By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

Main Points

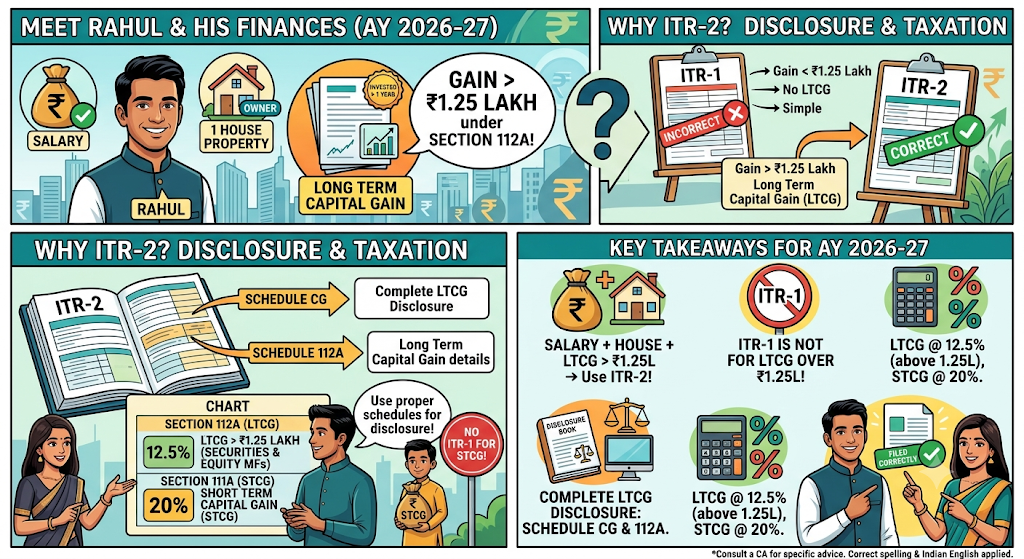

The ITR form filed for AY 2026-27 who earns salary income with owning 1 house property and having long term capital gain over ₹1.25 lakh under Section 112A will be ITR-2. It has been explicitly mentioned in the statement on the Income Tax Portal. The form ITR-1 can not be utilized in case of long term capital gain over ₹1.25 lakh. The complete LTCG would have to be disclosed in ITR-2 form by using Schedule CG and Schedule 112A.

Taxable LTCG under section 112A: flat 12.5% if you gain from securities & equity-based mutual fund is greater than 1.25 lakhs or if you invested for over a year. Taxable STCG under section 111A would be taxable at a flat rate of 20% . Note-You cannot file ITR-1 in case of STCG .

Around 38% of retail investors in India incurred losses on their equity investments in 2024 based on data provided by SEBI via LoansJagat. Even if they made profits, need to continue filing their taxes using form ITR-2, if either their LTCG exceeds ₹1.25 lakh or they have capital losses to carry forward. A salaried person who switched even 1 mutual fund scheme in FY 2025-26 has triggered a taxable event and cannot use ITR-1. The Annual Information Statement on the income tax portal already has this trade data pre-filled from CAMS and KFintech, so mismatches trigger notices.

Now you can hold as many as 2 house properties (used to be only 1 previously) under ITR-1 in AY 2026-27. For example, if you have salary income, 2 house properties, and exact 1.25 lakh long-term capital gain with no carried-forward loss, then you can continue to file ITR-1 for AY 2026-27. However, the moment it exceeds 1.25 lakh the entire long term capital gains are required to be filed in ITR-2 (not only the excess portion). If you still file ITR-1 with capital gain in excess of 1.25 lakh, you will get a notice for defective return under Section 139(9).

According to the official guideline by the Income Tax department a tax return is considered faulty if the wrong form has been used by the filer while filing ITR under the section 139(9). In AY 2026-27 ITR-2 form the Tax Garden information suggests that the AY 2026-27 ITR-2 form was published by CBDT on March 30, 2026, and a corrigendum was published on April 10, 2026. Failing to file it before July 31, 2026, means you lose your right to carry forward your capital losses for the coming 8 years.

The July 2026 ITR-2 from EbizFiling clearly states that one needs to compare their capital gain statement with their annual information statement as any variance is sure to attract a notice from the Income tax department. It would be important for taxpayers to know that as far as the assessment year 2026-27 is concerned, whether the capital gains has occurred prior to or after 23rd July 2024 is irrelevant, as the entire capital gains in respect of AY 2026-27 occurred after 23rd July 2024. So short term capital gains have been reduced to 20% which is being taxed under section 111A. Short term capital gains over 1.25 lakhs will be taxed under section 112A and will be taxed at a flat rate of 12.5%.

Step 1: Download the Capital Gains Statements

Go to camsonline.com or mfs.kfintech.com, select the period as FY 2025-26 (April 1, 2025 to March 31, 2026), and download the capital gains statement in excel format. At the same time, download the broker statement and reconcile both against your Annual Information Statement at incometax.gov.in.

Step 2: Login and Select ITR-2

Login to the website incometax.gov.in by using your PAN and password. Next, click on e-file, then select Assessment Year 2026-27 and ITR-2. You need to select AY 2026-27 carefully since this is the most frequent mistake made when filing capital gains for the first time.

Step 3: Fill up Schedule CG and Schedule 112A

Short-term and long-term gains should be entered separately in Schedule CG. For LTCG from equities, Schedule 112A needs scrip wise information: stocks/funds, cost, sale amount, number of units and date of sale. For shares acquired before February 1, 2018, you need to use the grandfathering provision: cost of acquisition will be the higher of actual cost or FMV on 31.01.2018 without exceeding sale consideration.

Step 4: Application of ₹1.25 Lakh Exemption and Setting off of Losses

Less ₹1.25 lakh from the total LTCG, after which the 12.5% taxation will apply. Short term capital losses can be set-off against short term and LTCG in the same fiscal year. However, LTCG losses can only be set-off against other LTCG in the same year. Both short term capital losses and LTCG losses can be carried forward up to eight years if the income tax return filing is done on time.

Step 5: Pay Self-Assessment Tax and E-Verify

If any tax is due after TDS and advance tax credits, pay self-assessment tax using Challan 280 before submitting the return. E-verify the return within 30 days using Aadhaar OTP, net banking, or EVC. An unverified return is treated as if it was never filed, making e-verification as important as filing itself.

For instance if a salaried taxpayer has section 112A LTCG income of more than Rs 1.25 Lakh for financial year 2026-27 irrespective of whether the taxpayer owns one house or two house he needs to file ITR-2. Deadline for filing ITR-2 for cases where no audit is required will be 31st July, 2026. Any amount of LTCG more than Rs 1.25 Lakh will be taxed at 12.5%. STCG will be taxed at 20%. The benefit of timely filing of appropriate ITR is that one will be eligible to set off his capital losses for 8 years.

What are the 3 most significant alterations in the new ITR forms applicable for AY 2026-27 that have a real impact on salaried tax payers?

The CBDT issued all the ITR forms for AY 2026-27 on March 30, 2026. The 3 important alterations include: Tax payers having not more than 2 house properties may file ITR-1 instead of ITR-2; fields related to earlier capital gain rate of 15% STCG & 10% LTCG have been eliminated in all forms; and ITR-3 deadline date for non audit professionals has been changed from July 31 to Aug 31, 2026.

My salary is below ₹12 lakh but equity capital gains push my total income above ₹12 lakh. Do I still get the Section 87A rebate on salary?

No. Section 87A is applied on total income, not income-head wise. Once your total income crosses ₹12 lakh, the full rebate is unavailable regardless of which income source pushed it over. Your entire tax liability is computed at applicable slab rates, including the portion attributable to salary income below ₹12 lakh.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article