Repo Rate Up, Home Loan Cost Up: Why Borrowers Feel It Fast

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

A repo rate rise can lift home loan costs quickly, especially for repo-linked borrowers. The reset window is short, so EMIs react sooner.

Home loan borrowers usually do not see a rate change on the same day the RBI announces a policy decision. But many feel the impact fairly quickly, especially on repo-linked or externally benchmarked loans.

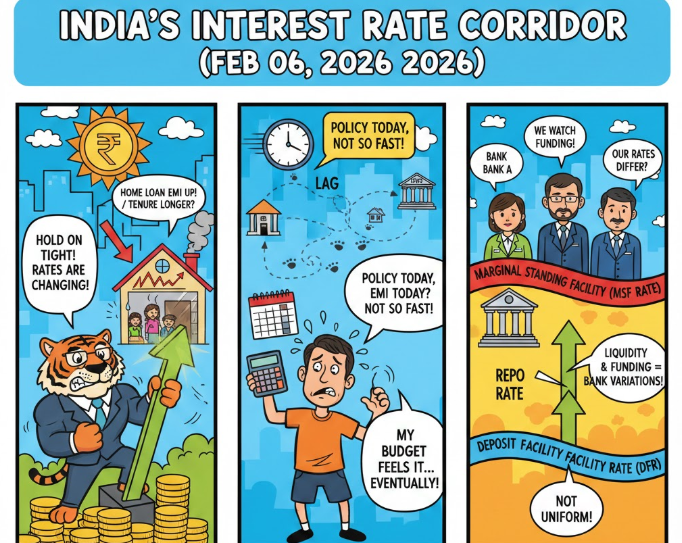

On February 06, 2026, the RBI kept the repo rate unchanged at 5.25%, with SDF at 5.00% and MSF at 5.50%, according to multiple post-policy reports. Even when rates are unchanged, borrowers track the repo closely because any future hike can feed into floating rates at the next reset, and that reset can come sooner than people expect.

What Borrowers Are Facing Right Now?

The issue is timing and predictability. When repo goes up, a borrower on a floating-rate home loan can see the interest rate move up at the next reset, followed by a higher EMI or longer tenure. Repo-linked borrowers typically face quicker pass-through than borrowers on older benchmarks.

A large part of the confusion comes from assumptions like “policy today, EMI today”. That is rarely true, but the lag can still be short enough to feel immediate in household budgeting. Recent coverage has flagged that lenders also watch liquidity and funding conditions, so transmission is not always uniform across banks.

Read More : Inflation Falls Below RBI Target Again

Before looking at EMI impact, here is the interest rate corridor that was widely reported after the February 06, 2026 policy decision.

This corridor is what markets and lenders anchor to, and it frames where lending rates can head next when policy shifts.

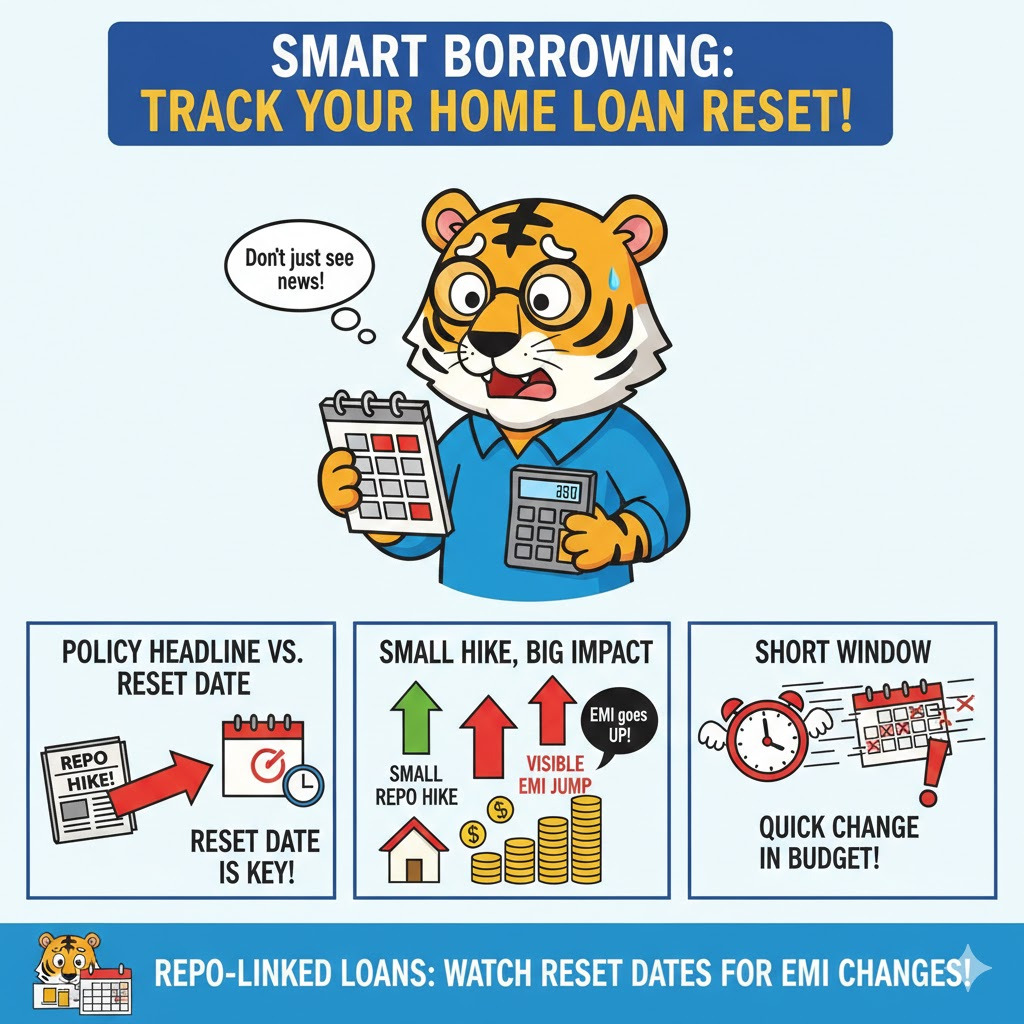

How Repo-Linked Loans Pass Through Faster?

Repo-linked home loans generally reset faster, so the borrower sees changes sooner after a repo hike. MCLR-linked loans, on the other hand, can reprice with longer reset cycles, so the impact can show up later. One lender explainer notes MCLR resets are often 6 to 12 months, while repo-linked rates can revise every 3 months, making the repo impact visible sooner for many borrowers.

The impact becomes clearer with a simple example. Assume a ₹50,00,000 loan for 20 years. If the rate moves up by 0.25% (25 bps), the EMI jump is not small.

That is an increase of roughly ₹794 to ₹795 per month, and it adds up over time if the higher rate persists. Borrowers often experience this as an EMI hike, or a tenure stretch, or both, depending on the lender’s reset and repayment setting. This is also why “repo unchanged” headlines do not automatically mean every borrower is safe, because the next move is what changes the monthly outgo.

What Changed Earlier and Why Borrowers Feel It More Today

The sharper borrower reaction today is tied to how retail lending moved towards external benchmarks in recent years, improving policy transmission. On the news flow side, the February 2026 policy was positioned as a pause with a neutral stance, with commentary linking future moves to inflation and growth outcomes.

Also Read : Bank Rate vs Repo Rate

In fact, Reuters reported on February 20, 2026 that the minutes showed a majority view that current rates were appropriate, citing buoyant growth and tame inflation, while still leaving room for action if data changes.

That tone shapes borrower expectations. If households think the rate cycle is turning tighter, even a small repo move becomes a trigger to prepay, refinance, or push for an EMI restructure.

LoansJagat’s February 09, 2026 explainer also highlighted that repo-linked borrowers may not see an instant EMI change on the policy day itself, but resets and bank spreads decide when the EMI actually changes.

What Policymakers, Banks, Analysts Are Saying?

Policy coverage after the February decision repeatedly pointed to a neutral stance and a data-led approach ahead.

The Economic Times reported that the RBI signalled calibrated liquidity management to support policy transmission, which lenders track closely for pricing. Mint’s live policy coverage also clearly listed the policy rates and noted the unchanged corridor, which feeds into market expectations on borrowing costs.

Conclusion

Repo-linked borrowers should track the reset date, not just the policy headline. A small repo hike can translate into a visible EMI jump within a short window.

Related Financial News | |||

How RBI’s Repo Rate Decision Affects Borrowers and Depositors | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article