By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

The Employees’ Provident Fund Organisation notified the EPF Scheme, 2026 on 29 June 2026, replacing the EPF Scheme of 1952. The new framework runs under the Code on Social Security, 2020. It applies to every salaried employee registered with EPFO across India’s organised sector.

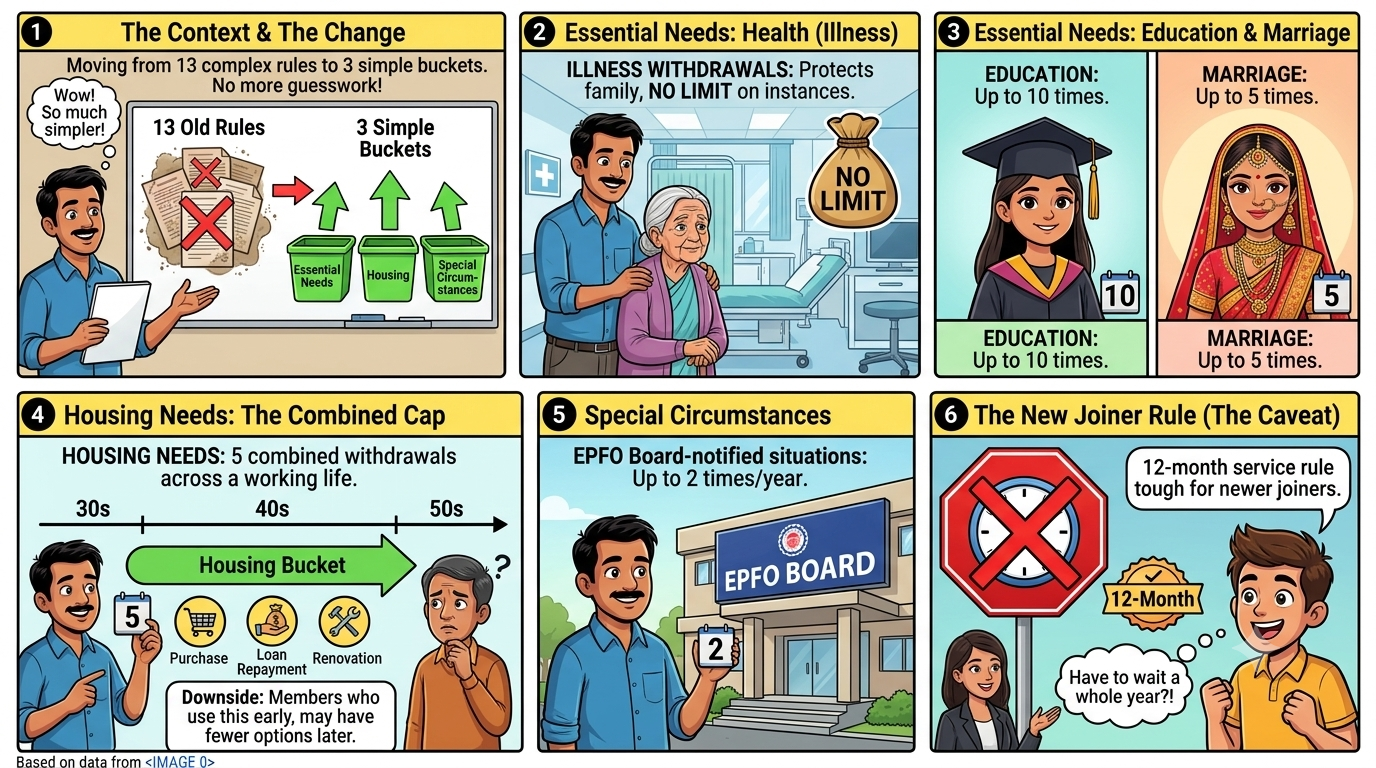

The biggest shift merges 13 separate withdrawal provisions into 3 categories: essential needs, housing needs and special circumstances. Each category now carries a fixed cap on how many times a member can withdraw during their entire EPF membership, not per job.

This matters because provident fund withdrawals often decide whether a family can pay a hospital bill on time. In the short term, members get simpler rules and faster digital claims, settled within 3 working days for eligible cases.

In the long run, the new restrictions regarding housing and special situations may make life hard for employees who have to pay out frequently for the same reasons over their ten to fifteen-year service period.

For over 7 crore EPFO subscribers, moving from 13 rules to 3 buckets removes a lot of guesswork. Earlier, an employee needing money for house repairs had to check separate clauses for renovation, alteration, and reconstruction.

Now, all 4 housing needs sit under one category with a combined cap of 5 withdrawals across a working life. The downside is that members who use this cap early, say for a plot purchase and a home loan repayment in their 30s, may find fewer options left for renovation in their 50s.

There is a genuine upside too. Illness withdrawals under essential needs carry no cap at all, protecting families during medical emergencies. Education withdrawals rose to 10 instances and marriage withdrawals to 5, both counted over the full EPF membership period. An HR industry comment on the reform called the expanded list “welcome, especially for housing and education,” while flagging the 12-month service rule as tough for newer joiners, as reported by Newkerala.

Members who complete 12 months of EPF membership can withdraw up to 75% of their eligible balance, including both employee and employer contributions plus interest. A member with a ₹1 lakh eligible balance must still keep ₹25,000 untouched, as confirmed in EPFO’s notification. This 25% minimum balance rule applies after every partial withdrawal, not just the first one. The EPF interest rate stays unchanged at 8.25% for FY 2025-26, so the reform only touches process, not returns.

This is also where LoansJagat’s data on salary contributions becomes useful context. According to LoansJagat’s PF deduction guide, an employee earning ₹15,000 basic salary contributes 12%, or ₹1,800 a month, while the employer matches this, split into 8.33% for pension and 3.67% for EPF. Over a 20-year career, this steady 24% combined contribution builds the very corpus that the new withdrawal caps now govern more tightly.

As reported by NewKerala, EPFO made no effort to conceal that the new change is “a step taken as part of a larger effort by EPFO to make service delivery easier and provide greater convenience in accessing Provident Fund savings to over seven crore members.” The said initiative was approved at the 238th Central Board of Trustees meeting, which was held on 13 October 2025 under the chairmanship of Dr Mansukh Mandaviya, Union Labour Minister. It is worth noting that the upgrading process brought up the auto-settlement limit from ₹1 lakh to ₹5 lakh.

Financial planners tracking the rollout suggest the solution to reduced flexibility lies in planning withdrawals around real-life stages, not using them reactively. Since housing and special circumstances now carry strict caps of 5 and 2 per year respectively, advisors recommend mapping likely future needs, such as a home loan versus a renovation, before filing any claim. LoansJagat’s data on salary-linked PF contributions shows how predictable this corpus is, which makes early planning around the 3 new categories realistic rather than reactive.

Beyond category limits, EPFO has tightened its claims timeline. Eligible online withdrawal claims are now targeted for settlement within 3 working days, down from the earlier 15 to 20-day window.

Offline claims made through employers also take almost 20 working days. Digital verification through Aadhaar has done away with most of the paperwork involved. EPFO 3.0 will have UPI and ATM card withdrawal facilities, which will be introduced phase-wise till 2026 mid.

The EPF Scheme 2026 simplifies the complex scheme of 13 rules to the simplified 3-category system with defined limits on the essential, housing and special needs withdrawals. For the 7 crore subscribers of EPF 2026, this implies an easier claim process from 29 June 2026 onwards. The downside is the reduced scope of making multiple withdrawals for the same purpose, mostly housing, so the employees must plan their withdrawals according to significant life events.

What will be the new formula for calculating the employee PF under EPF Scheme 2026?

There is no new formula for calculating the PF. The Payroll team can continue to deduct 12% of the Basic Salary + Dearness Allowance from the employees, and the company matching contribution will be 12% divided into 8.33% for EPS and 3.67% for EPF. All that HR teams will have to do is make sure the advance withdrawal forms have been updated as per the 3 new categories.

What are the exact withdrawal limits for essential, housing and special needs under EPF Scheme 2026?

Essential needs cover illness with no limit, education up to 10 times, and marriage up to 5 times over a full EPF membership. Housing needs, covering purchase, construction, loan repayment and renovation, allow 5 withdrawals total. Special circumstances, notified by EPFO's Central Board, permit 2 withdrawals per financial year.