By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

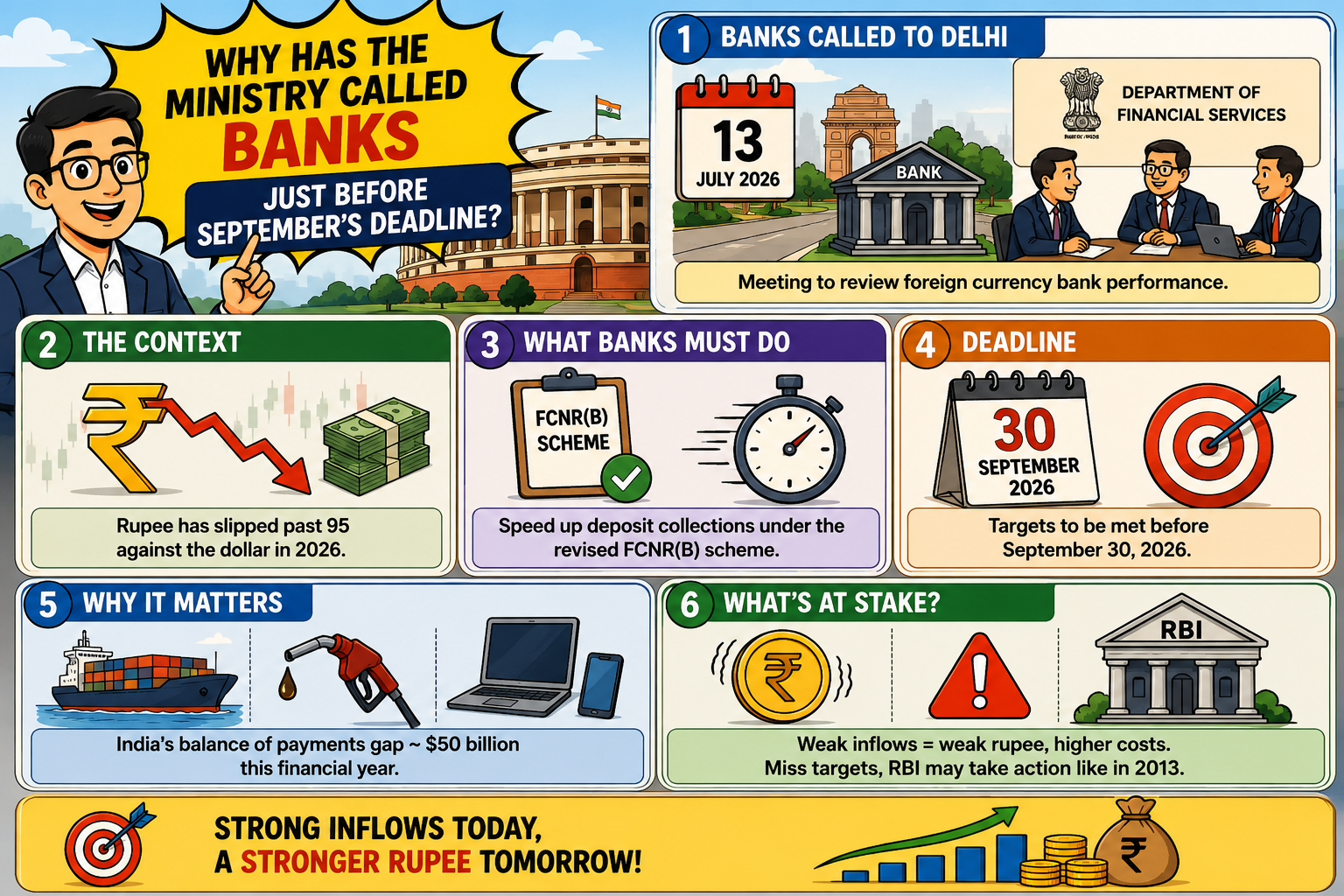

The Finance Ministry has called banks for a meeting on 13 July 2026 to check foreign currency inflows and push lenders to collect more.

Bank chiefs from public and private lenders have been called to New Delhi on 13 July 2026 by the Department of Financial Services. The meeting will track how much foreign currency banks have pulled in so far this year. This comes as the Indian currency has already fallen below 95 against the US dollar in 2026. The government officials need quick deposits from the new Foreign Currency Non-Resident Bank, popularly referred to as FCNR(B), before the deadline of 30 September 2026.

This is not a trivial matter, since there is about $50 billion in the current fiscal year’s balance of payments gap in India, as indicated by the June 2026 research paper from MUFG Research. Delayed flow results in an unstable currency, which makes oil and electronics more expensive. Quicker mobilisation, on the other hand, could calm the currency within weeks. Banks missing targets by September might force the RBI’s hand on fresh steps, echoing tools last used back in 2013.

Fuel and electronics get pricier fast when the rupee weakens. A one-rupee slide against the dollar can nudge retail petrol prices within days, QuantEco Research economists have pointed out. That kind of inflation often delays rate cuts from the Reserve Bank of India. Anyone tracking home loan or personal loan EMIs through 2026 should watch this space closely.

There’s an upside too, and it belongs mostly to NRIs. Roughly 9 million Indians live and work across Gulf countries, and they now earn 6 to 7 percent on FCNR(B) deposits, up from near 3 percent before June 2026. RBI is also covering the entire hedging cost on these deposits until 30 September 2026, so banks pass zero extra charge to depositors.

FCNR(B) Scheme: The Numbers Behind the 13 July Meeting

Just $3 to $4 billion has come in against a self-set target of $40 to $50 billion, and that shortfall is exactly why the ministry called this meeting. Banks have roughly 11 weeks left to close the gap through wider NRI outreach, especially across Gulf markets.

Economic Affairs Secretary Anuradha Thakur addressed the rupee directly in a PTI interview earlier this year. She said the government starts watching closely once the currency crosses 90 against the dollar. Thakur added that regulators are tracking the situation jointly, though a weaker rupee does help export competitiveness at times.

QuantEco Research’s Vivek Kumar flagged a separate worry around reserve quality. He noted India's usable foreign currency assets stood at $449 billion in March 2026, with a rising gold share eating into that cushion. Persistent Middle East tensions, he said, could squeeze import cover further in the coming months.

MUFG Research’s 8 June 2026 estimate puts total inflows near $40 billion for the year across all RBI measures combined. Their FCNR(B)-specific estimate lands around $20 billion, well short of what bankers are chasing. The gap owes partly to US short-term rates sitting near 4 percent now, against near-zero levels back in 2013.

Most analysts point to speed and outreach as the practical fix. Banks are being pushed to run sharper NRI awareness drives before September. A second lever floated in Reuters reporting from May 2026 involves dropping the 5 percent withholding tax on foreign bond investors, whose 2026 purchases fell to $1.1 billion from $6.5 billion in 2025.

Yes, in September 2013, under then-RBI Governor Raghuram Rajan. The scheme aimed for $10 billion and ended up pulling close to $30 billion, according to RBI records cited by Business Standard. That earlier success is the reason the ministry is pressing lenders again in 2026, only this time within a tighter nine-month window. Bankers involved in the 2013 push say direct, one-on-one contact with NRI clients made the real difference then.

RBI's 2026 version goes a step further too. Rate ceilings on FCNR(B) deposits above three years have been scrapped entirely, and banks get CRR and SLR relief on top. The 13 July meeting will likely ask lenders how well they've used this room so far.

Nothing new gets announced on 13 July 2026. This is a checkpoint, one where the ministry pushes banks to turn policy support into actual dollars before 30 September 2026. With just $3 to $4 billion collected against a $40 to $50 billion goal, the gap is still wide open. Borrowers, NRIs, and rupee watchers all have reason to follow what comes out of this meeting over the next 11 weeks.

Can currency swaps really shore up a country’s forex reserves during rupee pressure like this?

Currency swaps buy time rather than fix root problems. RBI's current facility lets banks raise FCNR(B) deposits without bearing hedging costs, which genuinely speeds up dollar inflows in the short term, as seen with the $26 billion raised through a similar swap-linked push in 2013. But swaps add contingent liabilities that resurface when deposits mature, typically in three to five years. They work best paired with structural fixes like narrowing the trade deficit, not as a standalone solution.

Which providers should NRIs use to move foreign currency into India right now?

Stick to RBI-authorised channels only. Any bank offering FCNR(B) deposits under the June 2026 scheme, including major public and private lenders, qualifies as a safe route right now. For smaller remittances, RBI-registered money transfer operators and the Reserve Bank’s own Liberalised Remittance Scheme framework apply. Avoid informal transfer agents entirely, since they fall outside RBI oversight and offer no protection if funds go missing. Checking a provider's RBI authorisation status before transferring money takes only a few minutes.

6% to 7%, up from ~3%