Bihar Student Credit Card : Updated Guide for Students

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Priya is a Bihar student who dreams of pursuing a BTech degree. She cannot pay ₹3 lakh for her BTech degree. Now, Priya can avail herself of a loan of ₹3 lakh at just 1% interest, especially available to female students, through the Bihar Student Credit Card (BSCC) scheme.

With the BSCC scheme, Priya can enjoy her education without financial concerns. She could use the loan for tuition, books, study materials, and hostel fees.

After completing the 4-year course, Priya can begin paying back the loan. The repayment term varies from 5 to 7 years in duration. If Priya chooses the term to be 5 years, she would pay ₹3 lakh along with ₹3,000 as interest, which would add up to ₹3,03,000. Her monthly EMI would then be around ₹5,050, leaving her adequate time to focus on her studies without any tension.

The Bihar government has hailed the initiative for particularly assisting students from backward classes and SCs in accessing higher education. Chief Minister Nitish Kumar has been highly appreciative of this move.

What is Bihar Student Credit Card?

The Bihar Student Credit Card Yojna, or "credit card scheme for the students of Bihar," is a government program that helps the financially deprived students of Bihar to pursue further education after 12th. It provides a loan of up to ₹4 lakhs that can be used for the charges related to education, such as tuition fees, books, study materials, and much more. Interest rates are low, especially for female, transgender, and disabled students, so it is inexpensive.

Read More – West Bengal Student Credit Card

Students will not have to start repaying the loan after they complete the course and join a job. To avail of the loan, students need to be permanent residents of Bihar and must have passed their 12th grade from a school that is recognised in the state. The scheme ensures that those students who need financial support can attend higher education, thus smoothening out their achievement of education without the burden of upfront repayments.

Features of the Bihar Student Credit Card

Here’s a table summarising the major features of the Bihar Student Credit Card (BSCC) scheme:

Feature | Description |

Loan Amount | Students can borrow up to ₹4 lakh to cover their education expenses. |

Interest Rate | The interest rate is 1% for female students, transgender students, and Divyang (disabled) students, making it more affordable for these categories. |

Repayment | Repayment starts only after completing the course and getting a job, allowing students to focus on their studies without worrying about repayments. |

Collateral | No collateral or security is required to obtain the loan, so no property or asset is needed from the student. |

Moratorium Period | Repayment begins one year after completing the course or five years after loan disbursement, whichever is earlier, giving students time to settle into work. |

Recovery Procedures | The loan recovery process is flexible and manageable for students, as the government provides the loan. |

Benefits of Bihar Student Credit Card:

- The loan can cover expenses like books, laptops, tuition fees, and hostel fees.

- It can be used for general, polytechnic, and technical courses.

- If the hostel is unavailable, the loan can be utilised to rent accommodation.

- A loan is also applicable towards livelihood expenditure.

- Financial support is available to purchase books and laptops or pay fees.

- The loan interest rate is 1% for Divyang, transgender, and female students.

Eligibility Criteria for Bihar Student Credit Card:

To be eligible for the Bihar Student Credit Card (BSCC) scheme, you must fulfill these requirements:

- Be a resident of Bihar

- Have passed the 12th standard in Bihar

- Be between the ages of 18 and 25

- Have a family income of less than ₹6 lakhs per year

- Have scored at least 50% in the 12th standard

- Be admitted to an educational institution recognized by the regulatory authority

- Be enrolled in a course at an authorized institute

- Complete the entire course

Documents needed for Bihar Student Credit Card:

- Application Form: You will need a completed common application form

- Identification: You need an Aadhaar card, PAN card, and proof of residence; acceptable documents would be a voter ID, a valid passport, a valid DL, or any valid ID.

- Academic Records: Copy of mark sheets and certificates of Class 10th and 12th

- Admission Proof: Proof for admission to the authorized institute

- Financial Documents: Income certificate, bank statement, and income tax returns

- Scholarship Proof: Copies of scholarship award letters

- Course Structure: Approved course structure

- Fee Schedule: Details on the fee schedule

- Photographs: Recent photographs of the student, parents, or guarantor

How many courses come under the Bihar Student Credit Card?

The Bihar Student Credit Card scheme supports many courses, including professional, engineering, and diploma courses.

Professional Courses:

- Bachelor of Business Administration (BBA)

- Bachelor of Computer Applications (BCA)

- Master of Business Administration (MBA)

- Master of Computer Applications (MCA)

- Bachelor of Technology (B.Tech)

- Bachelor of Pharmacy (B.Pharma)

- Bachelor of Science in Agriculture (B.Sc Agriculture)

- Bachelor of Science in Nursing (B.Sc Nursing)

- Bachelor of Science in Biotechnology (B.Sc Biotechnology)

- Bachelor of Science in Hospitality & Hotel Management

Engineering Courses:

- B.Tech in Computer Science Engineering (CSE)

- B.Tech in Civil Engineering

- B.Tech in Mechanical Engineering

- B.Tech in Electrical Engineering

- B.Tech in Electronics & Communication Engineering (ECE)

Diploma Courses:

- Diploma in Computer Science

- Diploma in Mechanical Engineering

- Diploma in Electronics Engineering

- Diploma in Electrical Engineering

- Diploma in Food, Nutrition/Dietetics

- Diploma in Food Processing/Food Production

- Diploma in Hotel Management

- Diploma in Food & Beverage Services

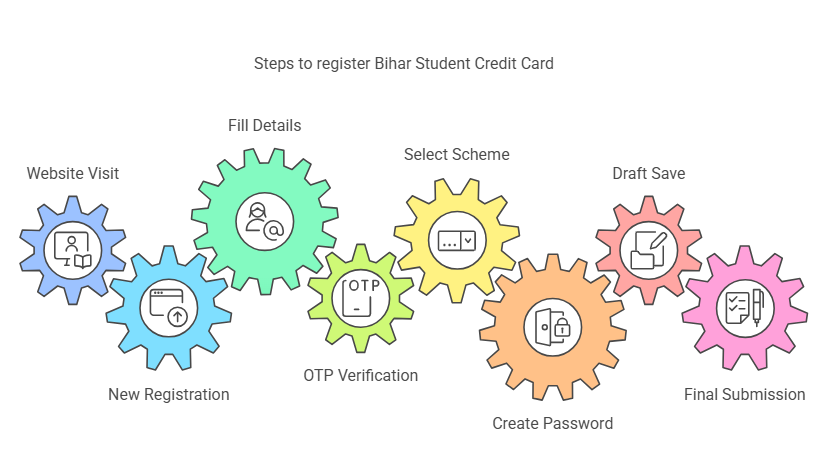

How to register for a Bihar Student Credit Card?

- Visit the 7Nishchay Bihar website.

- Click on the ‘New Applicant Registration’ option.

- On the next page, fill in the details (like first name, middle name, last name, Email ID, aadhar card number, and mobile number), and click ‘Send OTP.’

- Enter the OTP received at your registered mobile number and email ID.

- Select the ‘BSCC’ as your desired scheme and click ‘Submit.’

- Create your new password and click on the ‘Submit’ option.

- Fill in your details and click on ‘Save as Draft.’

- Click on the ‘Submit’ button.

- Now visit your nearest DRCC office for document verification.

- The DRCC will schedule an appointment and send an email/SMS with the visit date.

- Visit the DRCC with self-attested documents and submit them to the MPA for verification.

- After verification and loan approval, the DRCC sends an SMS/email informing you to collect the ‘Student Credit Card’ and loan sanction letter.

- Visit the bank to complete documentation after collecting the credit card and sanction letter from the DRCC.

- The bank disburses the loan, and the bank notifies the DRCC.

How to log into Bihar Student Credit Card page?

- Visit the 7Nishchay Bihar website.

- Enter your username, password, and captcha, and click on ‘Login.’

- You’ll be redirected to the homepage.

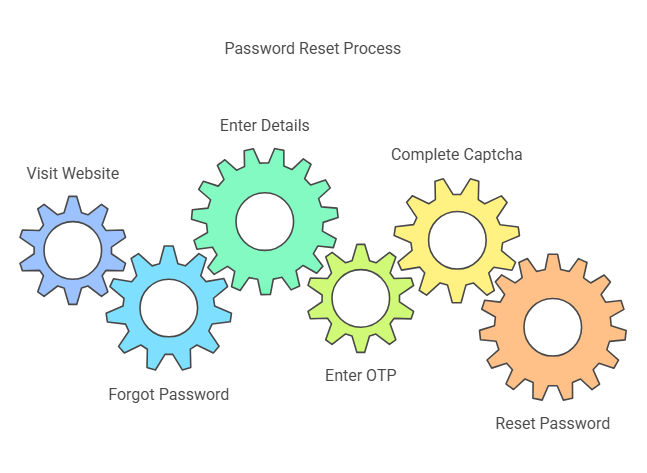

How to reset your password for the Bihar Student Credit Card page?

- Visit the 7Nishchay Bihar website.

- Click on the ‘Forgot Password’ option.

- Enter your mobile number and email ID, and click the ‘Send OTP’ option.

- Enter the OTP received using your registered mobile number and email ID.

- Enter the captcha and click on ‘Submit.’

- Reset your password and click on ‘Submit.’

- This is how you can reset your password.

Loan repayment:

The amount is paid through equated monthly installments, or EMIs. The repayment of the Bihar Student Credit Card loan amount only occurs after the moratorium period. The moratorium period is a delay in repayment, one year after completing the course or five years from when the amount was disbursed, whichever is earliest.

Repayment Period:

Once the moratorium period is completed, students are liable to repay their loan for 5 to 7 years. The repayment period is 5 to 7 years, based on the loan tenure sanctioned.

Repayment Options:

Students can repay loans via cheque, Demand Draft (DD) and Electronic Clearing System (ECS), National Automated Clearing House (NACH) and any other mode of repayment permitted by the bank.

Remedial Processes:

Since the government provides loans, it is lenient in the recovery process and makes it easier for students. Sometimes, the government even relaxes the amount remaining.

For instance, a student borrows ₹2 lakh under the Bihar Student Credit Card scheme. Once he finishes his course by 2025, he can pay back by the end of the fifth year of disbursement, which is 2030. He will start paying back after the moratorium period by cheque or ECS for 5–7 years. The government will even write off the remaining balance sometimes.

Student Loan Disbursement Process

The loan will be disbursed to the student's account after the student has verified the documents needed. Once verified and approved, the loan amount will be credited. The procedure is followed under the government's standard operating procedure, keeping the process very transparent and orderly.

Also Read – How to Take Education Loan in India

Loan Utilization

The amount borrowed will be utilised for the student's educational expenses. The amount is liable to be used for books, tuition fees, hostel charges, and all other necessary expenses for the student's education. The loan would be disbursed in installments per the academic year and approved course structure.

The details of loans disbursed for the last couple of years are as follows:

2016-17: ₹5,00,000

2017-18: ₹6,00,000

2018-19: ₹7,00,000

2019-20: ₹8,00,000

2020-21: ₹9,00,000

Note: The amount will be divided proportionally based on the financial year and the student's timetable.

Loan Terms:

1. The loan will bear interest at 2% over the base rate of the student loan scheme.

2. Government interest subvention for the loan

3. Government interest subvention on the loan will be provided subject to the following conditions:

4. Interest subvention is during the moratorium period or when repayment commences; if the student is not eligible for the subvention, the interest will continue to run.

5. If there is a default on the loan, the concerned authorities will impose a penalty. If the borrower fails to repay the loan, it will be classified as a Non-Performing Asset (NPA), and legal actions may be taken against the borrower.

6. In the case of certifying, verification needs to be completed by the borrower. It will be notified to the relevant authorities, who then issue a certificate of completion on the loan formality and schedule of repayment.

7. A CIBIL score is required at the time of sanctioning a loan. A good CIBIL score of more than 700 ensures smooth processing, but scoring below that is not easy as approval may turn difficult.

8. The applicant has to submit a document where he gives proof of income and his family details as part of loan verification. All the papers will be verified before providing the loan.

9. If a borrower fails to repay, authorities take strict measures to recover the amount entrusted through legal action and/or liquidate the assets concerned, if necessary.

10. The applicant must present the documents and certificates to prove the loan requirements are fulfilled. The loan might be disqualified if the applicant fails to provide the necessary documents.

Major takeaways

- It is a loan scheme that benefits economically weaker students of Bihar towards higher education.

- It can be availed of for all expenditures of education, which is not necessarily limited to fees only.

- Due to the reduced interest rate of this scheme, especially for some of the categories, it has been seen to be of much attraction

- The student shall maintain satisfactory grades for further availing of the loan facility.

Customer care details:

For assistance with the Bihar Student Credit Card, call customer care at 1800 3456 444 or email spmubscc@bihar.gov.in.

Conclusion

An excellent opportunity for students in Bihar, the Bihar Student Credit Card (BSCC) helps them pursue their higher education without thinking about money to spend; for loans up to ₹4 lakhs, low interest rates are provided with the plan covering fees for college tuition, books, and even some miscellaneous items.

Repayment plans start only after completion of the course, and this flexible system will help students to have their minds clear on their studies. Especially beneficial for girls, transgender, and disabled students, this scheme helps economically disadvantaged families achieve their dreams. Thanks to the Bihar government’s initiative, many students can access higher education and create brighter futures.

FAQs Related to the Bihar Student Credit Card:

Q1: Who can be denied a credit card?

Credit card applications are often rejected if the applicant has a low credit score. A bad credit score is one of the most important reasons behind the rejection of credit card applications and other loans.

Q2: Can students increase their credit limit?

Yes, if you increase your income, then you can increase your credit limit. You can observe from your credit report about the chances of its approval or not. The credit card companies check your credit ability for any credit limit increase.

Q3: Do credit cards have daily limits?

Yes, they generally have a daily spending limit that is often less than the available credit limit. This limit can also be considered as one of the fraud prevention measures set by a credit card issuer.

Other Credit Cards | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article