PFRDA Allows Loan Against NPS Corpus: Key Rules, 25% Cap

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

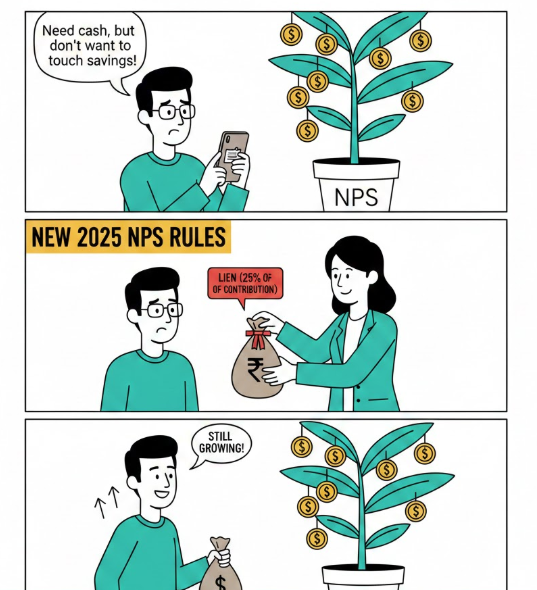

PFRDA’s 2025 exit-rule overhaul now allows loans against NPS via a lien on the pension account, capped at 25% of own contributions, giving subscribers another liquidity route.

The National Pension System has usually been treated as a long-horizon retirement product, with withdrawals tightly regulated to protect future income. That picture is changing. After the PFRDA (Exits and Withdrawals under NPS) (Amendment) Regulations, 2025 were published on 16-12-2025, the regulator introduced a new concept: financial assistance against pension corpus.

It lets a subscriber approach a regulated financial institution for a loan and allows the lender to mark a lien or charge on the individual pension account, within a defined limit. The move is being positioned as a liquidity option without forcing an early drawdown of retirement savings.

What’s Driving The Buzz Right Now?

PFRDA’s new facility is being read as “loan against NPS”. The government’s official note on key amendments states the lender may mark a lien or charge on the NPS account up to 25% of the subscriber’s own contribution, and it will be governed by guidelines issued by PFRDA.

Upstox, in an explainer updated on February 20, 2026, adds that subscribers can borrow against NPS by creating a lien and that this is not treated as a withdrawal. It quotes Tax2win’s Abhishek Soni saying there is no immediate tax liability at the time of taking the loan, while warning against casual borrowing that can hurt long-term retirement planning.

Moneylife, in its coverage dated December 19, 2025, reports the exposure is capped and the loan amount is restricted to a maximum 25% of own contributions, aligned with partial-withdrawal limits.

Before deciding, readers typically compare it with partial withdrawal.

This difference is essential because one is a debt obligation and the other is a reduction in the retirement pot.

What The New Rule Delivers?

The core change is the formal permission for a subscriber to seek financial assistance from a regulated lender and allow a lien on the pension account, within limits.

In the exposure draft issued earlier, PFRDA had described how the subscriber may create a security arrangement in favour of the lender, and the lender may mark a lien or charge to the extent of assistance provided.

Operationally, PFRDA has also published a “Response to Stakeholders” document that reiterates the provision: financial assistance can be taken and the lien/charge can be marked up to 25% of own contributions, within partial-withdrawal limits, with operational aspects to be governed separately.

This also lands alongside broader exit flexibility changes. The Economic Times reported on December 16, 2025 that non-government subscribers can withdraw up to 80% as lump sum in several exit scenarios, with at least 20% going to annuity in specified cases, and it listed slabs such as ≤ ₹8 lakh allowing 100% withdrawal at normal exit for non-government subscribers.

How The Story Built Up?

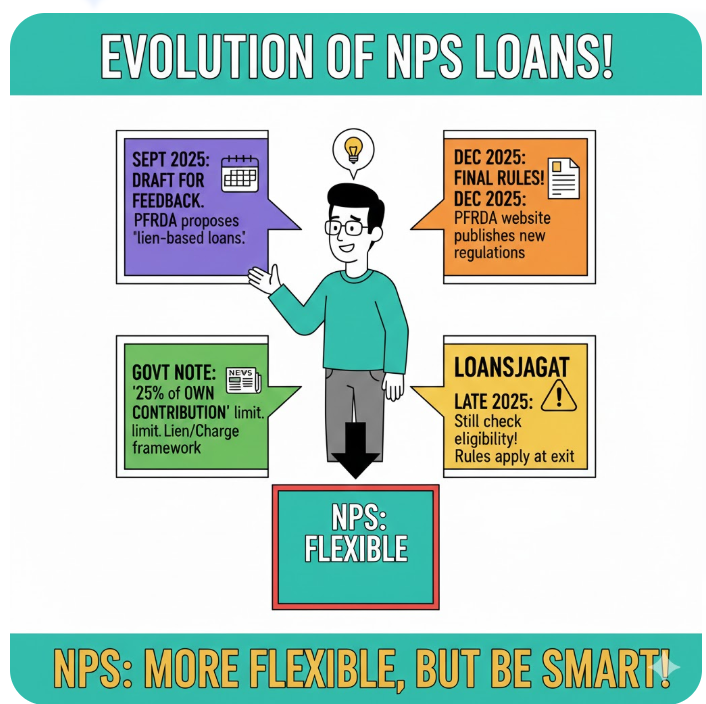

The loan-against-corpus feature did not appear overnight. PFRDA first issued the Exposure Draft dated 16 September 2025, inviting stakeholder comments on proposed amendments, including allowing a lien-based financial assistance facility.

After feedback, the amended regulations were published on 16-12-2025 on PFRDA’s website.

The government’s public note on key amendments summarised the change and clearly stated the 25% of own contribution ceiling and the lien/charge framework.

In news explainers and consumer-focused write-ups that followed, LoansJagat’s article (published in late 2025) flagged that despite higher flexibility for certain groups and scenarios, NPS is still rule-based and slab-driven at exit, and readers need to track eligibility conditions carefully.

Here is the clean timeline readers can pin to.

This chronology matters because it shows the rule is in place, while lender products and detailed operational processes may still vary by institution.

What Stakeholders Are Saying?

Abhishek Soni (CEO and Co-founder, Tax2win), quoted by Upstox on February 20, 2026, says the lien-based loan is not treated as a withdrawal and so carries no immediate tax liability at the time of taking the loan, but he cautions it can backfire if repayment becomes difficult or disrupts retirement planning discipline.

On the institutional side, the government’s amendment summary frames it as a regulated-lender facility with a clear 25% cap and further governance via PFRDA guidelines.

Conclusion

A loan against NPS can work for tight, short-term needs if repayment is predictable and the borrowing is capped. Used casually, it can weaken retirement adequacy and create avoidable debt pressure.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article