By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

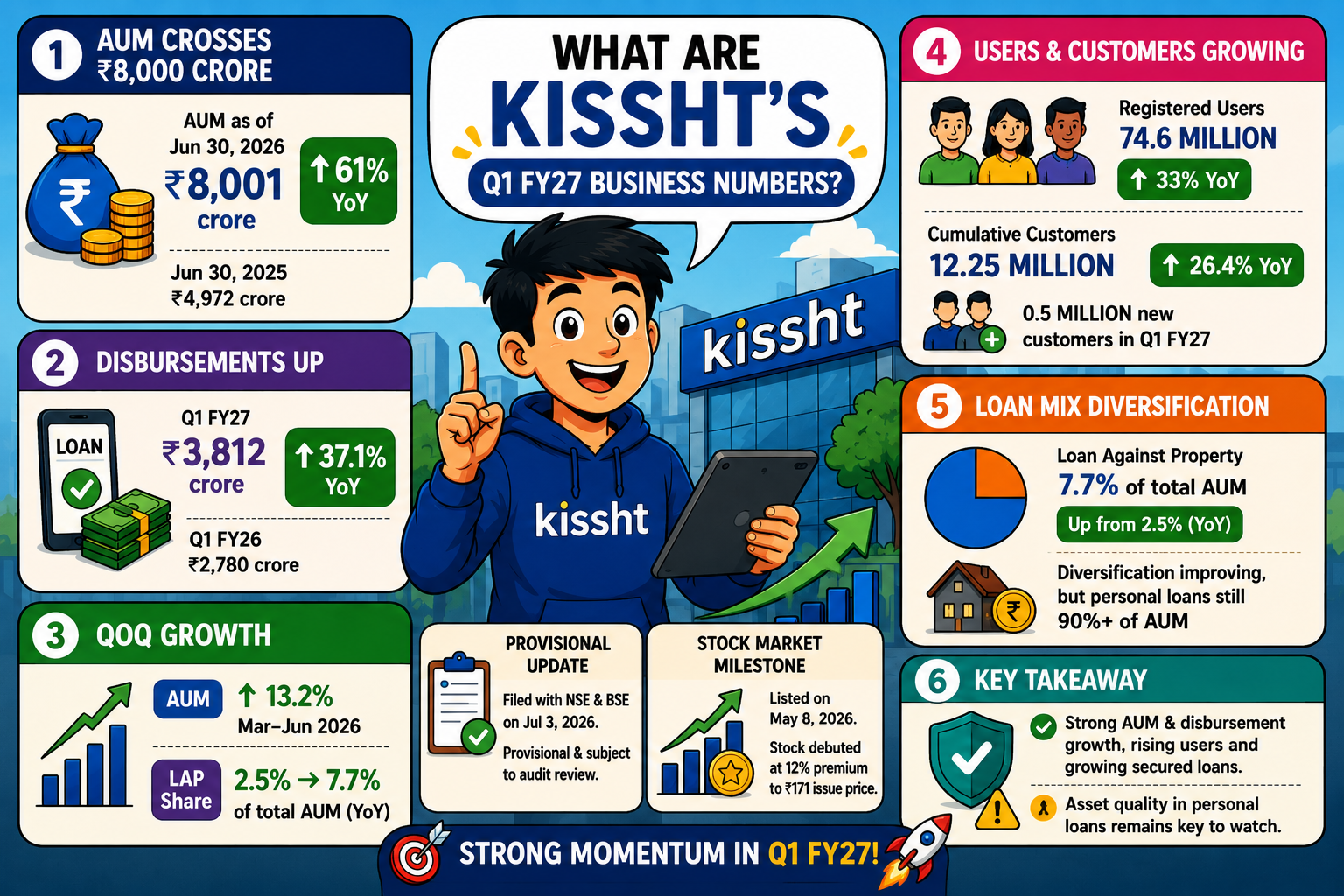

OnEMI Technologies Pvt Ltd is the Mumbai based parent of digital lending brands Kissht and RING. Its assets under management crossed ₹8,000 crore in the first quarter of FY27. AUM stood at ₹8,001 crore as of June 30, 2026, up 61% year on year. A year earlier, on June 30, 2025, AUM was ₹4,972 crore. Loan disbursements rose 37.1% year on year to ₹3,812 crore. In Q1 FY26, disbursements had stood at ₹2,780 crore.

The company’s provisional business update was filed with the NSE and BSE on July 3, 2026. These figures are provisional and await review by statutory auditors, as is standard for such quarterly filings. This growth follows Kissht’s stock market listing on May 8, 2026, when the stock debuted at a 12% premium to its ₹171 issue price.

Quarter on quarter, AUM grew 13.2% between March and June 2026. Registered users rose 33% year on year to 74.6 million by June 30, 2026. Cumulative customers served climbed 26.4% to 12.25 million, with 0.5 million new customers added during the quarter. The company’s Loan Against Property book expanded sharply to 7.7% of total AUM, up from just 2.5% a year earlier.

This diversification builds on a trend flagged in the company’s FY26 results, where LAP share had increased from 1.8% the previous year, with management expecting the scale up to accelerate through FY27. Yet unsecured personal loans still make up over 90% of Kissht’s overall AUM. Regulators have flagged asset quality concerns in this segment since late 2023. This makes the pace of secured lending growth an important metric to track this fiscal year.

Kissht’s scale up means more Indians can access instant, paperless credit for daily needs. Its registered user base grew 33% year on year to 74.6 million, a wide funnel for a company whose co-founders Ranvir Singh and Krishnan Vishwanathan built the platform in 2015 to serve mass market and mass affluent borrowers with small ticket consumer loans. Cumulative customers served rose to 12.25 million by June 30, 2026.

These borrowers tend to be salaried professionals and small merchants based in tier two and tier three cities. Such people are expensive for traditional banks to underwrite. Quick disbursal, which takes place within 24 hours, allows such borrowers to meet emergencies without seeking loans from informal money lenders. This trend aligns well with the digital financial inclusion drive being carried out in India. Since 2015, India’s financial inclusion efforts have accelerated rapidly.

The share of Kissht’s Loan Against Property book in AUM stands at 7.7% as of June 2026, up from 2.5% a year ago. This allows borrowers to take secured loans at much lower interest rates than those prevailing in unsecured personal loans, a service which can help reduce the cost of borrowing for small entrepreneurs who wish to grow.

Disbursements rose 37.1% to ₹3,812 crore in Q1 FY27, up from ₹2,780 crore in the corresponding period last year. The reason for the difference between the rate of disbursements growth and the one of AUM indicates that the lender is able to lend in bulk and manage risks more efficiently than ever before. GNPA was 2.12% in FY26, having improved by 78 basis points quarter-on-quarter and by 77 bps year-on-year.

Ranvir Singh, the Founder and CEO of Kissht, commented after the company’s FY26 results on May 27, 2026, that the fiscal year had demonstrated the excellence of the company’s risk governance framework while facing the post-overleverage concerns in the industry in FY25. He further noted that with capitalization following the successful IPO and improvement in the portfolio, the company would be well-positioned to scale the business responsibly in FY27 and thereafter. This is quite consistent with Q1 FY27 results when AUM grew by 61% y-o-y to ₹8,001 crore and disbursements increased by 37.1%.

Market watchers tracking the stock have also flagged the trading window closure ahead of Q1 FY27 results as a sign that the company's next formal earnings call, expected later this month, will offer a fuller audited picture beyond the provisional figures.

Kissht shares have moved sharply since listing. The stock came out on the stock exchange on May 8, 2026, with its opening price being ₹191 on the BSE, 11.70 percent higher than its issue price of ₹171. The IPO, which sought to raise ₹926 crore through subscription that took place from April 30 to May 5, saw the rally continuing since then in line with its business performance.

Analysts covering NBFC and fintech lenders note that Kissht’s growing Loan Against Property book could act as a cushion if unsecured credit stress resurfaces, since secured assets typically carry lower default risk. This view is reinforced by data outside the company itself.

According to LoansJagat’s review of the RBI’s Financial Stability Report released in June 2024, more than 51.9% of new non-performing assets that year came from unsecured retail loans, including personal loans, credit cards and microfinance. Set against that backdrop, Kissht’s move to grow LAP from 2.5% to 7.7% of AUM in a single year looks less like a side experiment and more like a deliberate hedge for FY27.

Kissht’s Q1 FY27 update shows steady growth less than two months after its stock market debut. AUM of ₹8,001 crore and 37.1% higher disbursements at ₹3,812 crore mark a strong start to the fiscal year. This new approach to the secured credit model using LAP, which is at 7.7% of AUM compared to 2.5% last year, may assist in achieving a balanced approach to growth and risk amid the ongoing unsecured credit concerns among Indian financial institutions. The market will be keen on seeing the audited Q1 results of Kissht for FY27 when the figures become available.

What is the financial status of Kissht in FY27?

Kissht began FY27 on a very good note. AUM went up by 61% to ₹8,001 crore and disbursement saw a rise by 37.1% to ₹3,812 crore in Q1 FY27. Kissht witnessed 74.6 million registered users while 12.25 million were served as customers. The Loan Against Property portfolio was also increased to 7.7% of AUM as against 2.5% in the same period last year.

What are my rights if Kissht serves me a recovery notice?

It is essential that the borrower enjoys proper treatment when the lender goes for recovery of loans. According to RBI guidelines, harassment is not allowed to take place in any way, communication can only be done at a reasonable time and all conditions must be explained clearly to the borrower. You must read the notice, check the outstanding amount and then write back. This is not legal advice. Consult a lawyer.