Bank Of Baroda’s Big FY27 Credit Bet: ₹50,000 Crore Corporate Loan Pipeline In Focus

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Bank of Baroda wants faster corporate lending in FY27, backed by a ₹50,000 crore pipeline and stronger Q4 FY26 asset quality.

Key Takeaways

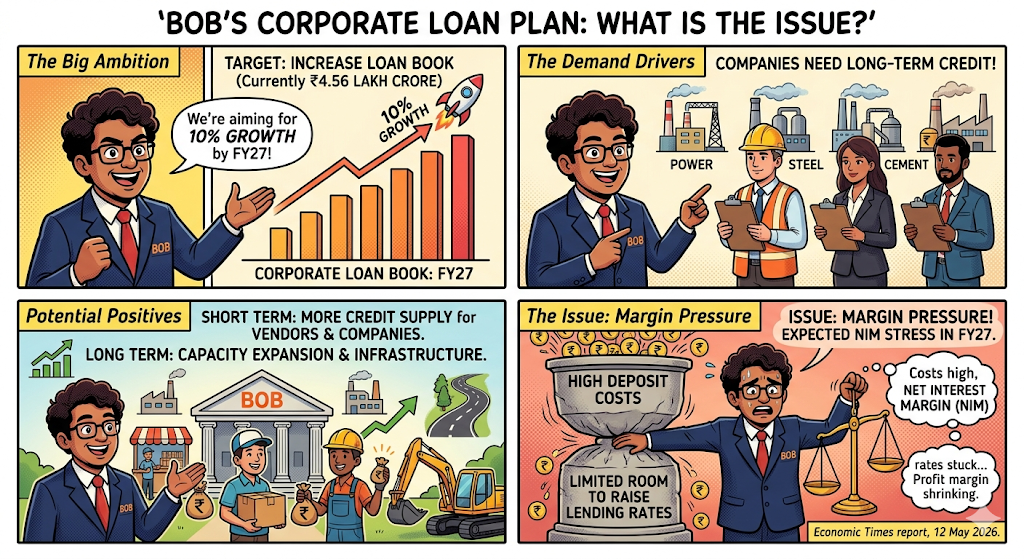

- Bank of Baroda is targeting 10% growth in its ₹4.56 lakh crore corporate loan book in FY27, with ₹50,000 crore in pipeline loans.

- The previous update was its Q4 FY26 result, where profit rose 11.25% YoY to ₹5,615.68 crore and asset quality improved.

Bank Of Baroda Loan Growth Plan: What Is The Issue?

Bank of Baroda is aiming to expand its corporate loan book by 10% in FY27. The public sector lender’s corporate loan book is currently around ₹4.56 lakh crore, and the fresh push comes at a time when companies in power, steel and cement are looking for long-term credit. Business Standard reported this on 11 May 2026, citing PTI.

In the short term, this can improve credit supply to large companies and their vendors. In the long term, it can support capacity expansion and infrastructure-linked activity. The negative side is margin pressure, as deposit costs remain high and banks have limited room to raise lending rates. The Economic Times reported on 12 May 2026 that BoB expects pressure on net interest margin in FY27.

The Big Numbers Behind BoB’s FY27 Corporate Push

The bank has a corporate loan pipeline of ₹50,000 crore. Around 50% of this has already been sanctioned but not disbursed, while the rest is under discussion. BoB MD and CEO Debadatta Chand also said nearly two-thirds of the proposals are term loans, while the remaining are working capital loans.

These figures show that the bank is not only chasing short-term working capital loans. A higher share of term loans points to corporate borrowers planning project expansion, fresh assets or capacity addition.

How This Credit Push Can Affect Indian Borrowers And Businesses?

For common people, corporate loan growth may not directly cut EMIs or change savings rates. But it can help indirectly. When companies receive long-term funds, they can build factories, expand power projects, buy equipment and pay suppliers faster.

This can support jobs, local contractors, logistics players and small vendors linked to large companies. The risk is that if corporate loans are priced too cheaply, bank margins may weaken. BoB has guided for 12-14% overall advances growth and 10-12% deposit growth in FY27, while aiming to keep net interest margin in the 2.75-2.95% band, according to The Economic Times on 12 May 2026.

What Experts And Stakeholders Are Saying?

Debadatta Chand said BoB has enough base to support growth but may also look beyond deposits for funding. He said the bank is seeing proposals from renewable power, steel and cement, with term loans forming a bigger share of the pipeline.

The likely solution for BoB is selective growth, stronger fee income and better pricing. The bank also plans to step up treasury and wealth business to offset weaker margins, as reported by The Economic Times on 12 May 2026.

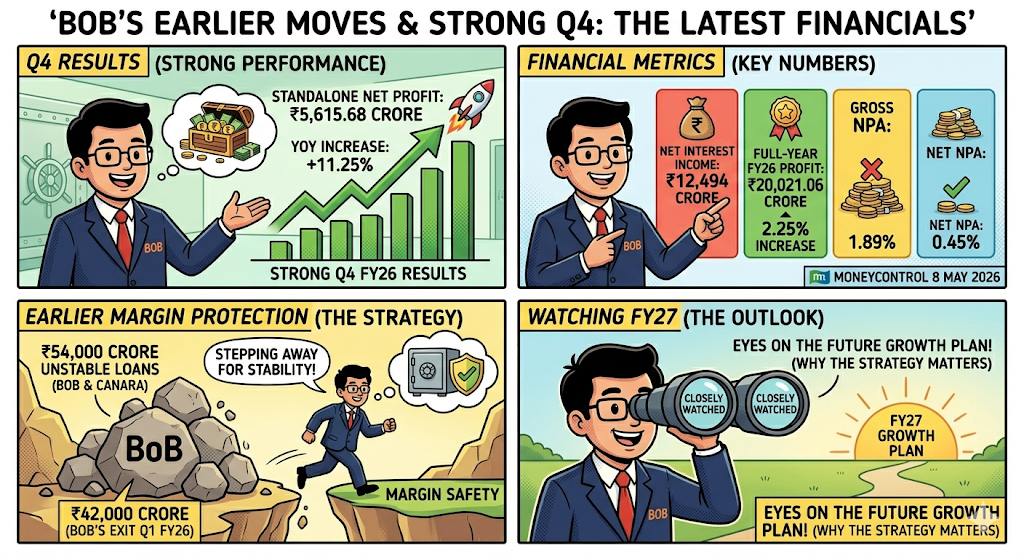

Q4 Profit, NPAs And Margin Safety

Before this FY27 loan target, BoB had reported strong Q4 FY26 numbers. Moneycontrol reported on 8 May 2026 that standalone net profit rose 11.25% YoY to ₹5,615.68 crore, while full-year FY26 standalone profit increased 2.25% to ₹20,021.06 crore.

There was also an earlier margin-protection move. LoansJagat reported that BoB and Canara Bank together stepped away from ₹54,000 crore of loans, with BoB exiting about ₹42,000 crore in Q1 FY26, citing margin safety. This shows why the FY27 corporate growth plan will be watched closely.

Conclusion

Bank of Baroda’s FY27 plan is a strong corporate credit push built on a ₹50,000 crore pipeline and better asset quality. The challenge is simple: grow faster, but keep margins and bad loans under control.

FAQs

Can a first-time business owner in India get a loan without strong business history?

Yes, a first-time business owner can get a business loan, but approval depends on documents, credit score, business plan, income proof and collateral. Banks usually prefer existing businesses because they can check sales, GST returns and repayment capacity.

For a new business, the borrower should prepare a proper project report, expected revenue, investment details and use of funds. A good personal credit score also helps. New entrepreneurs can also check government-backed schemes, NBFC loans or small-ticket business loans before applying for a large loan. Avoid borrowing without knowing EMI pressure and cash flow.

What happens to a bank’s money when a company fails to repay its loan?

When a corporate firm defaults on a loan, the bank first tries to recover the money from the company itself. It may use collateral, sell pledged assets, restructure the loan, or take legal action under recovery laws. If recovery is not enough, the bank must absorb the loss by making provisions from its profits.

In serious cases, the loan becomes a non-performing asset, or NPA. Depositors do not directly pay for the default, but large defaults can reduce a bank’s profit, weaken lending capacity and affect shareholders. That is why banks carefully check corporate borrowers before giving large loans.

Related Finance News | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article