By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

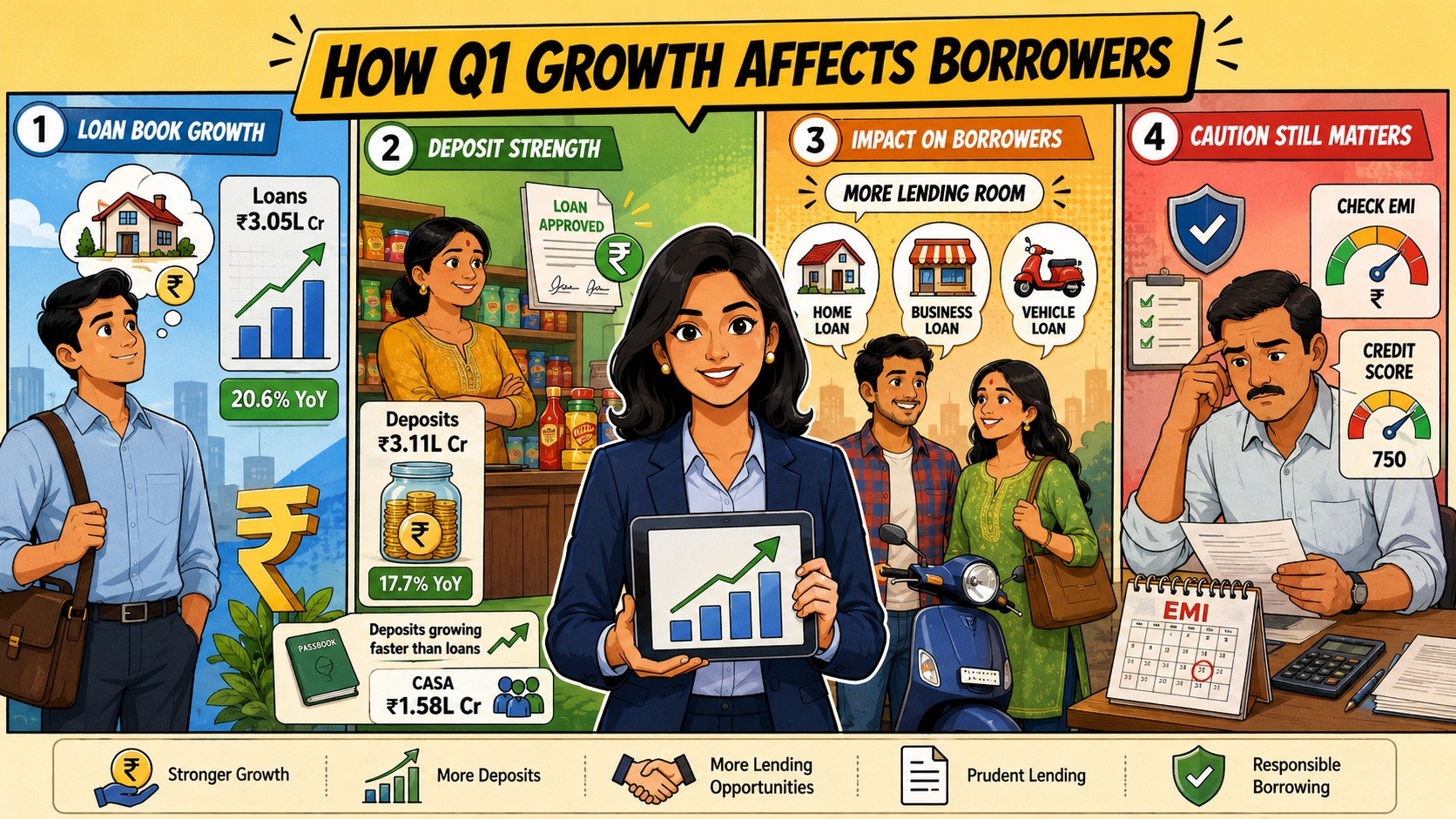

IDFC FIRST Bank’s Q1 FY27 update shows loans above ₹3 lakh crore, while faster deposit growth may support lending and ease funding pressure before results.

Key Highlights

On 03rd July 2026, IDFC FIRST Bank reported a provisional business update for Quarter 1 of FY 27 (01st April to 30th June 2026); total loans increased to ₹305,488 Crores, and total deposits exceeded ₹311,000 crore. Share prices increased by almost 2% as reported by the Economic Times.

For Indian households and businesses, faster lending may improve access to home, vehicle, consumer, and MSME loans. There is a risk, too. Rapid credit expansion can create repayment pressure when checks weaken. The reported loan total includes credit substitutes, not only conventional customer advances. The bank said asset quality continued to improve, though detailed bad-loan and credit-cost numbers remain pending.

Deposits grew 5.9% QoQ, ahead of the 5.2% rise in loans. That 0.7-point gap gives the bank better funding support, but borrowing rates will still depend on funding costs, applicant risk and loan type.

Increases in loans included an annual figure of 52,255 crores and a quarterly figure of 15,210 crores. Deposits increased 46,903 crores YoY and 17,399 crores QoQ. During this period the fastest growth in the bank’s CASA likely decreased reliance on costlier wholesale funds.

In its April 25, 2026 investor presentation, IDFC FIRST Bank said customer inflows had normalised during April and expected deposit growth to recover from Q1 FY27. MD and CEO V Vaidyanathan told The Economic Times on April 27 that annual deposit growth could return towards 20%.

The credit-deposit ratio declined 90 bps QoQ but remained 210 bps above June 2025. LoansJagat’s reading is that the quarterly deposit pickup is positive, yet deposits must keep pace with loans. Its October 23, 2025 analysis had already tracked the bank’s CASA growth and asset-quality movement.

IDFC FIRST Bank’s 20.6% rise in loans may improve access to credit for salaried customers, small businesses and households seeking vehicle or personal loans. A larger deposit base also gives the bank more room to support fresh lending. Still, approval terms will depend on income, credit score, existing debt and repayment history.

LoansJagat views the stronger CASA base and quicker deposit growth as positive signs for funding stability. Its view is that borrowers should not judge a loan only by the advertised rate. Processing fees, insurance costs, foreclosure charges and the final annual cost can change the actual repayment burden.

IDFC FIRST Bank entered FY27 with loans above ₹3 lakh crore and quicker deposit growth. The July 25 results will show whether growth improved earnings without adding fresh loan stress.

When was the Q1 FY27 update released?

IDFC FIRST Bank disclosed the provisional figures on July 3, 2026.

What was the CASA ratio for IDFC FIRST Bank?

The bank’s CASA ratio reached 50.8% on June 30, 2026.

Are IDFC FIRST Bank’s free services genuine or just a gimmick?

The benefits are genuine, but customers should check balance requirements, charges and account terms first.

Is insurance compulsory with an IDFC First Bank loan?

No. Loan insurance is generally optional. Borrowers should verify the sanction letter before agreeing.

Total Deposits

50.8%