By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

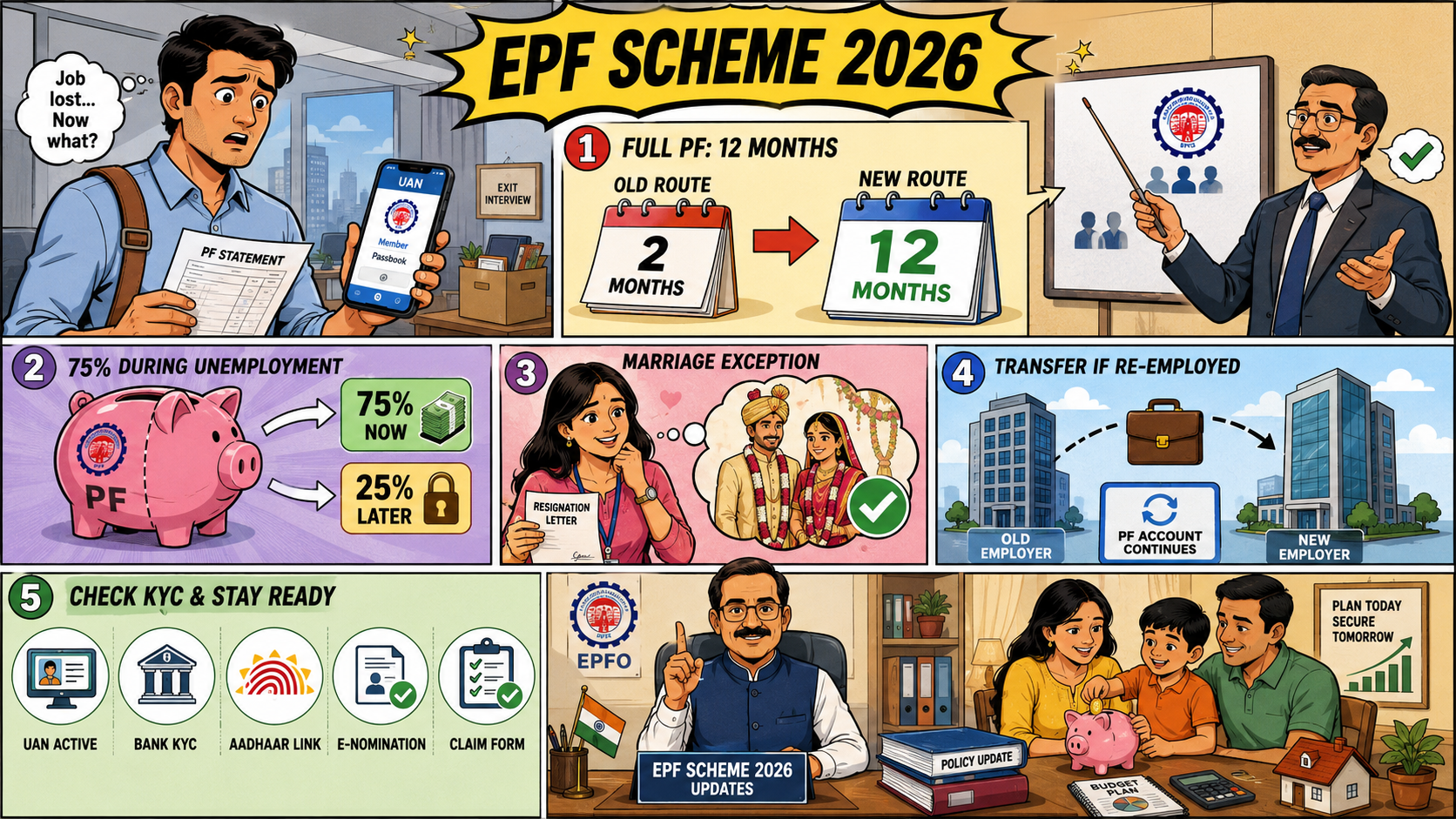

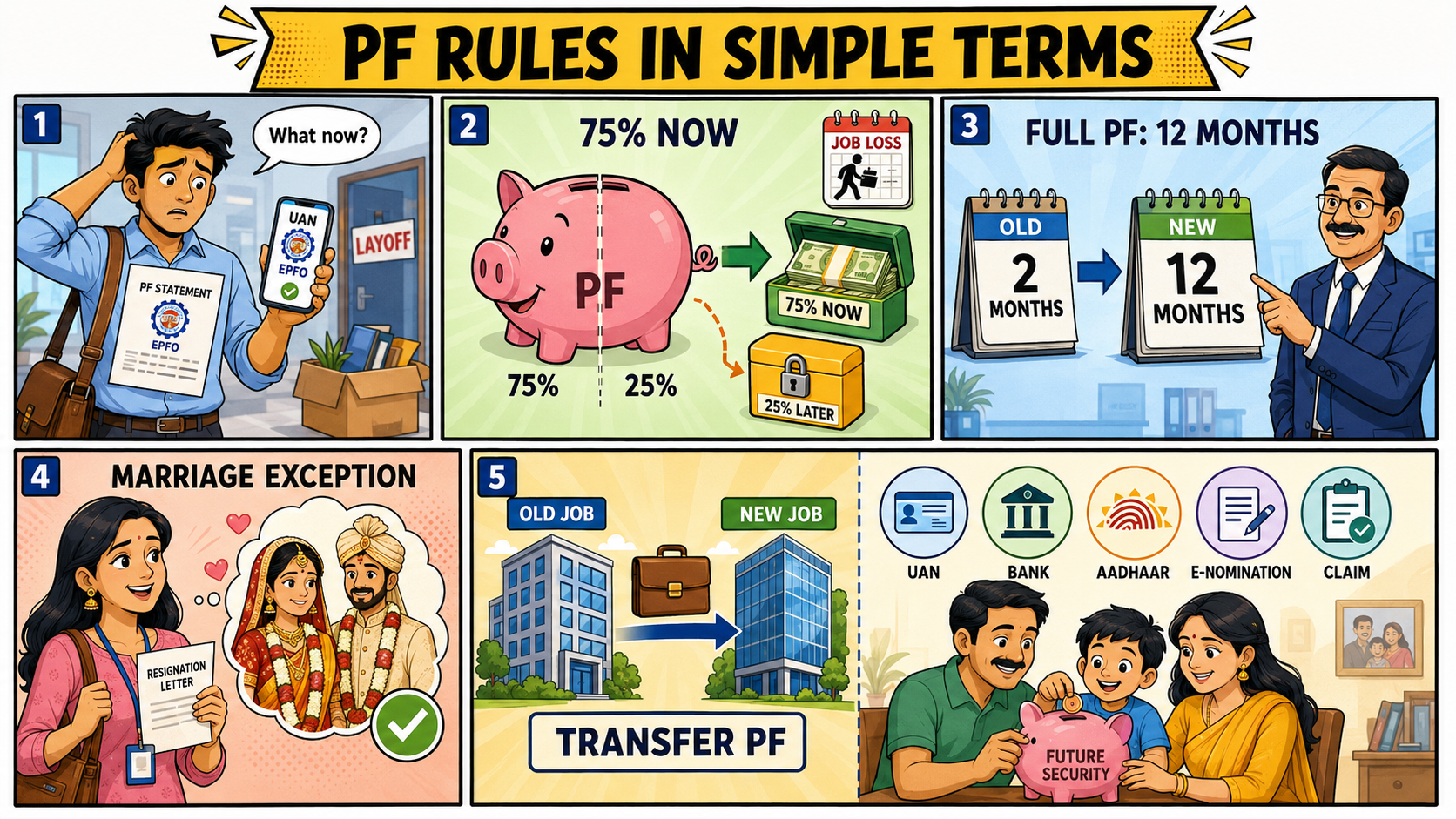

EPF members who lose employment now face a 12-month wait for full PF withdrawal, while 75% access remains available during unemployment.

Key Highlights

The EPF scheme 2026 has changed how full PF withdrawals are made after a loss of employment. The Gazette of India states that members will now have to wait 12 months after leaving continuous employment in a code-covered establishment before making an application for a full PF withdrawal. The previous system of a 2-month waiting period has been scrapped for run-of-the-mill job loss cases.

This would negatively impact those PF members who rely on their PF as a safety net in case of layoffs or resigning. The 12-month waiting period places a financial burden on members who would need to cover their rent, bills, or even the costs of looking for a new job. Though the rule aims to specifically address the discouragement of constantly withdrawing retirement savings whenever an individual changes their job.

The new PF withdrawal rule changes the conditions for employees leaving employment to withdraw the full balance of the provident fund. The EPF Scheme 2026 now allows full withdrawal of the provident fund only after completion of the 12-month period of non-employment in a covered establishment. This now applies to the majority of ordinary job exit cases.

There are some exceptions to this. Registered female members resigning to get married do not have to fulfill the waiting period. The EPF Scheme also provides for full withdrawal in cases such as retirement, permanent disability, voluntary migration, retrenchment, and voluntary retirement. However, for a majority of employees in the private sector, the 12-month waiting period will apply.

For India’s salaried workers, the first impact will come during a sudden job loss. A person in Delhi NCR, Pune, Bengaluru or Hyderabad may have PF savings from years of service but cannot take the full amount quickly after exit. That can create stress when severance is small or the next job takes longer than expected.

The positive side is that members do not lose access completely. The EPFO reform note dated October 15, 2025, said 75% of the PF balance, including employee share, employer share and interest, can be withdrawn during unemployment. The remaining 25% stays in the account so that the member does not restart retirement savings from zero after every job break.

Before filing a PF claim, members should check what has changed. The legal text may look heavy, but the worker-facing result is simpler.

This table should not be read as a replacement for claim rules on the EPFO portal. A worker should check UAN, exit date, Aadhaar-bank linkage, e-nomination and employer contribution history before filing a claim. One wrong entry can delay money when the person needs it most.

Compliance experts quoted in the reference report have read the 2026 scheme as a major shift for HR, payroll and employee exit processes. Employers now need to keep exit dates, contribution records and employee details clean because PF withdrawal timelines depend on those records. A wrong exit date can turn into a direct problem for the worker.

The safer route for members is simple. If the person is moving to a new job, a PF transfer is usually better than a full withdrawal. If the person is unemployed and needs funds, a partial withdrawal can help. For basic member guidance, the LoansJagat PF withdrawal guide explains how much PF can be withdrawn and what members should check before applying.

The biggest change is not only the 12-month wait. It is the way families will plan emergency cash. A worker who earlier expected full PF money after 2 months may now need a separate 3-month to 6-month emergency fund outside EPFO. That can reduce dependence on credit cards and personal loans after job loss.

For borrowers, the rule can change behaviour. A salaried person with a home loan or personal loan may need to speak to the lender early if income stops. Waiting until the EMI default begins is risky. The better option is to use 75% PF access only for essential costs, keep loan repayment records clean and avoid spending the PF amount on non-urgent expenses.

Before the EPF Scheme 2026, workers were used to the 2-month withdrawal idea after unemployment. Many resigned employees waited for the exit date to reflect on the UAN portal and then applied for final PF settlement. That made PF a common fallback fund after a job change or job loss.

The policy direction changed before the final 2026 notification. EPFO’s October 2025 reform note had already said that frequent withdrawals were reducing final PF balances. The government then notified the EPF Scheme 2026 through the Gazette on June 29, 2026, giving the new withdrawal structure legal backing.

The government’s position is that provident fund money should serve long-term social security. EPFO has said repeated withdrawals leave members with lower balances at final settlement. That is why the 25% retention rule has been pushed as a retirement-saving protection.

Workers may look at it from a monthly budget angle. A person who has lost a job may not want to wait for retirement logic when rent is due on the 5th. Employers also carry a larger responsibility now. HR teams must update exit dates correctly, guide employees on partial withdrawal and transfer, and avoid delays in records.

EPF Scheme 2026 has made full PF withdrawal after job loss stricter. The worker still gets 75% access during unemployment, but full settlement now needs 12 months in ordinary job-exit cases.

For salaried Indians, the PF account can no longer be treated like quick backup cash after every job break. Members should keep UAN records updated, check KYC before filing, and use PF withdrawal only after planning the next few months carefully.

What changed in full PF withdrawal after job loss?

Full PF withdrawal now needs 12 months of non-employment under the EPF Scheme 2026.

Can a member withdraw any PF amount during unemployment?

Yes. A member can withdraw 75% of the eligible PF balance during unemployment.

What happens to the remaining 25% PF balance?

What remains of the 25% stays in the PF account until the 12-month condition is fulfilled.

Does the 12-month rule apply to female members resigning for marriage?

No, the EPF Scheme 2026 will specifically exclude women who resign from jobs due to marriage.

Should a worker withdraw PF after joining a new job?

PF transfer is the general preference whenever a worker joins a new establishment that is also covered.