In June 2026, Corporate FD Rates Reached 8.95% as NBFCs Were More Competitive than Major Banks

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Corporate fixed deposits are more lucrative than bank fixed deposits. Nevertheless, investors need to consider important factors such as the interest rate, credit risk, tax implications, liquidity needs, withdrawal penalties, and the absence of insurance.

Key Highlights

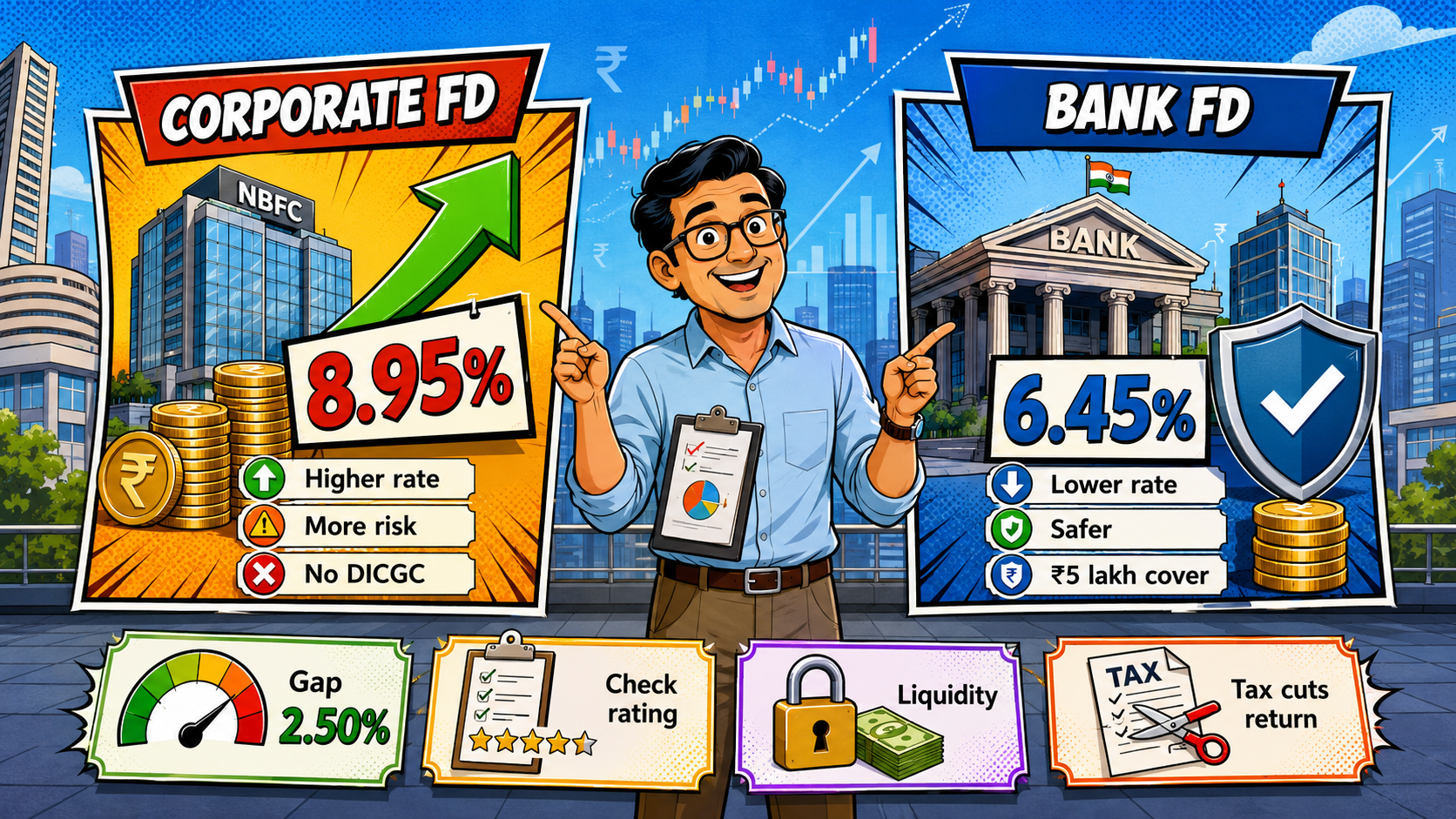

- Muthoot Capital Services offered 8.95% for regular investors over 36 months.

- Senior citizens could earn 9.20% after an additional 0.25%.

- Mahindra Finance offered 7.45%, while Shriram Finance paid 7.25%.

- SBI’s highest listed callable retail FD rate was around 6.45%.

- Corporate FDs do not receive ₹5 lakh DICGC deposit insurance.

Corporate fixed deposit rates reached 8.95% per annum in June 2026, led by Muthoot Capital Services. The rate applied to a 36-month deposit for regular investors, while eligible senior citizens received an additional 0.25%, taking the return to 9.20%.

The comparison, published by Mint on June 22 using rates available on June 17, showed that selected NBFC and housing finance company deposits outpaced major bank FDs. Higher returns, however, bring issuer-level credit risk and no DICGC protection.

Which NBFCs Offered the Highest Corporate FD Rates?

Muthoot Capital’s 8.95% was the highest listed rate, followed by Manipal Housing Finance at 8.25%. Among AAA-rated issuers, Can Fin Homes offered 7.50%, Mahindra Finance paid 7.45%, and Bajaj Finance offered 7.40%.

These are the highest rates reported in the June 17 comparison. Returns can vary by payout frequency, cumulative option and booking date.

Investors should also review the live Muthoot Capital Services rate card because monthly-income and annual schemes may carry different rates.

How Much More Can an Investor Earn at 8.95%?

The illustration assumes a ₹1 lakh cumulative deposit with quarterly compounding. It excludes tax, TDS, premature withdrawal charges and issuer-specific rules.

At 8.95%, the indicative maturity amount is ₹9,252 higher than at 6.45%. That return partly compensates investors for lending directly to a corporate issuer instead of using an insured bank.

How Do Corporate FD Rates Compare With Banks?

The State Bank of India listed 6.45% on its 444-day Amrit Vrishti deposit, while HDFC Bank offered around 6.50% across major retail tenures.

Against 6.45%, Muthoot Capital’s 8.95% creates a 250-basis-point gap. Manipal Housing Finance’s 8.25% creates a 180-basis-point difference, while Mahindra Finance’s 7.45% offers a 100-basis-point advantage.

Why Are Corporate FDs Riskier?

The DICGC states that NBFC deposits are not covered by its insurance system. Eligible deposits with insured banks receive protection of up to ₹5 lakh per depositor per bank, including principal and interest.

The Reserve Bank of India states that only eligible deposit-taking NBFCs with the required investment-grade rating may accept public deposits. Investors should verify authorisation before transferring money.

Credit ratings indicate assessed repayment capacity but do not guarantee repayment. They can change if an issuer’s liquidity, capital position or asset quality weakens.

How Can Depositors Balance Returns and Liquidity?

An 8.95% corporate FD may offer better returns, but locking the full ₹3 lakh for 36 months can restrict access during medical bills, school expenses or income loss. LoansJagat’s emergency fund guide also advises keeping emergency savings readily available.

A better approach is to retain part of the money in an insured bank FD and place only a smaller share in a highly rated corporate FD. Investors should also compare the latest credit rating, withdrawal penalty and post-tax return before applying.

What Should Investors Check Before Booking?

Download the latest rate card, application form and rating letter from the issuer’s website. Confirm the applicable rate on the booking date and select a tenure linked to a defined expense. Emergency funds should not be locked into long corporate deposits.

FAQs

Are corporate FDs insured by DICGC?

No. NBFC deposits do not receive DICGC bank deposit insurance.

Is an AAA-rated corporate FD completely safe?

No. AAA indicates strong assessed repayment capacity, not guaranteed repayment.

Is corporate FD interest taxable?

Yes. Interest is taxed according to the investor’s applicable slab.

Which FD should investors choose when Muthoot Capital offers 8.95% for 3 years?

Choose after comparing credit rating, liquidity, tax impact, and safer alternatives from established issuers first.

What is the best corporate fixed deposit in India for regular investors?

The best option combines competitive returns, strong ratings, flexible withdrawals, and reliable repayment history consistently.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article