Big Alert: 90% People Don’t Know This RBI Cheque Rule

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

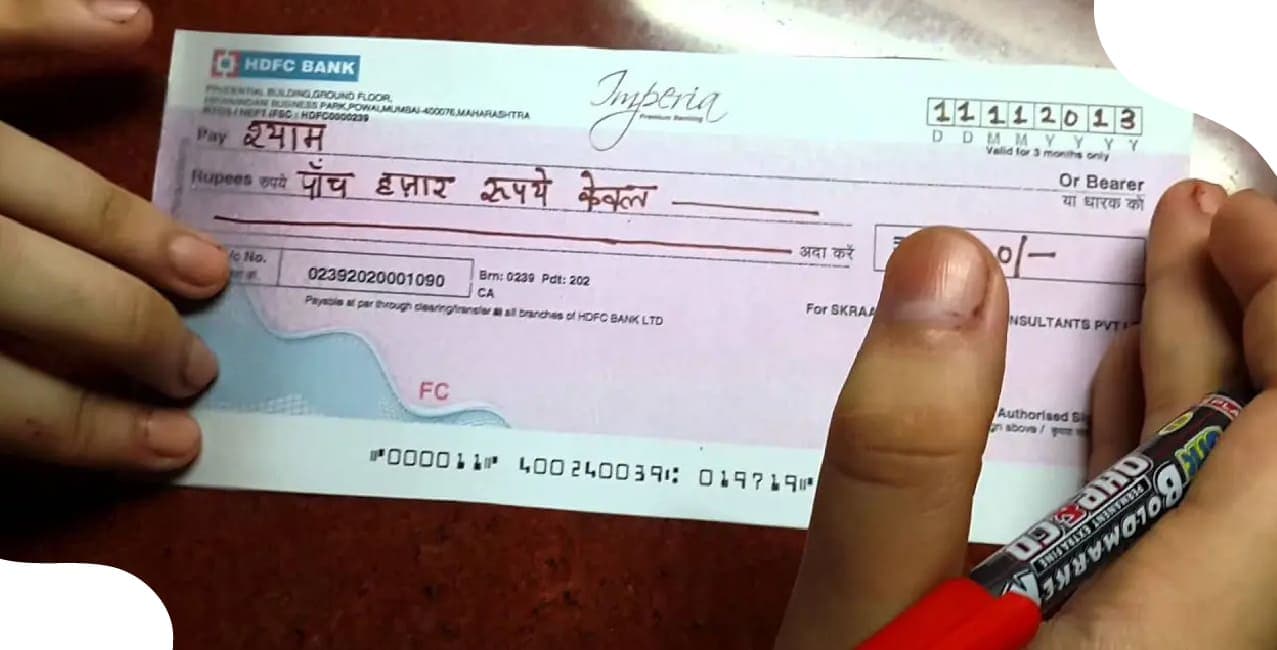

In India, cheques are still widely used for personal and professional payments, even though digital transactions have become more common. But very few people know that a small mistake with your signature on a cheque can make you lose the money in your bank account.

Many employees have signed a blank cheque at some point to let their organisation fill in the account details for salary credit. Usually, this signature is placed on the front of the cheque, in the box marked “Authorised Signatory.”

However, some individuals unknowingly or casually sign on the back of the cheque. This is not just incorrect; it can be highly risky. As per RBI guidelines, signing on the back of a cheque (other than in specific cases of endorsement) can be misused, and the account holder may end up losing funds.

Why Do People Sign on the Back of the Cheque?

The confusion arises because cheques are still seen as complex instruments by many people. Some believe that signing on the back is an additional security measure, while others simply follow what they’ve seen colleagues or family members do. In rural areas and among first-time account holders, the practice is more common because of limited awareness of banking procedures.

Another reason is the concept of cheque endorsement. Traditionally, if a person wanted to transfer the right to receive payment to someone else, they would sign at the back of the cheque. But most ordinary bank customers do not fully understand this, and they mistakenly use the back of the cheque for routine signatures.

Key reasons why people sign on the back of cheques include:

- Misunderstanding cheque endorsement practices.

- Lack of financial literacy and awareness of RBI rules.

- Following outdated practices seen in older generations.

- Belief that signing twice (front and back) adds extra security.

Unfortunately, this misconception can give fraudsters an open opportunity to misuse the cheque, as the back signature acts as an authorisation to

transfer ownership.

Read More – RBI Introduces New Rules for Faster Cheque Clearance Within Hours

What Is the Difference Between a Cheque Bearer and a Cheque Order?

To understand why signing in the wrong place is risky, it is important to know the difference between bearer cheques and order cheques.

Imagine two situations:

- You write a cheque for your friend Ramesh and do not strike out the word bearer. This means anyone who physically holds the cheque, not just Ramesh, can cash it. It works like giving a ₹500 note; whoever has it, owns it.

- On the other hand, if you cross out the bearer and write order, only Ramesh himself, whose name is on the cheque, can withdraw the money. Even if someone else finds the cheque, they cannot encash it without Ramesh’s identity verification.

The following table explains the difference:

This table shows that bearer cheques are highly risky compared to order cheques. Signing on the back of a cheque essentially gives it the power of a bearer cheque if misused, which is why the RBI repeatedly warns against this practice.

What Happens If I Don’t Sign the Cheque?

A cheque without a signature is incomplete and automatically invalid. The bank will simply reject it, and no transaction will take place. While this might seem like a safe mistake compared to signing on the back, it can still cause delays in payments, penalties for bounced cheques, and a negative impression in professional dealings.

In fact, banks categorise unsigned cheques as dishonoured instruments. If the cheque was meant for loan repayment, rent payment, or business transactions, the payer could also be liable for penalties. Under the Negotiable Instruments Act, 1881, repeated dishonouring of cheques can even lead to legal consequences.

So, while an unsigned cheque doesn’t immediately put your money at risk, it can damage your credibility and result in financial inconvenience.

Also Read - The Role of RBI and NPCI in Safeguarding India's Financial Infrastructure

My Signature on the Cheque Doesn’t Match the Documents. What to Do?

Another common issue faced by account holders is signature mismatch. This usually happens when:

- People change their signature style over time.

- They use a hurried or casual signature on cheques.

- The signature on the bank’s records (submitted years ago) differs from the current one.

If your cheque signature does not match the specimen signature stored in the bank’s system, the cheque will be rejected. This is a protective mechanism against forgery.

What should you do if this happens?

- Update your signature at the bank: Visit your branch with ID proof and formally register your new signature.

- Maintain consistency: Always sign cheques in the same style to avoid mismatch errors.

- Avoid dual signatures: Some people try to add flourishes or extra strokes to “improve” their signatures. This inconsistency can cause rejection.

Remember, consistency in signature is as important as writing the correct payee name or amount. Without it, your cheque remains invalid.

Conclusion

Cheques may seem old-fashioned in today’s UPI and digital banking world, but they still play a crucial role in salaries, rent agreements, business transactions, and legal settlements.

A single mistake, such as signing on the back instead of the front, can lead to serious financial loss. RBI guidelines are clear that endorsements should only be used in specific cases and not in everyday cheque writing.

To stay safe:

- Always sign in the space provided at the front.

- Prefer order cheques over bearer cheques for higher security.

- Ensure your signature matches the one in the bank’s records.

Financial literacy in these small details can prevent fraud, save time, and protect your hard-earned money. In banking, a signature is not just a formality; it is the shield guarding your account.

Other News Pages | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article