By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key takeaways:

A Provident Fund (PF) is a savings plan that helps workers save for retirement and provides financial security for their future. Both the employer and the employee contribute a portion of the employee's salary every month.

For example, Ramesh receives a monthly salary of ₹20,000. He contributes 12% of his income, amounting to ₹2,400, to his Provident Fund (PF). His employer matches this contribution with an equivalent amount. Consequently, a total of ₹4,800 is deposited into Ramesh's PF account each month, thereby facilitating his efforts to save for a secure retirement.

Table:

The table presented below outlines the annual savings that can be achieved through these contributions. It is important to note that this figure does not account for any interest that may accrue over time.

This table shows that in just one year of saving regularly, you can build a solid amount of ₹57,600. With the power of compound interest, this amount will grow even more over your career, helping you create a strong fund for retirement.

This safe savings plan provides crucial financial security. It allows people like Ramesh to access their money during retirement or in times of need, such as when facing unemployment or medical expenses. In this blog, you'll learn how to check your PF balance and find out the basics of PF.

Read More - How to Find the PF Account Number

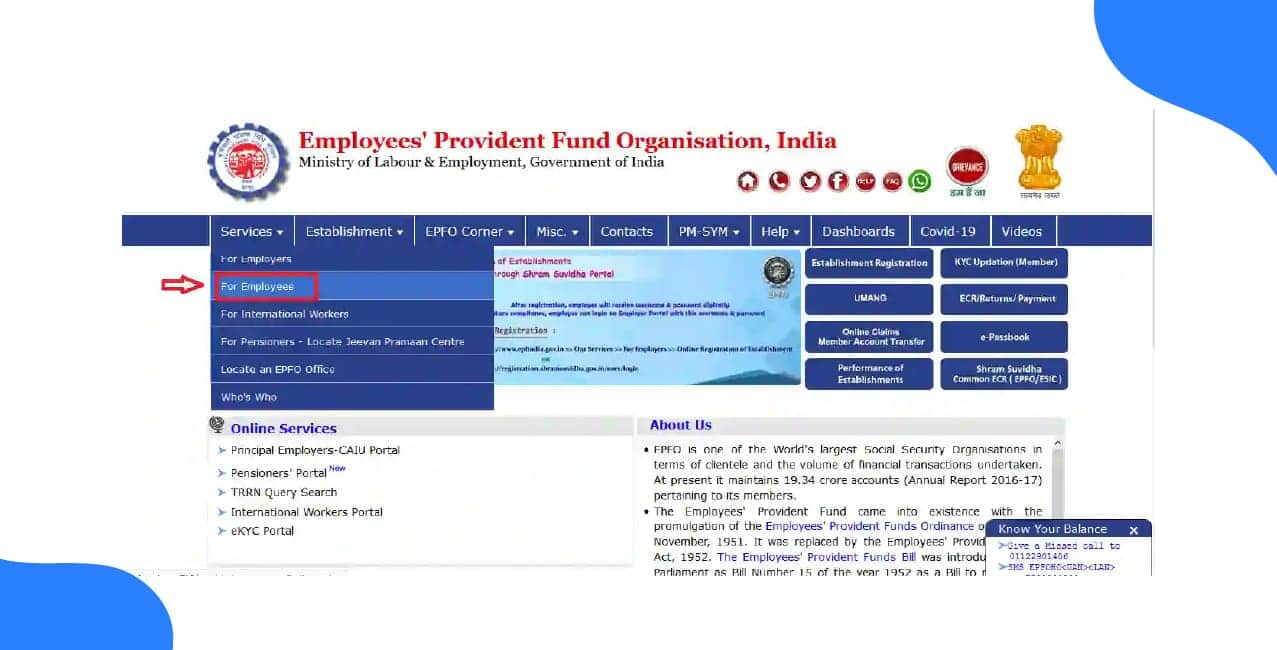

How To Know PF Balance?

To keep track of your long-term savings and make innovative financial plans, it’s essential to know your Provident Fund (PF) balance. This helps you figure out how much money you’ll have for retirement, including the interest you earn and the amounts contributed by you and your employer.

Let’s take a look at Mayank’s story. He’s a 30-year-old professional who earns ₹25,000 in Dearness Allowance (DA) on top of his base salary. Mayank saves carefully and regularly:

If he continues this for 10 years without any salary hike, his principal amount would be ₹7,20,000. However, with an estimated 8% annual compound interest, this corpus is projected to grow to an impressive ₹11,00,000-₹12,00,000.

Mayank ensures this growth continues by not making premature withdrawals, making extra contributions through the Voluntary Provident Fund (VPF), and regularly checking his balance via the UMANG app to stay informed.

You can easily check your balance just like Mayank. To use online and SMS services, you’ll need your Universal Account Number (UAN) and a mobile number linked to your Aadhaar and PF account.

Here’s a simple table with the most popular ways to do it:

Every employee can easily keep track of their savings thanks to a simple and user-friendly system.

( The EPFO offers many options to stay updated, whether you prefer checking your detailed passbook online or getting a quick balance update via SMS.)

Regularly checking your PF balance is essential for thoughtful financial planning and helps you stay on target for your retirement goals. It’s not just about knowing a number; it’s about understanding your financial health.

Now that you know how to check your balance, let’s look at why it’s so important to keep an eye on your PF account.

Bonus Tip: Contact your employer to update your number in the EPFO records to access online services.

You should regularly check your Provident Fund (PF) balance to secure your finances. This simple step ensures your retirement savings are growing as they should. It also helps you find any problems early, keeping your future safe.

Also Read - EPFO Launches Revamped ECR To Streamline Return

Example:

Maumita earns ₹30,000 a month and puts ₹3,600 into her Provident Fund (PF) with the help of her employer. After two years, she checked her balance and saw it was only ₹1,40,000. She expected it to be around ₹1,70,000.

Fortunately, she acted quickly and found out that her employer had missed three months of contributions in her passbook. By catching this mistake early, she saved herself from a significant financial loss in the future.

Here are the main reasons why this habit is essential:

These reasons show how this habit can make a big difference in your life!

To keep track of your balance, you need to manage your finances rather than simply monitoring them actively. This will help you protect your contributions, ensure your employer is accountable, and keep you focused on your long-term goals.

The key takeaway for managing your provident fund is to stay observant. With this, we wrap up our discussion.

Bonus Tip: This could indicate delayed contributions by your employer, an inactive UAN, or incorrect KYC details.

Your Provident Fund is the key to a secure and carefree future. It’s not just a monthly deduction; it's your retirement savings. By knowing what it is, checking your balance regularly, and understanding its importance, you take control of your financial future.

Your hard-earned money is growing quietly over time. With a bit of attention today, you can build a strong fund for your future dreams. Start checking your PF now, it's a small step towards a brighter tomorrow!

Can I check the EPF balance online if my EPF account is inactive?

Yes, you can check your EPF balance even if it is inactive, as long as you’re under 58 years old.

Can I check the EPF balance of my EPF account created from previous employment?

Yes! When you log in to the EPF portal, you’ll see all your EPF accounts linked to your UAN. Just choose the member ID of your old account to check your balance.

When does the EPF balance get updated?

Your EPF balance gets updated in your passbook within 24 hours after you contribute. So, you need to wait at least a day before checking your EPF account.

.

Can I check my PF balance without UAN?

No, UAN is mandatory for online, SMS, or missed call services. Alternatively, ask your employer for details.

Other Related Pages | |||

3. Log in with your UAN and password.

4. Select your member ID to view the passbook and balance.

How to Use a Business Loan for Digital Transformation in 2025 |