Can a ₹15 Lakh Salary Get You a ₹1 Crore Home Loan in 2026?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- ₹15 lakh a year is ₹1.25 lakh a month before any deductions. Banks use FOIR norms to cap your eligible EMI at 50% of gross income, which comes to ₹62,500. A ₹1 crore loan at 8.5% over 30 years costs ₹76,900 a month. The numbers do not work.

- This income-to-loan mismatch is not new. Lenders tightened FOIR ceilings for mid-income borrowers through 2025. Those same caps, 40 to 55% for anyone earning below ₹2 lakh per month, are still in force in 2026.

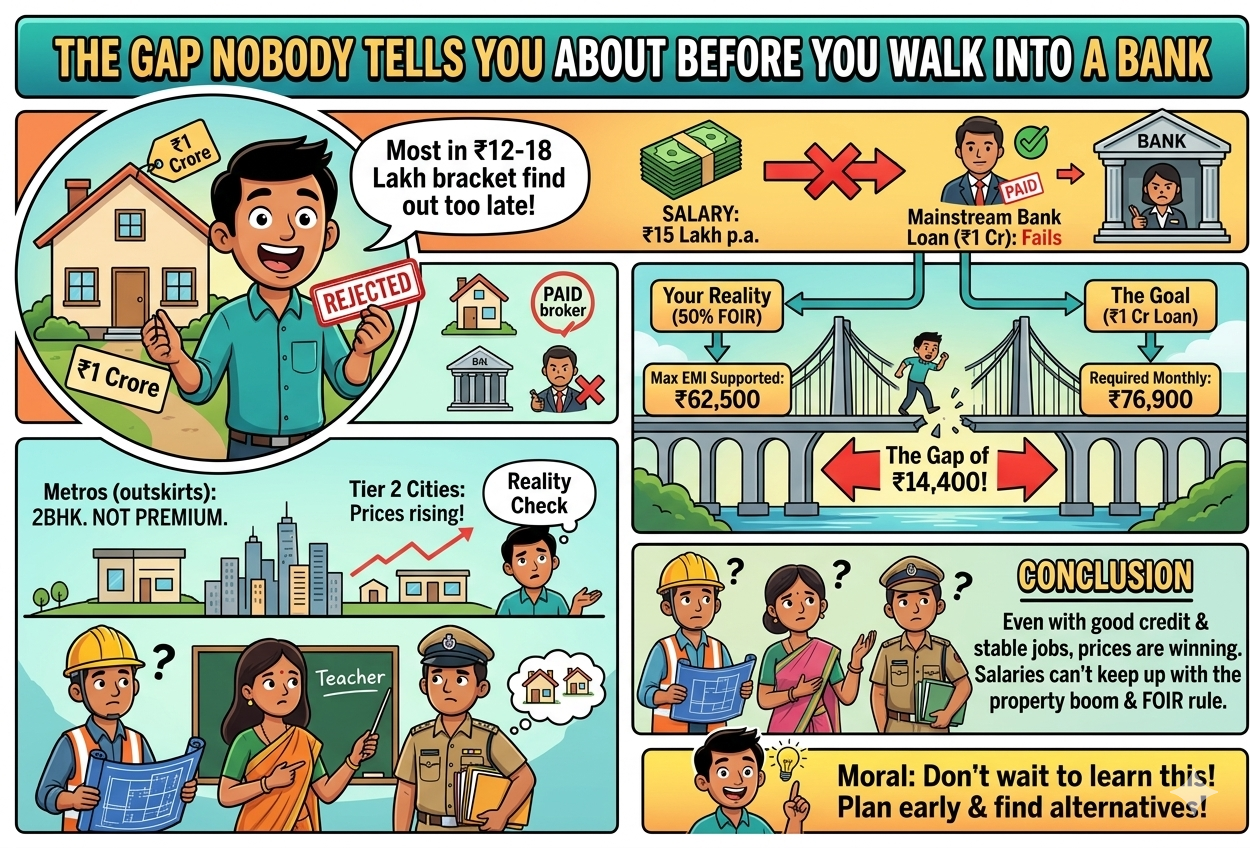

The Gap Nobody Tells You About Before You Walk Into A Bank

Most people in the ₹12 to 18 lakh salary bracket find out too late. The property is shortlisted. The broker has been paid. The bank rejects or, at the very least, accepts a figure which is 40% less than what was anticipated.

Salary of ₹15 lakh in June 2026 will not help in qualifying for a home loan of ₹1 crore by any mainstream Indian bank in one go. Under the ceiling of 50% FOIR, the maximum EMI that could be supported by this salary is ₹62,500. This loan requires ₹76,900 monthly. There is a gap of ₹14,400, which cannot be overlooked by any bank.

The difficult question then becomes what this ₹1 crore can buy in 2026. In major metropolitan cities like Delhi, Mumbai, or Bengaluru, this will purchase a 2BHK apartment on the outskirts and definitely not anything premium. Second-tier cities do provide more, but their prices have been increasing too. Thus, this is not an issue faced by people who dream beyond their capacity.

Engineers working for a salary, teachers in schools, and mid-level government officers with a good credit score and stable income will face the same issue here. Their incomes are simply lagging behind the price of properties, and the FOIR framework has never had a solution to this problem.

How does this play out for middle-income buyers across India?

The tenure argument is the first thing most buyers try. If a 20-year tenure costs too much, why not go to 25 or 30 years? The table below shows why this doesn't fully solve the problem:

The EMI of ₹76,900 clears the ₹62,500 eligibility limit by a significant margin, even at the maximum 30-year tenure. The answer is not stretching the tenure.

There is, however, a real way through. Adding a co-applicant can increase home loan eligibility by 50-80%, according to MoneyKarma’s 2026 home loan eligibility guide. It is enough to make a ₹1 crore loan viable for two earning members applying together.

On top of that, RBI’s LTV rules require a minimum 25% down payment on loans above ₹75 lakh. This means a buyer needs to bring ₹25 lakh to the table before stamp duty or registration costs, a factor that reduces the required loan amount and improves eligibility simultaneously.

What Experts Say? What the Numbers Actually Support?

Most lenders in India sanction a home loan of 55 to 65 times the net monthly salary, provided the FOIR stays within acceptable limits, according to Easy Home Finance. For a ₹15 lakh salary with a take-home of around ₹90,000 after tax and PF deductions, that puts realistic eligibility between ₹49.5 lakh and ₹58.5 lakh.

Financial planners put the ceiling slightly higher (₹55 to ₹65 lakh) for borrowers with a CIBIL score above 750 and no existing EMI obligations. Either way, the number sits well under ₹1 crore.

LoansJagat’s data confirms that lenders consistently ensure total monthly EMIs do not exceed 50% of net take-home salary. Mid-income borrowers on their platform regularly underestimate the FOIR gap when targeting loans above ₹75 lakh.

Three steps to improve outcomes are to add a co-applicant to combine incomes, clear existing personal or vehicle loan EMIs before applying, and extend tenure to 30 years to bring the EMI to its lowest point. A borrower who plans 12 to 18 months ahead can realistically work through all three before approaching a lender.

Conclusion

A ₹15 lakh salary, on a solo application, qualifies for roughly ₹55 to ₹65 lakh in 2026, not ₹1 crore. The math is the math, and no lender will waive the FOIR ceiling. Borrowers in this bracket should either target properties within that loan range or build a joint application with an earning co-applicant. The door to a ₹1 crore loan isn’t closed, but it does require a plan, not just a pay slip.

FAQs

How much home loan can I get on a ₹1 crore property?

Banks fund a maximum of 75% of properties above ₹75 lakh, per RBI’s LTV rules. That means ₹75 lakh is the highest possible loan. The remaining ₹25 lakh must come from you as a down payment. Final approval still depends on whether your income clears the FOIR threshold.

Is a ₹1 crore home loan manageable on a ₹1.45 lakh take-home salary?

Barely. Your FOIR limit allows a maximum EMI of ₹72,500, but the loan needs ₹76,900 per month. Most banks will sanction ₹90 to ₹95 lakh at best. Without a co-applicant or larger down payment, the financial margin is too thin to be comfortable.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article