Home Loan Rate Cut In 2026? Buyers May Need To Watch These Warning Signs

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Indian homebuyers waiting for cheaper loans in 2026 may not get quick relief as inflation, crude oil and bond yields stay sensitive.

Key Takeaways

- Home loan rates may not fall fast in 2026 as retail inflation rose to 3.48% in April, while ICICI Bank’s May rates are at 8.50% to 9.80%.

- Earlier, LoansJagat reported on April 23, 2026 that the 5.25% repo rate hold kept EMIs stable but made fresh cuts unlikely.

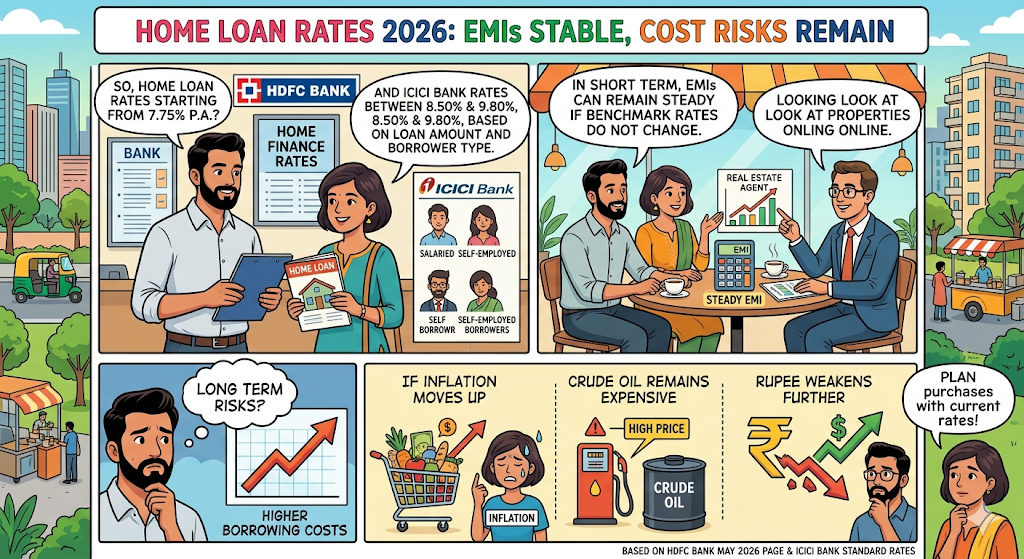

Home Loan Rates 2026: EMIs Stable, Cost Risks Remain

Home loan borrowers may have to plan 2026 purchases with current rates, not expected cuts. HDFC Bank’s May 2026 page shows home finance rates starting from 7.75% p.a., while ICICI Bank lists standard home loan rates between 8.50% and 9.80%, based on loan amount and borrower type.

In the short term, EMIs can remain steady if benchmark rates do not change. In the long term, buyers may face higher borrowing costs if inflation moves up, crude oil remains expensive, or the rupee weakens further.

Rate Cut Hopes Face A Reality Check

Reuters reported on May 12, 2026 that India’s retail inflation rose to 3.48% in April 2026, below its poll estimate of 3.8%, but energy risks from the Middle East conflict remained a concern. Food inflation was also a key driver.

This means banks may not rush to lower home loan rates. Trading Economics showed India’s 10-year government bond yield at 7.00% on May 27, 2026, up 0.76 percentage points from a year earlier. Higher bond yields usually keep loan pricing tight.

2026 Home Loan Watchlist

Buyers should track more than only bank advertisements. A low headline rate may come with processing fees, credit score conditions, loan-to-value rules, reset clauses and insurance add-ons.

Before taking a fresh loan, buyers should compare total cost, not just the first-year rate. Existing borrowers should ask their lender for spread revision or check balance transfer options.

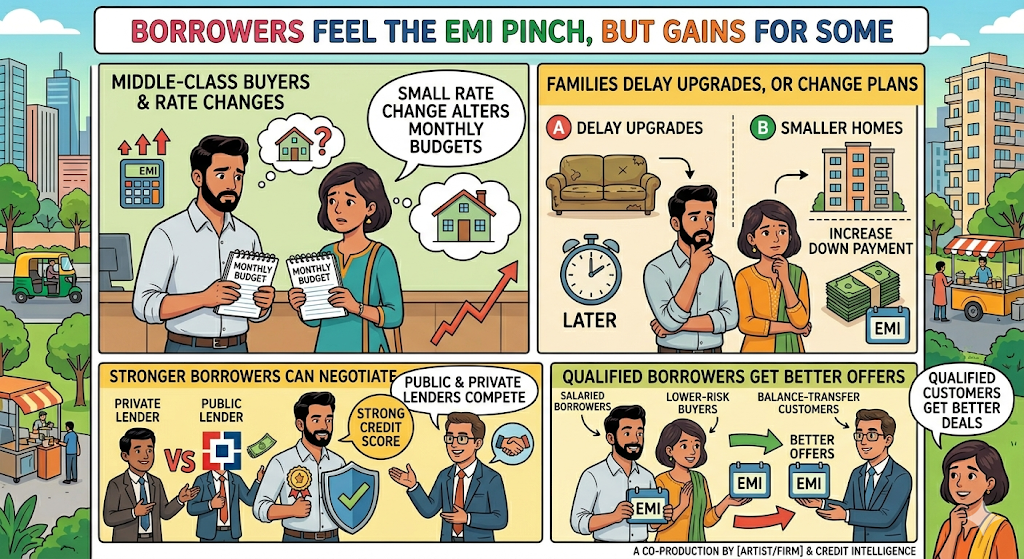

Borrowers May Feel The EMI Pinch, But Some Can Still Gain

For the middle-class buyer, even a small rate change can alter monthly budgets. If rates do not fall, families may delay upgrades, choose smaller homes, or increase down payments to keep EMIs under control.

The positive side is that borrowers with strong credit scores can still negotiate. Public and private lenders are competing for quality customers, so salaried borrowers, lower-risk buyers and balance-transfer customers may get better offers.

What Experts Say And What Buyers Should Do?

Reuters reported on May 21, 2026 that Standard Chartered economists expected possible rate hikes from June 2026 due to crude oil, rupee and inflation risks. Reuters also reported on May 22, 2026 that the central bank was not keen to hike only to defend the rupee and would focus on inflation.

LoansJagat reported on April 23, 2026 that the 5.25% rate hold kept home loan EMIs stable, but further cuts looked unlikely due to West Asia tensions and crude oil pressure. Borrowers should keep EMIs affordable at today’s rate and refinance only when the saving is higher than transfer costs.

Conclusion

A sharp home loan rate fall in 2026 looks uncertain for now. Buyers should track inflation, crude oil, rupee, bond yields and bank spreads before signing a long-term loan.

FAQs

Why do floating home loan rates go up quickly but come down slowly after rate cuts?

Banks may not cut floating home loan rates right away because every loan has a reset date. Even if the benchmark rate comes down, the borrower gets the benefit only when the loan reaches that reset cycle. For repo-linked loans, this can be monthly or quarterly.

For older MCLR or base-rate loans, the cut may take longer, and sometimes the borrower has to request a switch. The bank’s spread also plays a role. So borrowers should check the benchmark, reset date and spread in their loan letter. If the rate is still high, they can ask the bank for revision or transfer the loan.

Why do different banks offer different home loan interest rates in India?

Home loan rates in India are not the same for everyone. Banks first look at their benchmark rate, like repo-linked rate or MCLR. Then they add their own margin. After that, the borrower’s details come in. A good CIBIL score, steady salary, lower loan amount and clean repayment history can help in getting a lower rate.

Self-employed borrowers may get a slightly higher rate if income proof is weak. The property value and loan tenure also make a difference. So, before choosing a loan, one should check the final rate, reset date, fees and bank charges, not only the advertised offer.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article