By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

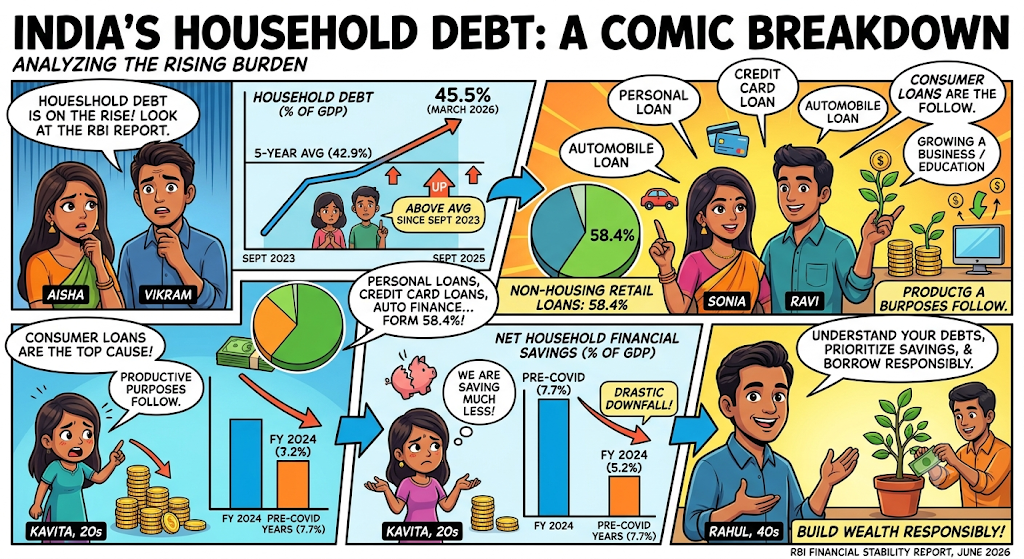

Household debt in India increased to 45.5% of GDP by March 2026, surpassing its 5-year average of 42.9%, as per the June 2026 Financial Stability Report of the RBI.

Non-Housing Retail Borrowings Comprise 58.4% of Household Borrowings and Continue to Increase Consistently.

India's household debt has reached 45.5% of GDP by September 2025 and March 2026, as mentioned in the Financial Stability Report of June 2026 published by the RBI. The 5-year average of this ratio has been 42.9%, and Indian household’s debts have been above this ratio since September 2023. The non-housing retail loans, which consist of personal loans, credit card loans, and automobile finance loans, contributed to the increase and formed 58.4% of the total debts of March 2026.

Consumer loans were the first reason for Indian household debts while loans taken for productive purposes followed. Net household financial savings have gone down drastically to 5.2% of GDP in FY 2024 from 7.7% in pre-COVID years.

An average Indian borrower avails himself or herself of a loan that is valued at Rs 4.8 lakh, which represents a rise from the Rs 3.9 lakh that was seen in the month of March 2023, representing a growth rate of 10.8 per cent for the year ending March 2025, as reported by LoansJagat. Almost half of the loans borrowed by sub-prime borrowers are used for consumption rather than asset generation.

On a more positive note, share of prime and higher rated borrowers, in both value of outstanding loan amounts and the number of accounts, has increased. Housing loans had become nearly default-free as their share fell to a paltry 0.5 per cent by March 2026 from 1.2 per cent in March 2019.

The RBI's June 2026 FSR stated that “global financial stability risks remain elevated” and that the retail loan segment needs close monitoring. The RBI also warned that risks to asset quality could increase, especially if the West Asia conflict weakens economic conditions and hits borrower cash flows. Gross NPA ratios in unsecured retail loans stood at 1.7% as of March 2026, a figure the RBI says must be watched carefully.

The RBI noted that India's sound macroeconomic fundamentals place it in a stronger position than many global peers to absorb shocks. Public sector banks hold a capital adequacy of around 16% and private banks around 18.1%, with gross NPAs near 2.1% as of September 2025. The RBI has already acted by raising risk weights on consumer credit in November 2023, which slowed unsecured loan growth across banks and NBFCs.

The current level of household debt at 45.5% of India's GDP is not yet at crisis level, but it is a red alert. And given that non-housing retail loans constitute 58.4% of household debt, and savings have shrunk to a mere 5.2% of the GDP, Indian households can't afford to borrow without a plan. Checking their credit score, comparing loan interest rates and ensuring they have not taken too many loans should be the 3 most useful steps for any individual in 2026.

What made India's household debt rise to 45.5% of GDP in September 2025 as per the latest RBI report?

The rise was due to non-housing retail loans which accounted for 58.4% of total household loans as of March 2026, always outperforming housing, agriculture, and business loans. The consumption loans account for most household loans, whereas loans for asset creation have been growing very slowly.

Is India's household debt dangerous, and what is driving its continuous rise each year?

In 2024, India's household debt was at 42% of GDP, an increase from only 26% in 2015, where the average debt per person increased by 23% in two years, from ₹3.9 lakh in 2023 to ₹4.8 lakh in March 2025. Digital loans, easy approvals, and aggressive marketing campaigns are the main causes.