Credit Card Late Fee Shock? 3-Day Buffer May Save Indian Cardholders

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

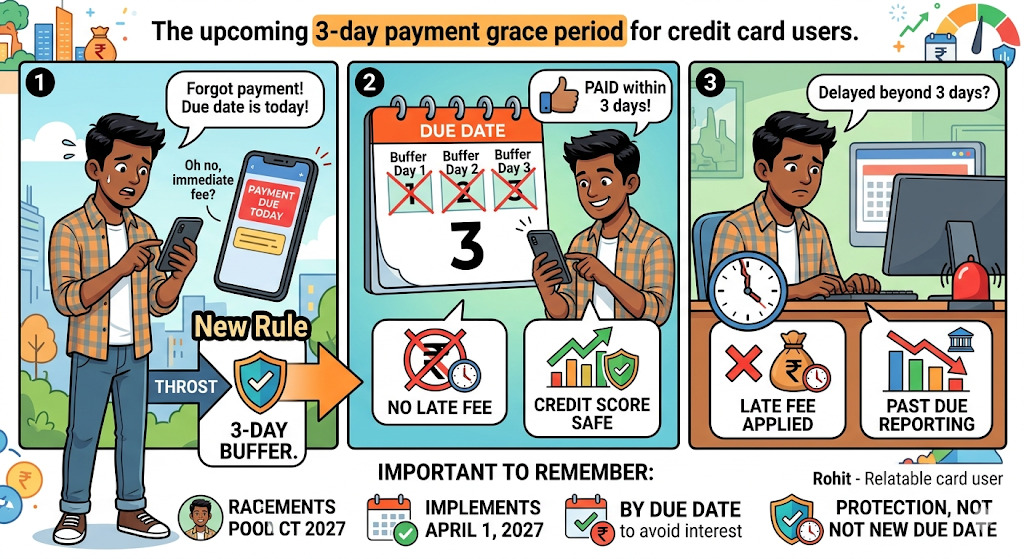

A missed credit card due date by 1 or 2 days may soon stop hurting users through instant penalties or credit bureau tags.

Key Takeaways

- Card issuers can charge late fees or report “past due” status only if payment remains unpaid for more than 3 days.

- The earlier update was the wider credit reporting shift, where lenders moved towards faster borrower data reporting from April 1, 2026.

What Has Changed For Credit Card Users?

Credit card users will get a 3-day payment buffer before late fees or “past due” reporting can begin. NDTV Profit reported on April 29, 2026 that the revised rules will apply from April 1, 2027, giving banks and card issuers time to update systems and customer disclosures.

Read More - Unpaid Credit Card Debt

In the short term, this helps users who miss payments due to salary delay, bank holiday, failed auto-debit or app glitches. In the long term, it can reduce unnecessary credit score damage. The risk remains that the original due date does not shift, so delays beyond 3 days can still invite charges.

This change is not a new due date. It is a short protection window. Cardholders still need to pay by the statement date to avoid interest and future billing stress.

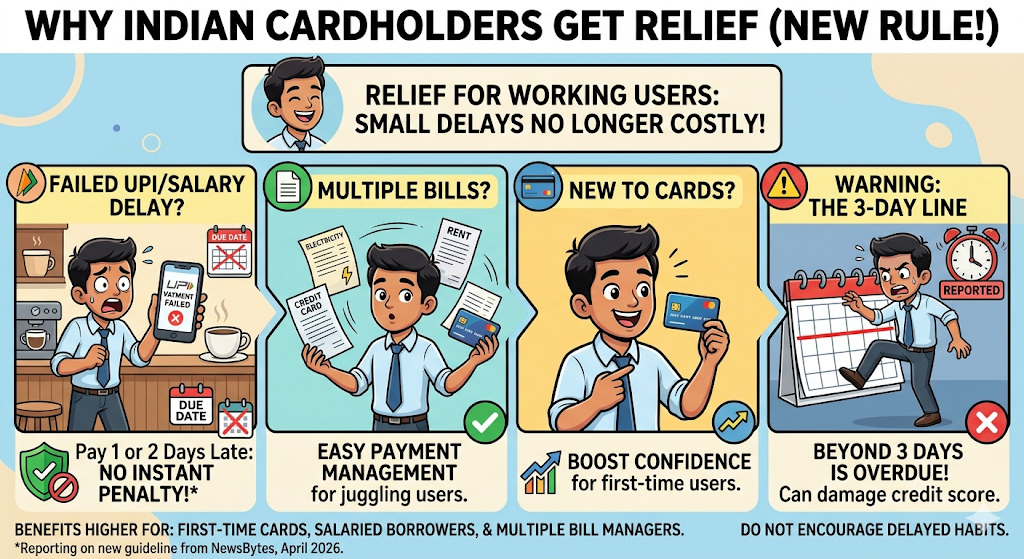

Why Indian Cardholders Will Feel The Impact

For India’s working users, the biggest relief is on small delays. A person who pays 1 or 2 days late due to a failed UPI transaction or salary credit issue may not face an instant penalty. NewsBytes reported on April 29, 2026 that the new guideline links both reporting and penal action to a delay of more than 3 days.

The positive impact is higher for first-time card users, salaried borrowers and people managing multiple bills. Still, the rule should not encourage delayed payment habits. Once the 3-day line is crossed, the card account can be treated as overdue and reported to credit information companies.

Earlier Updates Behind This Move

The 3-day rule comes at a time when India’s credit data system is getting faster. The Economic Times reported that regulated lenders were asked to report borrower account information to credit information companies every week from April 1, 2026, instead of slower reporting cycles.

Also Read - Repayment Strategy That Works Smart Debt Plan

That earlier change means both good and bad repayment behaviour can show up faster in credit records. So, while the 3-day buffer reduces sudden penalties, quicker reporting also means customers have less room to ignore unpaid dues.

This makes payment timing more important. A quick correction within 3 days can protect the user, but a longer delay may travel faster into the credit record.

What Experts Say And What Users Should Do?

Personal finance experts quoted across news reports see this as a consumer-friendly change because it separates small technical delays from genuine defaults. Upstox reported on April 28, 2026 that late charges must be linked to the unpaid amount after the due date, not the total bill.

The practical solution is simple. Users should keep auto-debit active, pay 2 days before the due date, track failed payments and avoid paying only the minimum due. The buffer should be used only for genuine delays, not as a monthly habit.

Conclusion

The 3-day rule gives credit card users breathing space, not an extended due date.

For a clean credit record, paying before the bill date remains the safer move.

FAQs

Can A 10-Minute Credit Card Payment Delay Affect CIBIL Score?

A credit card payment delayed by just 10 minutes is unlikely to affect the CIBIL score if the amount is paid within the 3-day grace period. In this Reddit case, the user paid an SBI credit card bill at 12:10 AM, just after the due date, and was worried about late fees and credit reporting.

As users discussed, banks generally should not report such short delays to credit bureaus within the grace window. However, customers should still check the statement for late fee or interest charges and contact customer care for reversal if needed.

What If A Credit Card Bill Remains Unpaid For 3 Years?

If a credit card bill is not paid for 3 years, the outstanding amount can grow sharply due to interest, late payment fees and other charges. The bank may mark the account as default, report it to credit bureaus and the user’s CIBIL score can fall heavily.

Recovery calls, legal notices and settlement offers may also follow. Even if the bank writes off the account, the borrower’s credit report can still show negative history for years. The best step is to contact the bank, ask for a repayment plan or settlement and get written confirmation after payment.

Related Finance News | |||

RBI Expands Agri Startup Financing Through Cooperative Banks | |||

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article