Future EMI Cut Becomes Sales Pitch For Small Home Loans

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Small home loans are turning into a high-volume play, with lenders using rate-cut hopes and policy support to pull first-time buyers into the market.

Small home loans usually refer to lower-ticket housing loans, largely in the ₹5 lakh to ₹25 lakh range, taken by first-time buyers in smaller cities, semi-urban belts and fringe urban clusters.

The segment is getting fresh attention because affordable homes remain underfinanced even as property prices climb. Under PMAY-U 2.0 operational guidelines dated 1 September 2024, an affordable house is defined as one priced up to ₹45 lakh, with carpet area up to 60 sq m in metros and 90 sq m in non-metros.

Why Small Home Loans Are Becoming A New Growth Bet?

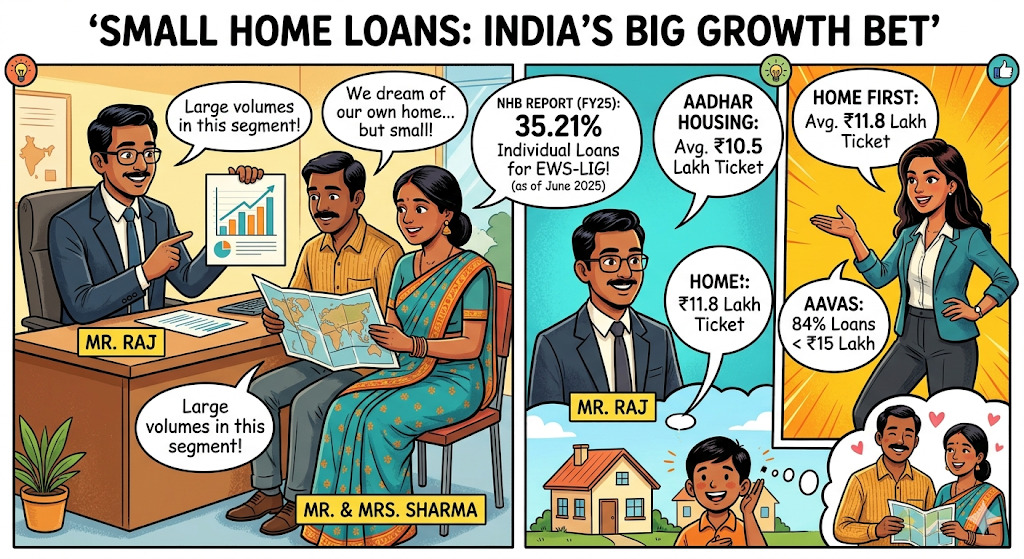

Lenders are chasing this segment because it still offers volumes. National Housing Bank’s Annual Report 2024-25, released on 13 January 2026, said the EWS-LIG segment accounted for 35.21% of individual home loan disbursements as on 30 June 2025.

Read More - Good Days For Home Loan Borrowers

Specialist lenders show how small these loans are on the ground. Aadhar Housing Finance reported an average ticket size of ₹10.5 lakh, Home First reported ₹11.8 lakh, and Aavas said 84% of its active loans were below ₹15 lakh.

This rush is also linked to changes in the housing market. Reuters reported on 12 March 2026 that luxury homes made up 63% of residential sales in 2025, up from 53% in 2024, while demand for homes priced below ₹1 crore fell 31%.

That leaves banks and NBFCs looking at smaller borrowers for retail growth. LoansJagat, in its 4 December 2025 report, also said lower rates were supporting borrower interest in home loans.

How The EMI Story Reached Here?

The sales line now goes beyond eligibility and moves to future repayment comfort. After cumulative rate cuts of 125 bps since February 2025, many lenders are pitching floating-rate home loans as products that may become easier on the wallet if rates soften again.

Reuters reported on 29 January 2026 that economists expected policy rates to remain at 5.25% through 2026. Earlier, The Economic Times reported on 7 February 2025 that a 25 bps cut could reduce EMI by about 1.8% on a 20-year loan.

That said, a future EMI cut is not locked in. Reuters reported on 12 March 2026 that retail inflation rose to 3.21% in February, and economists flagged oil-led risks. So the pitch is useful for selling, but the next cut still depends on inflation and growth data.

What Stakeholders Are Saying?

Also Read - RBI Keeps Repo Rate Unchanged

Borrowers want lower monthly outgo, while lenders want scale in a segment where demand is still broad. The Economic Times reported on 2 March 2026 that Governor Sanjay Malhotra said rates could stay “around this level or lower” for a long time, barring shocks. That comment has only added to sales chatter around future EMI relief.

Conclusion

Small home loans are now a serious retail lending play, not a side segment. For banks and NBFCs, the next EMI cut may still be uncertain, but the sales pitch has already begun.

Related Financial News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article