Why Millions of Indian MSMEs Still Don’t Qualify for Bank Loans?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- MSME credit in India surpassed ₹40 trillion in March 2025, up 20% YoY But millions of small businesses still lack access to formal loans because traditional lending does not take into account informal income or seasonal cash flows.

- The SIDBI report notes that the current MSME credit gap is close to ₹30 lakh crore and experts and policymakers are promoting data-driven credit systems instead of traditional loan models.

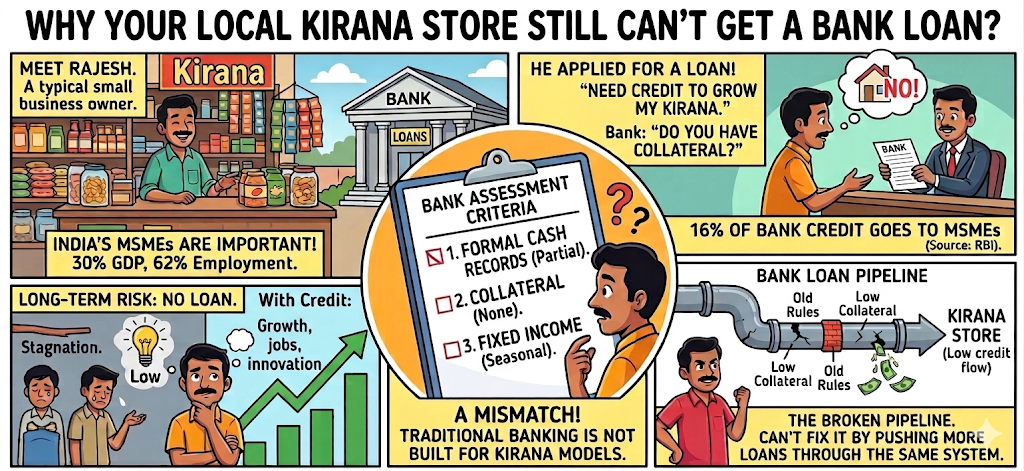

Why Your Local Kirana Store Still Can’t Get a Bank Loan?

India’s 63 million MSMEs contribute nearly 30% to GDP and over 62% of all employment. Yet they remain starved of credit. The problem is not a lack of schemes. It is a mismatch between how traditional banks assess loans and how small businesses actually operate.

Most MSMEs have seasonal income, partial cash records, and no collateral. Standard loan models were simply not built for them.

The danger over the long term is serious. If MSMEs cannot get credit at reasonable rates, their growth is stunted. Jobs disappear. Innovation slows.

Only about 16% of total bank credit reaches the MSME sector, according to the RBI, despite MSMEs being central to India’s economy. This gap cannot be closed by pushing more loans through the same broken pipeline.

How does this change India’s Credit Story?

Data-driven credit is a game-changer for millions of small business owners. They can now be assessed on real financial behaviour instead of being turned away for lacking paperwork.

Bank statement analysis, UPI transaction history, GST filings, and utility bills can all paint a reliable picture of a borrower’s ability to repay.

AI-powered lending models, leveraging alternative data such as digital payment trails and GST filings, could bridge an estimated USD 130-170 billion credit gap for India’s MSMEs, a PIB release said.

India’s Digital Public Infrastructure such as Aadhaar, UPI, and the Unified Lending Interface is building the foundation for AI-led financial inclusion.

What Experts Are Saying: Smart Credit, Not Just More Credit

Experts are clear that volume alone will not solve this problem.

Vaibhav Joshi, Co-Founder and CEO of EasyPay, says, “There is a clear MSME credit crunch for the sector and the main reason for this is a lack of financial inclusion, especially in Tier 3 cities and below.”

On the policy side, Finance Minister Nirmala Sitharaman urged fintechs and financial institutions to leverage ULI’s interoperable, digital-first framework to support the growth of MSMEs and bridge the long-standing credit access gap.

ULI aggregates financial and non-financial data such as GST filings, bank statements, digital payment records, and utility bills. This allows for data-driven underwriting even for borrowers with limited or no credit history.

The solution lies in layered risk assessment. Lenders must combine bureau data with live cash flow signals. Alternative records, like receipts of mandi or milk collection data, can be reliable inputs for rural businesses.

While the policy initiatives have been holistic, the respondents in the SIDBI’s survey continue to quote access to timely and adequate credit as a big challenge. This indicates awareness and last-mile implementation still lag behind policy intent.

Conclusion

India’s MSME sector does not lack ambition. It lacks fair access. Data-driven credit is not just a technology upgrade. It is a smarter and fairer way to recognise the true creditworthiness of millions of small businesses. As digital infrastructure matures and awareness grows, the gap between a business owner’s potential and their credit score can finally begin to close.

FAQs

1. Why are small businesses still struggling to get MSME loans despite so many government schemes?

Many MSMEs still cannot get loans because traditional banks rely heavily on collateral, formal income proof and credit history. Old lending systems often think small businesses are risky because they have seasonal income, cash transactions or limited paperwork.

2. Why were bankers unhappy with MSME loan announcements under Atma Nirbhar Bharat?

Many bankers felt the schemes increased pressure to lend quickly without fully solving issues like poor borrower documentation, repayment risks, and weak credit assessment systems. Experts say it needs better data-driven lending models, not just more loan targets.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article