By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

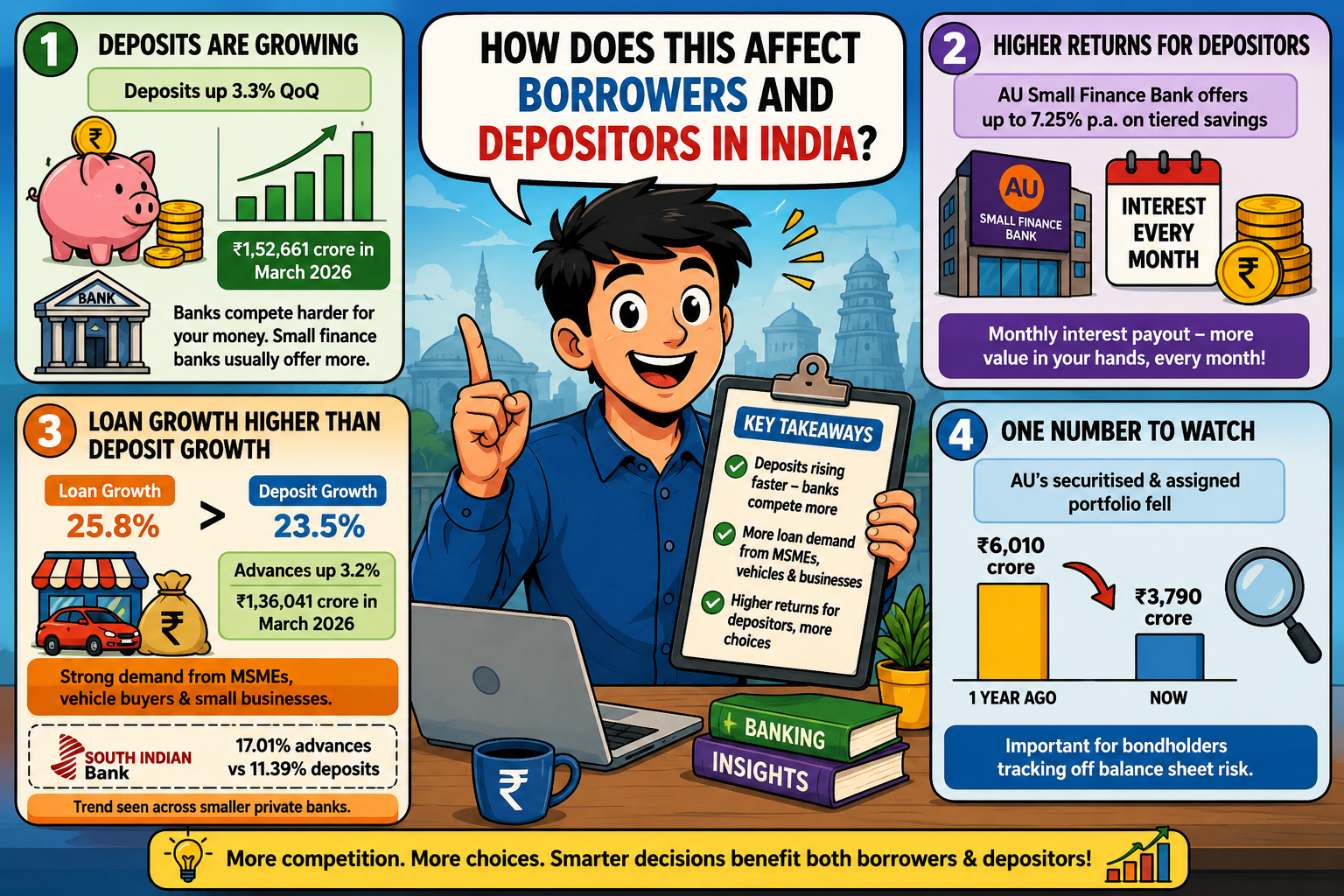

Key Takeaways

June 30, 2026 was a good day for AU Small Finance Bank’s books. Deposits landed at ₹1,57,730 crore, a full 23.5% ahead of where they stood a year earlier at ₹1,27,696 crore. Loans grew even quicker. AU’s gross advances reached ₹1,40,460 crore this quarter, and last year at the same time that number was ₹1,11,614 crore, a 25.8% climb. Bring the securitised book, assigned portfolio and IBPCs into the mix, and total lending settles at ₹1,44,250 crore, well above the ₹1,17,624 crore mark from June 2025.

There’s more going on here than just growth, though. The RBI has already cleared AU in principle to become a universal bank, a rare status for any small finance bank to reach. On the ground, AU ran close to 2,790 touchpoints across 21 states and 4 Union Territories as of March 31, 2026, with a customer base crossing 1.2 crore. None of the June quarter figures are locked in yet. They’re still sitting with the audit committee, board and statutory auditors, so the official Q1 FY27 results won't be out until later this month.

Deposits rose 3.3% quarter on quarter, up from ₹1,52,661 crore in March 2026. That kind of growth doesn’t come easy right now. Every bank in India is fighting harder for the same retail rupee. Small finance banks usually win that fight by paying more.

LoansJagat's rate data confirms this. AU Small Finance Bank offers up to 7.25% per annum on tiered savings balances, and pays out interest every month instead of the usual quarterly cycle most banks follow. That monthly payout is a small thing on paper, but it’s often the reason a depositor picks AU over a larger private bank offering a lower, quarterly rate.

Loan growth outran deposit growth again this quarter, 25.8% against 23.5%. That gap points to steady demand from MSMEs, vehicle buyers and small businesses. Advances rose 3.2% from ₹1,36,041 crore in March 2026. AU isn’t the only lender seeing this. South Indian Bank posted 17.01% advances growth against just 11.39% deposit growth in the same quarter, so the pattern runs across smaller private banks this year, not just AU.

One number worth flagging is AU’s securitised and assigned portfolio fell to ₹3,790 crore, down from ₹6,010 crore a year ago. Bondholders tracking off balance sheet exposure should keep an eye on that drop.

Founder, MD and CEO Sanjay Agarwal has talked up the bank’s growth before. On crossing ₹1 lakh crore in both loans and deposits in FY25, he called it proof of the bank’s resilience, pointing to its expanding footprint and its role as a financial partner across India. The scale of that growth is easy to miss until you see the starting point.

The balance sheet of AU started with approximately ₹5,000 crore in April 2017 when the company converted itself from a NBFC to a bank. It increased to reach over ₹1.9 lakh crore in March 2026. The merger of AU with the Fincare Small Finance Bank in 2024 which was an all-stock merger worth around $530 million contributed to it significantly.

For depositors, the takeaway is simple. Don’t assume one bank has the best rate just because it's the biggest name. AU's CASA ratio slipped from 29.2% a year ago to 28.8% now, which means it's leaning a bit more on term deposits to fund itself. Shop around before locking in a fixed deposit anywhere.

For small businesses hunting for a loan, AU’s ₹1,40,460 crore advances book says the bank still wants to lend, even mid transition to universal bank status. Analysts covering the sector, quoted in the same Business Standard piece, warn that banks growing loans faster than deposits for too long eventually have to raise deposit rates or slow down lending, or their loan to deposit ratio gets uncomfortable.

Go back one more year and the pace looks even steadier than it seems at first glance. In June 2025, AU had reported deposits of ₹1,27,700 crore, up 31.3% from ₹97,290 crore a year before that, with advances of ₹1,11,620 crore, up 23.1%. Some of that older growth came from base effects tied to the Fincare merger. Now that the base is much bigger, past ₹1.5 lakh crore in deposits, holding onto 23.5% growth is harder to pull off, and AU has done it anyway.

AU Small Finance Bank starts FY27 with ₹1,44,250 crore in loans and ₹1,57,730 crore in deposits, both ahead of last year. The June 30 numbers are still provisional, pending sign off from auditors and the board. Between its 2,790 touchpoints, a new corporate office at BKC in Mumbai, and the RBI’s in-principle nod to go universal, AU has plenty riding on the next few quarters. Whether it can keep loans outgrowing deposits without squeezing its margins is the real question for anyone watching this bank closely.

Does AU Small Finance Bank’s Q1 FY27 update show any relief on bad loans?

The business update as at 30th June, 2026 only gives out data about deposits and advances but does not provide any information about asset quality such as gross NPA and net NPA. While deposits stood at ₹1,57,730 crore and loans at ₹1,44,250 crore, no information is provided here about any bad loans. The information about asset quality will be available once we have the complete quarterly results for Q1 FY27.

Should recent AU Small Finance Bank news change my credit card decision?

Not for this update specifically. The June 2026 numbers cover deposits and loans, not credit card operations. AU’s deposits grew 23.5% and advances grew 25.8% year on year, both signs of a bank scaling up, not shrinking. If anything, steady growth like this is a mild reassurance for existing cardholders. There’s no reason drawn from this particular update to switch cards or worry about the bank’s stability.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article