By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

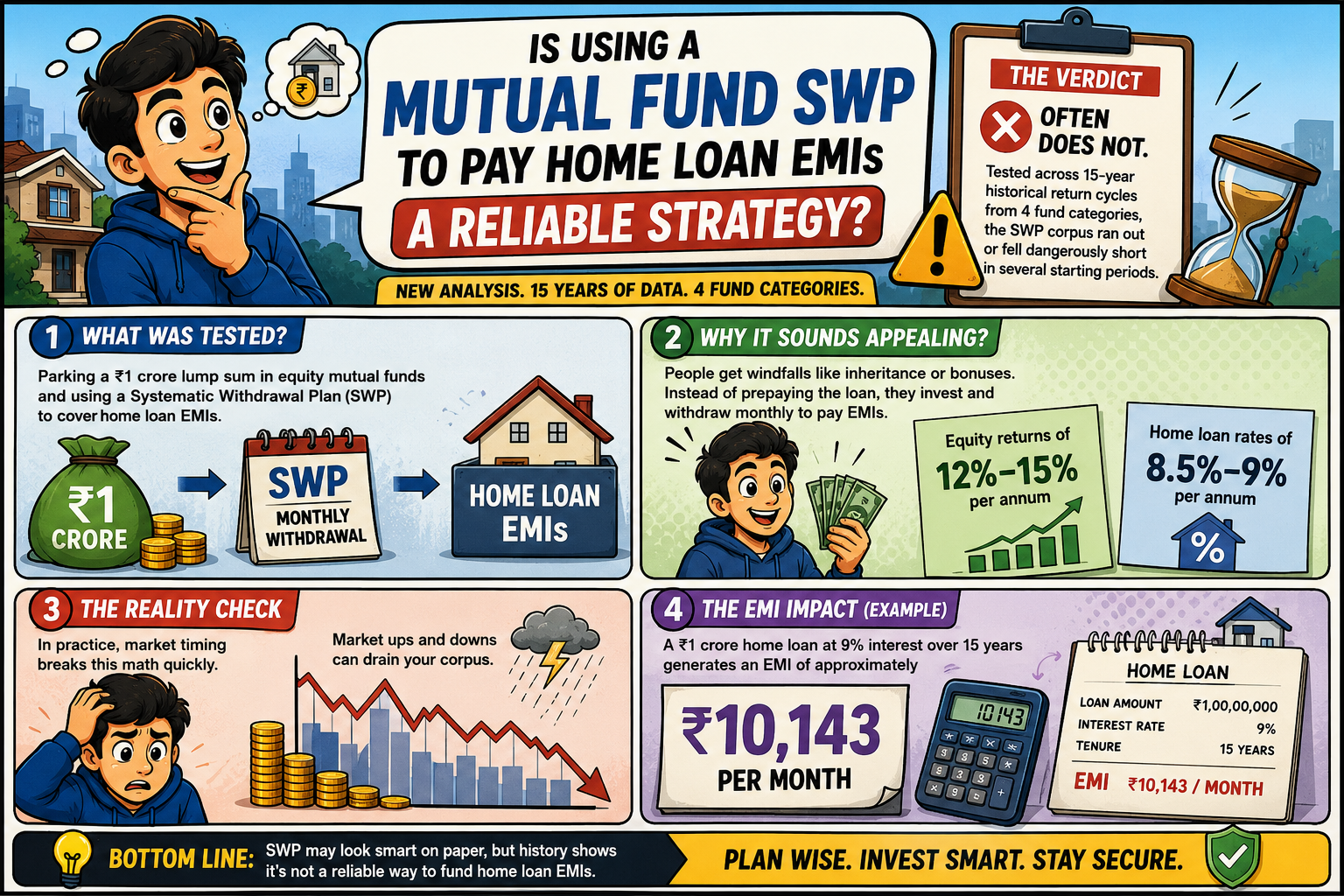

A new analysis tested whether parking a ₹1 crore lump sum in equity mutual funds and using a Systematic Withdrawal Plan (SWP) to cover home loan EMIs actually works. The verdict is that it often does not. When tested across 15-year historical return cycles from 4 fund categories (large-cap, mid-cap, hybrid, and large & mid-cap), the SWP corpus ran out or fell dangerously short in several starting periods.

The strategy appeals to borrowers who receive windfalls like inheritance or bonuses. Instead of prepaying the loan, they park money in equity funds and withdraw monthly to cover EMIs. On paper, equity returns of 12% to 15% per annum look attractive against home loan rates of 8.5% to 9%. In practice, market timing breaks this math quickly. A ₹1 crore home loan at 9% interest over 15 years generates an EMI of approximately ₹10,143 per month.

The gap between average returns and actual SWP outcomes is the core problem. 3 structural flaws make this strategy fragile:

A market fall in Year 1 or Year 2 forces the investor to sell more units at lower prices to maintain the same EMI. This permanently reduces the corpus. Even a recovery in Year 3 or Year 4 cannot fully repair the damage. A key concern is that the rate of withdrawal must remain lower than the rate of growth, and in a country where inflation runs high, a 4% buffer may not be enough.

According to LoansJagat’s home equity report, the average price-to-income ratio in India is 8.8. A typical Indian family needs nearly 9 years of full income to afford a home. In Mumbai, that number jumps to 15.1 years. In Delhi, it is 12.3 years. This affordability gap is exactly why borrowers get attracted to strategies like SWP-funded EMIs. The math looks good. The market reality does not.

Financial planners point to 1 core principle: fixed liabilities should not be funded by variable assets. If you have the funds, prepaying the home loan principal directly eliminates a certain liability. EMIs are constant and definite, but mutual fund returns are neither assured nor guaranteed.

Experts suggest that if the SWP route is used at all, the withdrawal rate must be meaningfully lower than the portfolio’s growth rate, with a 5% to 6% buffer recommended. Hybrid funds, which historically return 10% to 11% per annum, carry lower volatility than pure equity and are considered more suitable.

3 safer alternatives exist for borrowers sitting on a lump sum:

The data from 2010 to 2025 is clear. SWP is a retirement income tool, not an EMI payment mechanism.

Indian borrowers must separate 2 decisions: where to invest a lump sum and how to repay a home loan. Merging them creates a fragile system that breaks in the 1st bad market year. Prepayment remains the safest option. If investment is the goal, keep the SWP entirely separate from EMI obligations.

Should I use a mutual fund SWP to pay my home loan EMIs instead of prepaying the loan?

No. Historical data shows this strategy can fail if markets fall early. Fixed EMIs should not depend on market-linked returns. If you have a lump sum, prepaying the loan is generally the safer option.

Can I rely on an SWP from a ₹50 lakh mutual fund investment to pay my home loan EMI?

Not always. An SWP may work in some market conditions but can struggle during downturns. It should not be your primary EMI repayment plan, especially for long-term home loans.