By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

RBI’s 2026 gold loan rules raise small-ticket LTV to 85%, while forcing tighter valuation, documentation and borrower protection checks before jewellery-backed credit starts in April.

Key Highlights

Gold loan borrowers in India will see a new lending process from April 1, 2026, when the RBI's gold and silver collateral rules fully apply to banks, cooperative banks, NBFCs and housing finance companies. The biggest borrower-facing change is the 85% LTV cap for consumption gold loans up to ₹2.5 lakh. The Reserve Bank of India issued the directions on June 6, 2025.

This affects first-time borrowers in the short term because many may get a higher sanctioned amount for jewellery. Later, it can reduce disputes at closure since lenders must document purity, weight and deductions. The negative side is plain. A borrower who treats the higher LTV as extra spending room can lose repayment breathing space. Gold loans remain secured loans in India, and family jewellery can still go to auction if repayment fails.

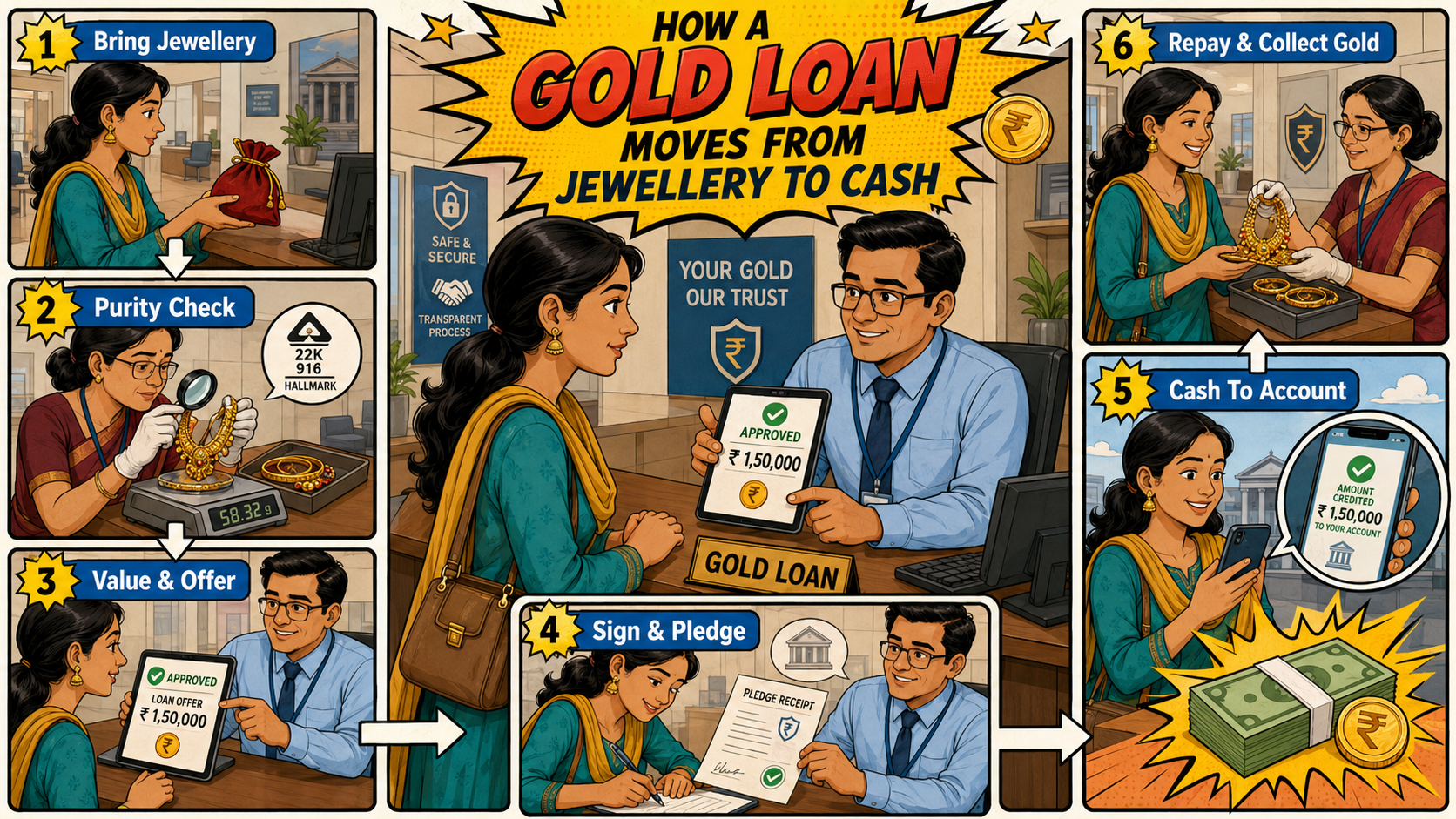

A first-time borrower usually walks into a branch with one figure in mind, the money needed that day. The new rules push the lender to look beyond that. The pledged article has to be checked for ownership, net gold content and valuation. If the jewellery has stones, lacquer, enamel or heavy design work, those parts do not increase the loan value.

The shop bill also does not decide the loan. A necklace bought for ₹2 lakh may carry making charges and design costs, but the lender will focus on the gold content. This difference can disappoint borrowers at the counter. It is better to know this before signing.

The borrower should first ask whether the lender is regulated and whether all charges appear in the Key Fact Statement. Interest rate is only one part. Processing fees, valuation fees, renewal fees, penal charges and auction costs can change the actual cost of the loan.

A second check is documentation. Borrowers should collect the pledge receipt and the assaying certificate or e-certificate. That record should mention purity, gross weight, net weight, deductions and value at sanction. A photograph of the pledged jewellery, where given, can help later if there is a dispute about the article returned after repayment.

The table below gives the main borrower checks, along with official source points that should be verified before handing over jewellery.

Most gold loan trouble starts with three weak points: an unclear repayment date, a misunderstood jewellery valuation and missing documents after sanction.

Step 1 starts at home: The borrower should list the purpose, amount needed and likely repayment date. A medical bill due in 10 days is different from a business gap with uncertain cash flow.

Step 2 happens at the branch: The lender checks the jewellery, purity and net gold weight. The borrower should remain present during the process and ask how stones, lac or other non-gold parts are deducted.

Step 3 is the sanction stage: The lender offers a loan amount, interest rate, tenure and repayment option. The borrower should not sign only because the amount looks attractive.

Step 4 is the repayment period: A borrower choosing bullet repayment has to keep the final date visible. Paying everything at the end may look easy on day 1, but it can hurt if income is delayed.

Step 5 is closure: After full repayment, the borrower should collect the pledged jewellery and compare it with the original receipt or certificate before leaving the branch.

For many Indian homes, gold is not an investment product on a spreadsheet. It is wedding jewellery, inherited bangles or a chain bought after years of saving. When a sudden cash need arises, that jewellery becomes the fastest way to raise money without selling land, breaking a business cycle, or asking relatives.

The 85% LTV cap can help smaller borrowers who need urgent credit up to ₹2.5 lakh. A borrower may receive a better sanctioned amount from the same eligible gold, compared with the older 75% ceiling. This can support school fees, crop spending, shop stock or hospital payments. The catch is repayment. Higher access also means a larger outstanding amount if the borrower stretches the loan without a cash plan.

Banking experts usually read the new framework as a borrower protection move with a warning attached. The protection comes through better valuation records, a written trail and standardised checks. The warning comes from household behaviour. Gold loans are easy to take and easy to roll over, so some borrowers stop treating them as short-term credit.

A safer plan is boring, but it works. Borrow below the eligibility, not up to the last rupee. Match tenure with a known income date. Keep repayment money separate when a salary, crop receipt or customer payment arrives. If the branch staff pushes renewal without explaining the total cost, the borrower should ask for the full payable amount in writing before agreeing.

A higher loan limit can tempt borrowers to take more than they need. That is where trouble usually begins. According to LoansJagat, documentation can improve the loan process, but repayment behaviour still decides whether the pledge stays safe. A borrower who takes ₹2 lakh for a ₹1.2 lakh need may feel comfortable on the sanction day. The pressure arrives when interest, renewal charges or a delayed income cycle enters the picture.

The safer route is to treat a gold loan as a short cash bridge. Before signing, the borrower should name the exact repayment source, salary credit, shop collection, crop sale, insurance payout or family transfer. If that source is not visible, the loan amount needs a cut. Strong paperwork protects the jewellery record, but only timely repayment protects the jewellery itself.

The last updates were when the RBI published Final Directions on Gold and Silver Collateral on June 6, 2025, after the RBI Policy Discussions on Small Borrowers and Lender Practices. Regulated entities were given until April 1, 2026, for compliance and lenders could make changes in their internal practices, staff, training, valuation formats, and documents for the prospective borrowers.

One of the related consumer updates was on hallmarking. The Press Information Bureau, in its March 4, 2023, release, said that hallmarked gold jewelry would not be allowed to be sold after March 31, 2023, if it did not have a 6-digit HUID. This rule does not substitute the lender’s valuation, it is just one additional way for a prospective borrower to authenticate the identity of the gold jewelry before approaching a lender.

The 2026 gold loan rules have improved access for small borrowers but have increased the need to read the branch carefully. First-time borrowers should check HUID, the cost of the loan, valuation papers, and the repayment date before offering family gold.

What is the 85% LTV rule for gold loans?

It allows eligible consumption gold loans up to ₹2.5 lakh to get funding up to 85% of accepted gold value.

Does hallmarking guarantee a higher gold loan?

No. Hallmarking helps verification, but the lender still checks purity, net weight and valuation before sanction.

Can a borrower lose jewelry after missing payments?

Yes. If dues remain unpaid, the lender can start recovery and auction steps as per loan terms.

Taking a gold loan for 6 months, what is the biggest risk if repayment gets delayed?

The biggest risk is losing pledged jewellery through auction after default notices. Borrow less than the maximum limit and repay before charges pile up.

Should a first-time borrower take the maximum gold loan amount?

No. Borrowers should take only what they can repay from a known income source within the selected tenure.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article