By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

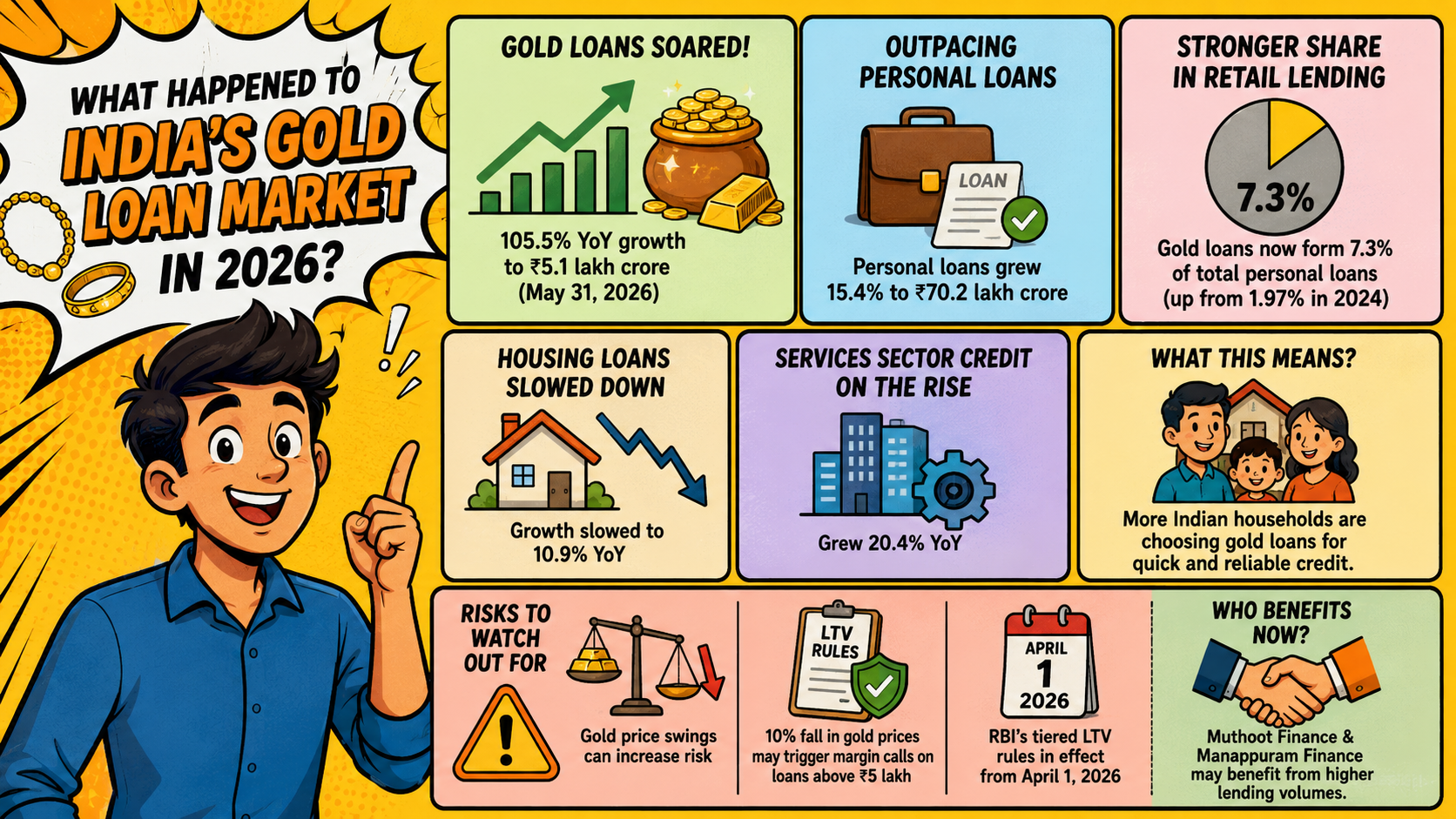

India’s gold loan portfolio surged 105.5% year-on-year to ₹5.1 lakh crore as of May 31, 2026, according to Reserve Bank of India data. This growth far outpaces personal loans, which rose only 15.4% to ₹70.2 lakh crore in the same period.

Housing loan growth slowed to 10.9%, while gold-backed credit expanded its share of retail lending. Gold loans now form 7.3% of India's total personal loan portfolio, up from 1.97% in 2024. The change will affect millions of Indian households who need fast loans secured by collateral in 2026.

This increase is a sign of a structural change in Indian retail lending, and not just a temporary phenomenon, according to experts who have been following Indian lending trends for 2026. In the immediate future, Muthoot Finance and Manappuram Finance may be able to benefit from increased lending volumes.

Over the long term, rapid growth raises concentration risk tied to gold price swings in 2026. Global industry reports place typical gold price corrections at 10% to 20%, a range that can trigger margin calls under such LTV caps.

Gold loans now offer faster cash access than personal loans in 2026 for millions of Indian households. About 85% of borrowers avail loans up to ₹2.5 lakh, as per RBI data cited in April 2026 reports.

Small-ticket borrowers benefit most from the RBI’s revised loan-to-value structure, effective April 1, 2026. Loans under ₹2.5 lakh now qualify for up to 85% LTV, up from a flat 75% cap.

This flexibility helps students, homemakers, and small business owners access funds without income proof, as per 2026 RBI norms. Gold loans below ₹2.5 lakh no longer require mandatory credit appraisal, per RBI's 2026 framework.

This makes gold-backed credit one of India’s most inclusive lending tools in 2026. LoansJagat data shows bank lending against gold reached ₹2.1 lakh crore by March 2025, up 103% from ₹1.03 lakh crore in March 2024.

Analysts caution that part of 2026’s gold loan growth reflects reclassification, not just fresh demand. A report published by finsightsbysquareleague.com in May 2026 noted a major bank reclassified some agricultural loans as gold loans since May 2024.

This reclassification made the gold loan total look inflated overnight, per the May 2026 report. RBI bulletin data still confirms genuine demand growth across housing, vehicle, and gold-backed loans in 2026.

The RBI has implemented a tiered LTV framework from April 1, 2026 to address this risk. Lenders must now return pledged gold within 7 working days of loan closure, as per 2026 rules. Delayed returns attract a ₹5,000 daily penalty, payable directly to the borrower. Experts at thesecretariat.in notes that the RBI is monitoring bank and NBFC exposure closely through 2026

Swaminathan J, RBI Deputy Governor, has commented that gold loans enable formal access to credit if lenders adopt prudent valuation, transparent lending practices, and adequate borrower assessment. It is believed that lenders should be more cautious about maintaining disciplined LTV ratios and risk management than loan growth.

India’s gold loan market crossed ₹5.1 lakh crore by May 31, 2026, which marks 105.5% annual growth. Borrowers gain faster access to funds, but lenders face gold price volatility risk. The RBI’s tiered LTV regime, which became effective from April 1, 2026, seeks to achieve a balance between accessibility and safety. Monitor NBFC margins and asset quality carefully until the end of 2026.

Why are people opting for gold loans in 2026?

Loans taken against gold have risen by 105.5% to ₹5.1 lakh crore up to May 31, 2026, says the RBI. This happened because gold prices went up. Faster approval, no income proof for loans under ₹2.5 lakh, and quick cash needs are also driving this shift.

Should I buy gold during a price dip in 2026?

It depends on your goals and risk appetite, so this isn’t investment advice. RBI’s April 2026 tiered LTV rules cap loans above ₹5 lakh at 75% LTV. Industry reports cite gold price corrections of 10% to 20% as a common trigger for margin calls.

15.4%