders were penalised for sanctioning loans beyond prescribed LTV ratios, signalling that enforcement is not theoretical.

A related Moneycontrol report dated 10 June 2024 reported a monetary penalty of ₹1 lakh on India Home Loan Limited for non-compliance, adding to the compliance narrative around housing lenders.

On rates, borrowers have seen frequent benchmark tweaks. Economic Times reported that SBI cut MCLR by up to 5 bps effective 15 August 2025, taking the MCLR range to 7.90% to 8.85% from 7.95% to 8.90% earlier. Business Standard later reported on 9 December 2025 that HDFC Bank reduced MCLR by up to 5 bps, with its MCLR range at 8.30% to 8.55%.

These rate moves change EMI math and can alter eligibility outputs.

With resets and spreads, the same borrower can see different EMI outcomes across banks, and eligibility calculators rarely reflect that nuance.

What Stakeholders Are Saying?

Industry updates point to 2 clear positions. Supervisory action reported by Economic Times indicates NHB wants stricter adherence to LTV limits on high-value loans. Banks, on the other hand, keep signalling small benchmark cuts and pass-through depends on reset dates, as reflected in SBI’s MCLR-linked impact coverage.

LoansJagat states that LTV limits are tiered, and borrowers can get up to 90% funding for smaller home loans, but only 75% for bigger loans above ₹75 lakh.

Conclusion

In 2026, the “real” loan amount is decided after FOIR checks and valuation-based LTV discipline, not the first calculator screen. Borrowers get better clarity by stress-testing EMI, listing every obligation, and checking valuation assumptions early.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article