FCNR(B) Rates Increased by 300 bps Due to RBI Taking Over Hedging Costs

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

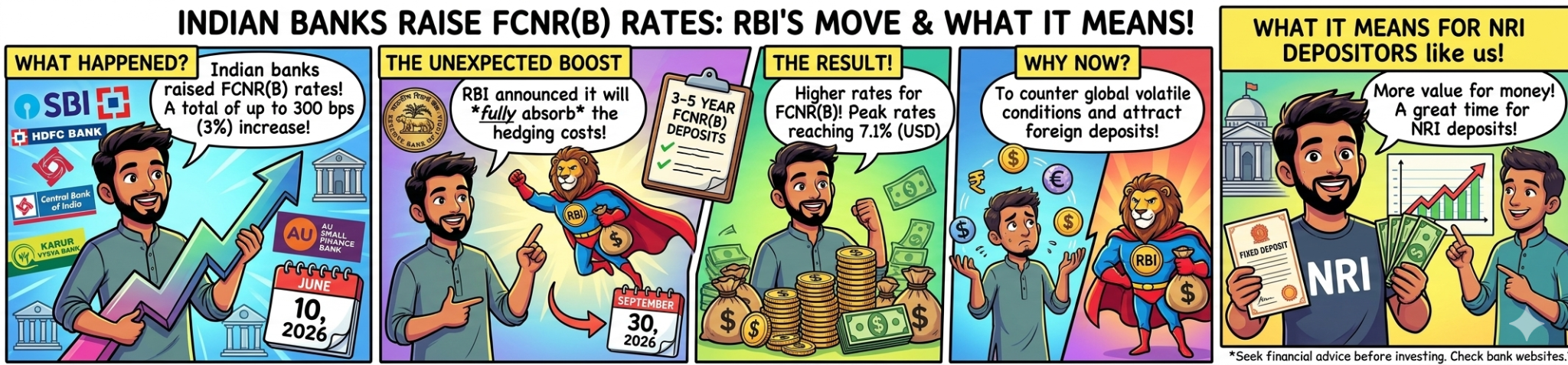

- On June 10, 2026, SBI, HDFC Bank, Central Bank of India, Karur Vysya Bank, and AU Small Finance Bank increased their FCNR(B) deposit rates by up to 300 bps. Deposit interest rates have reached 7.1% in case of US dollars.

- RBI stated that it would take over all the hedging cost of fresh deposits made with an FCNR(B) tenure of 3 to 5 years until September 30, 2026, on June 5, 2026.

Changes Made on FCNR(B) Rates on June 10, 2026

On June 10, 2026, SBI increased FCNR(B) deposit rates by 295 bps. HDFC Bank also increased FCNR(B) deposit rates by 260 bps. Karur Vysya Bank raised peak rates by over 300 bps, and it reaches 7% for 3 to 5 year USD deposits. AU Small Finance Bank offers 7.1% on 3 to 4 year deposits.

SBI launched a special product called “SBI Advantage FCNR(B) Deposit,” which offers 6% for deposits above $1 million for a 5-year term. SBI offers 5.25% for deposits below $1 million in the 3 to 4 year bucket. Rates were increased by 255 bps for the 4 to 5 year bucket. These are USD-denominated deposit rates for NRIs, OCIs, and Persons of Indian Origin (POIs).

How will these Higher Rates Affect NRIs and India’s Forex Inflows?

Before this scheme, SBI offered just 3.05% and HDFC Bank 3.4% on 5-year FCNR(B) deposits. With hedging costs previously around 2.5% per year, banks could not offer competitive rates without bearing a heavy cost. The new RBI facility removes that barrier entirely.

SBI Research now expects inflows of $40-45 billion via the FCNR(B) route. MUFG Bank estimates $20 billion as a base case. The current outstanding FCNR(B) deposit balance as of March 2026 stands at $33.8 billion, up from $32.8 billion a year ago. A flood of NRI dollars could strengthen the rupee and ease India’s pressure on forex reserves.

What are Experts Saying? What should NRI Depositors do?

P D Singh, CEO for India and South Asia at Standard Chartered Bank, said the scheme could materially improve foreign currency inflows into India.

SBI Research stated that banks can now offer FCNR(B) pricing in the range of 5.5% and above. FCNR(B) deposits could easily attract inflows exceeding the $34 billion mobilised during the 2013 scheme.

According to a Senior Financial Analyst at Loans Jagat, NRIs with idle foreign currency savings should compare rates across at least 3-4 banks before locking in. “The window is open only until September 30, 2026. Acting early matters,” she said.

Conclusion

The RBI’s June 5, 2026, decision to absorb hedging costs has triggered a sharp rate war among Indian banks. FCNR(B) deposit flows in FY26 were only $946 million, versus $7 billion in FY25. This scheme is a direct attempt to reverse that gap. For NRIs holding US dollars, UK pounds sterling, Euros, Australian dollars, Canadian dollars, or Japanese yen, FCNR(B) deposit rates have jumped sharply. Check your bank’s revised rates before September 30, 2026, which is the last date to mobilise deposits under this scheme.

FAQs

Why did RBI grant permission to banks to raise interest rates for FCNR(B) and NRE deposits from June 2026 onwards?

The rupee was under stress owing to lower foreign portfolio investments. The RBI decided to abolish the interest rate ceiling and absorb the cost of hedging in order to bring in NRIs’ dollars.

Are FCNR(B) deposits actually worth opening now, given the new RBI scheme?

Yes, if you hold foreign currency savings. Banks like AU Small Finance Bank are offering 7.1% on USD deposits. The hedging cost is fully covered by RBI until September 30, 2026. Returns are tax-free in India. The window is short, so act soon.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article