By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Highlights

A few banks' first quarter business performance update revealed that the growth rate of loans outperformed the growth rate of deposits, as system credit expanded from 9.5% in June 2025 to 17.7% in May 2026.

However, the growth in deposits increased only to 12.2% in May 2026 and lags significantly behind the credit growth rate; this disparity is expected to continue in fiscal year 2027.

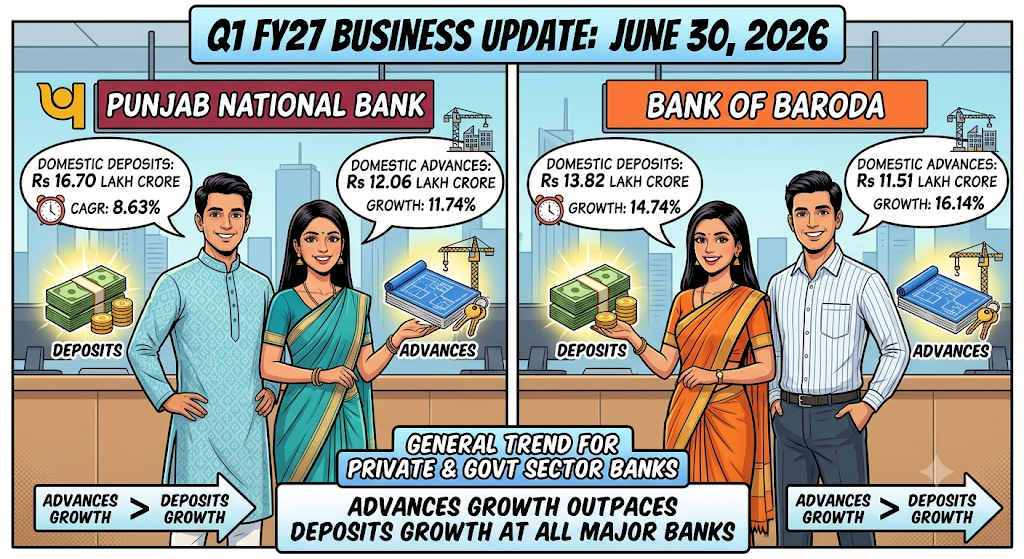

The figures of Q1 FY27 business update for June 30, 2026, show the same trend for both private and government sector banks. Growth in advances has been greater than growth in deposits at all major banks reporting their financial results.

Whereas, PNB's domestic deposits have grown with CAGR of 8.63 per cent with 16.70 lakh crore deposits and with the growth of 11.74 percent on its domestic advances to Rs 12.06 lakh crore as of 30th June 2026. Whereas, deposits with the Bank of Baroda stood with 14.74 per cent growth with Rs 13.82 lakh crore while its advances have grown with 16.14 percent with 11.51 lakh crore.

At J & K bank, with domestic advances showing a growth of 25.51 per cent with 1.31 lakh crore, its domestic deposits stood at 1.73 lakh crore with 16.75 per cent growth, meanwhile advances grew by 25.51 per cent. While advances with South Indian bank rose 17.01 percent with Rs 1.04 lakh crore, deposits grew 11.39 percent with Rs 1.26 lakh crore. Among other private banks, Tamilnad Mercantile bank’s advances registered a rise of 27.44 per cent, deposits grow 18.54 per cent.

On the whole, banking credit in India crossed Rs 2,04,75,000 crore with a record. At the system level, credit growth is 14.6 percent against deposit growth of 12.5 percent with 2,48,81,000 crore deposits as of January 31, 2026.

The gap between loan and deposit growth isn't new. It has been building since FY24, and it is getting harder for banks to close it. CareEdge Ratings expects credit growth of 13-14.5% in FY27, while deposit growth for scheduled commercial banks will moderate to around 11-12%.

The reason is straightforward. Household savings are moving away from low-yield bank accounts toward higher-return alternatives. Mutual funds, equities, small savings schemes, and direct stock market investing are all absorbing a growing share of Indian household surplus. Banks have also been cutting savings deposit rates to protect margins. This has made CASA accounts (current accounts and savings accounts) less attractive, pushing depositors toward term deposits or non-bank investment products. South Indian Bank, for example, saw CASA deposits grow only 14.61% to ₹41,493 crore, while advances grew at 17.01% over the same period. At IndusInd Bank, the CASA ratio has fallen below 30%, reflecting the systemic challenge in attracting low-cost savings amid high interest rates.

The West Asia conflict also added to the problem. Anand Rathi noted that wholesale deposit costs rose in May 2026 because of the war, though the RBI acted quickly to ensure sufficient system liquidity.

For ordinary borrowers, a persistent credit-deposit gap has a direct consequence. When banks can't raise deposits fast enough to fund loan books, they compete for funds by keeping rates high or borrowing wholesale at elevated costs. This pressure on bank margins makes lenders slower to pass on policy rate cuts to retail borrowers, a concern the RBI flagged formally in 2025. Even borrowers with repo-rate-linked home loans found that rate cuts don't reach them instantly, since loan reset cycles can delay transmission by 6 to 12 months depending on the lender.

The wider loan growth story also has a retail credit angle. LoansJagat notes that India's personal loan market hit ₹8.80 lakh crore in FY25, an 8.3% rise in loan volume from FY24, though total money borrowed actually fell by 2.9%, since borrowers moved toward smaller, shorter-tenure loans. With corporate loan demand now picking up strongly in FY27 alongside retail, banks are balancing both growth fronts simultaneously while managing the deposit shortfall.

There is a positive structural dimension here. YES Securities noted that credit growth has reached 17%, "driven by improved corporate loan growth and earlier improvement in MSME lending," which signals the growth isn't being driven by risky unsecured retail lending alone. PSBs are gaining market share in retail and MSME lending faster than private peers, partly because they entered the cycle with lower loan-to-deposit ratios.

Sanjay Agarwal, Senior Director at CareEdge Ratings, remarked: “The macro environment is favourable for the Indian banking sector as the economy is likely to see a growth of real GDP by 7.2% in FY27, coupled with an inflation rate sustained at 4%.” Thereby underpinning credit demand across retail, MSME, and corporate segments. However, he warned that elevated crude prices and supply chain disruptions from the Middle East conflict “may create short-term pressures on input costs and credit growth.”

Anand Rathi's analysis notes that the RBI's FCNR(B) push could lift deposit growth by 150-200 basis points and help sustain sector credit growth at 14-15% in FY27. The brokerage estimates aggregate FCNR flows of $40-60 billion, a move that would add 1.5-2% to deposit growth if successful.

On asset quality, YES Securities expects FY27 to be the last year in which pre-existing IRAC norms govern credit provisions, with the Expected Credit Loss framework taking over from FY28 without any material one-time shock. Banks with provisioning cover above 80% are seen as well-positioned to absorb any incremental NPA formation if El Nino or macro conditions worsen.

Anand Rathi's top banking picks include SBI (Target Price: ₹1,301), Bank of Baroda (₹329), ICICI Bank (₹1,716), and Axis Bank (₹1,610).

India's banking sector enters Q2 FY27 with credit momentum intact, system credit at a historic ₹20 lakh crore milestone, and loan growth running nearly 5-6 percentage points ahead of deposit growth. Whether the RBI's FCNR push can narrow this gap by 150-200 basis points before September 2026 is now the single most-watched variable for the banking sector's margin trajectory heading into FY28.

What are the 3 most important things to check before choosing a bank for a home loan in 2026?

Check the interest rate type first: fixed vs floating, since most banks offer floating rates starting at 7.10% p.a. Second, compare the processing fees, which range from 0.25% to 1% of the loan amount. Third, check prepayment penalty terms, since RBI's April 2026 rules ban prepayment charges on all floating-rate home loans.

Fiscal deficit in 2026, and is it at healthy levels or not?

The fiscal deficit of India for FY 2026-27 has been targeted to be 4.3% of GDP, which would come to ₹16.96 lakh crore. The country achieved its FY 2025-26 fiscal deficit of 4.4%, while the fiscal consolidation had been consistent in the wake of post-pandemic fiscal deficits of more than 9%. The optimal range for an emerging economy has been between 3%-4% of GDP.