By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

By March 2026, Indian households borrowed ₹118.6 lakh crore, and consumption increased. This exemplifies the quick, EMI-led consumption and the rise of repayment exercises over various income groups.

Key Highlights

India’s consumption-loan portfolio reached ₹118.6 lakh crore in March 2026, rising 15.3% in 1 year, according to CRIF High Mark’s How India Lends, May 2026 report. The rise shows how loans are now linked to regular buying, not only homes, cars or business needs. Personal loans, consumer durable finance, credit cards and two-wheeler loans are carrying a larger share of household spending.

The shift affects borrowers in 2 ways. In the short term, a family can buy a phone, fridge, laptop or scooter without paying the full price at once. Over time, repeated small EMIs can reduce monthly room for rent, groceries, school fees and medical needs. That is where the risk begins. A loan may look affordable alone, but 5 loans together can hurt a household budget.

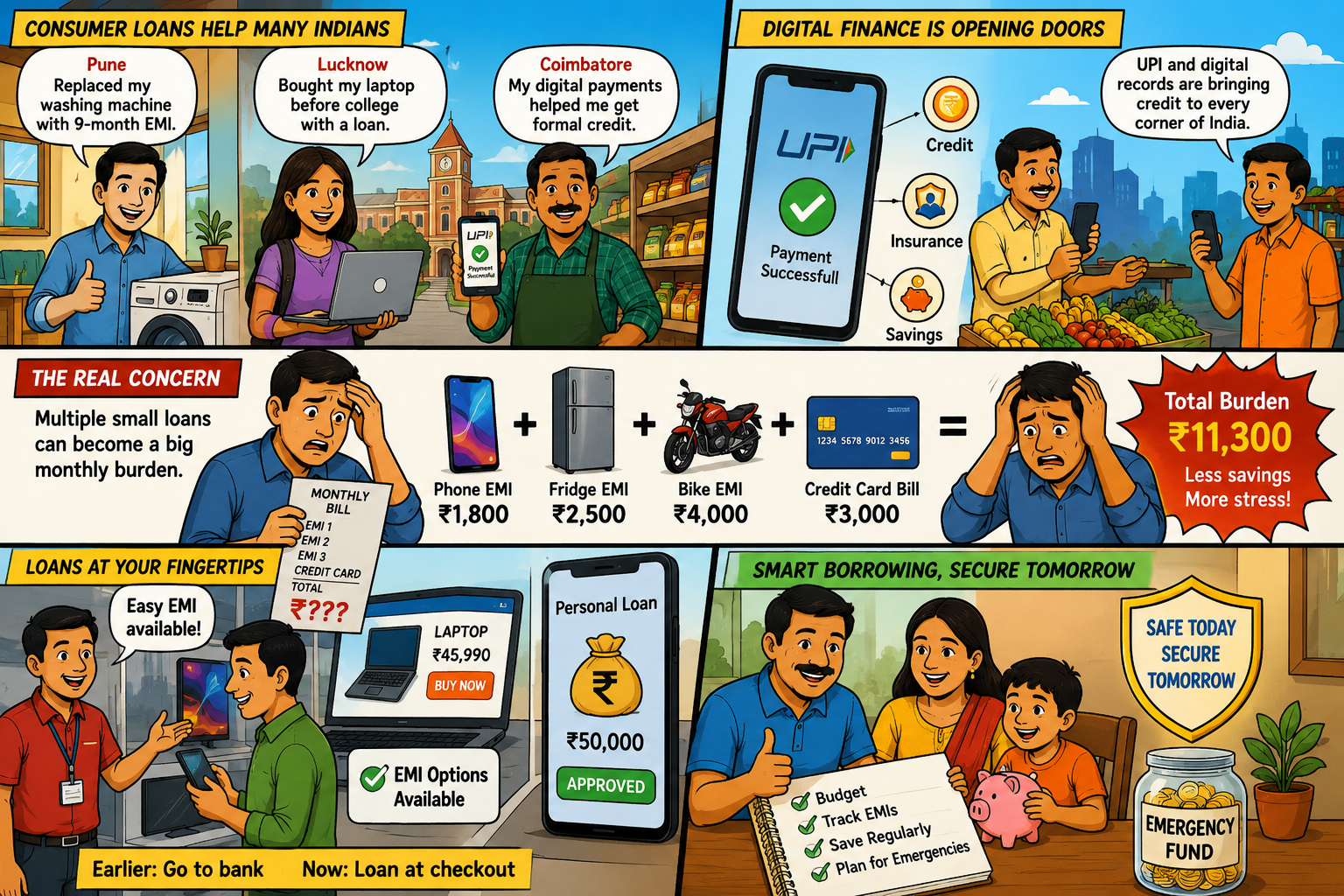

Consumer loans are helping many Indians buy products sooner. A salaried buyer in Pune can replace a broken washing machine through a 9-month EMI. A student in Lucknow can buy a laptop before college begins. A small shop owner in Coimbatore can use digital payment history to access formal credit. For such borrowers, credit can support daily life when used with care.

Government data also shows why lenders are reaching deeper into India. The Press Information Bureau said on 11 April 2026 that UPI had opened access to formal finance for millions and created new routes to credit, insurance and savings for small merchants and informal workers. Faster payments, digital records and app-based checks have made lending easier outside large cities, too.

The concern is not 1 planned loan. The concern is repeated borrowing. A buyer may accept ₹1,800 as a phone EMI, ₹2,500 for a fridge, ₹4,000 for a bike and a credit card bill at month-end. Each payment looks small. Together, they can reduce savings and force another loan during an emergency.

That habit is spreading because credit now appears during the purchase itself. Earlier, a borrower went to a bank. Now the loan arrives at checkout. Retail counters, online carts and mobile apps offer EMI options before the buyer has fully compared the cash price.

The rise in consumer loans is part of a wider credit shift. Formal lending is growing, digital payments are creating borrower records, and repayment planning has become more important for households managing more than 1 EMI.

After this rise, lenders and borrowers have different pressures. Lenders want growth from personal loans and consumer durable finance. Borrowers want quick approval and a lower upfront cost. The gap appears when income does not rise as fast as monthly repayment commitments.

The answer starts with access. Digital payments have created transaction records for people who earlier had limited formal credit history. Lenders can now examine bank statements, UPI inflows, salary credits and repayment behaviour faster. That has reduced friction for many borrowers.

The second reason is price. Phones, appliances, school devices and travel costs have become harder to pay in 1 shot for many families. EMI finance breaks the bill into monthly parts. Retailers like it because it improves sales. Lenders like it because small loans create repeat customers. Consumers like it because they do not need to wait.

CRIF High Mark’s report showed personal loans at ₹16.5 lakh crore in March 2026. Consumer durable loans reached ₹1 lakh crore and grew 20.8% year-on-year. These are not abstract banking figures. They point to real purchase behaviour inside homes, shops and online marketplaces.

Still, not every personal loan is shopping debt. Some borrowers use personal loans for hospital expenses, weddings, education fees, rent deposits or older loan repayment. That distinction is important. The ₹118.6 lakh crore figure signals rising consumption-linked borrowing, but it does not mean the full amount was spent on luxury buying.

Credit advisers usually ask borrowers to do 3 checks before accepting a fresh EMI. First, add all existing EMIs. Second, check the final payable amount, including processing charges, GST, insurance and penalties. Third, keep emergency cash for at least a few months of basic expenses.

The solution is not to avoid every loan. A useful loan can help a household buy something needed. The problem starts when the borrower takes credit because approval is easy, not because repayment is comfortable. That line is thin. Many people cross it during festive sales, phone upgrades or urgent family expenses.

LoansJagat’s repayment guide, dated 5 January 2026, recommended a simple route for borrowers handling multiple loans. Close high-interest debt first, use part-prepayment where charges allow, and keep a fixed repayment plan instead of paying randomly. This helps borrowers see the full loan burden before it becomes stressful.

Lenders also need stronger checks. A credit score alone may not show a recent salary cut, informal borrowing or new app loans. Retailers should show the cash price and EMI-linked price separately. If a discount disappears after choosing finance, the buyer should know it before signing.

Before the March 2026 loan figure, official data had already shown strong credit activity in the Indian economy. The Department of Economic Affairs said in its Monthly Economic Review, April 2026, that bank credit grew 17.1% year-on-year as of 31 March 2026. That growth came while domestic demand stayed active and financial conditions supported lending.

Digital finance also laid the base for wider credit access. The PIB note of 11 April 2026 said UPI had moved beyond payments and helped small merchants and informal workers build routes to credit, insurance and savings. That matters because many new borrowers now enter finance through payment records, not branch paperwork.

The broader change is visible at the street level. A vegetable vendor accepting UPI, a salaried employee with a pre-approved app loan and a shopkeeper offering no-cost EMI are all part of the same shift. Credit is becoming easier to access and easier to spend.

The risk for borrowers often starts with small numbers. A phone EMI looks manageable. A credit card conversion feels lighter than paying the full bill. A two-wheeler loan may look necessary for daily travel. Taken alone, none of them may look worrying.

According to LoansJagat, the trouble begins when several repayments run together in the same month. For example, a ₹1,500 appliance EMI, a ₹3,000 credit card conversion, a ₹4,500 two-wheeler loan and a ₹6,000 personal loan add up to ₹15,000. For a household earning ₹45,000, that is 1-third of the income before rent, groceries, school fees, fuel and medicines.

Borrowers need to check the full monthly outgo before accepting another loan. The final payable amount matters more than the EMI shown on a product page. Processing fees, GST, insurance, and late charges can push up the real cost.

A safer purchase leaves room for an emergency. If a 1 hospital visit, salary delay, or school payment can disturb the budget, the loan may need to wait. Easy approval should not become the reason to borrow.

India’s ₹118.6 lakh crore consumption-loan portfolio shows how deeply credit has entered everyday buying. It has helped consumers access goods faster and brought more people into formal finance.

The warning is simple. Easy credit should not replace budgeting. A useful EMI can help a family. Too many small loans can reduce monthly breathing room and push borrowers towards fresh debt. The next stage of India’s credit story will depend on how carefully lenders approve loans and how honestly borrowers count their repayments before buying.

What happened to the consumer loans market in India?

India’s consumer loan market grew 15.3% YoY to ₹118.6 lakh crore in March 2026.

What’s the jump in consumer loans in India attributed to?

Consumers are availing loans via EMIs to purchase consumer electronics, household goods, and two-wheelers and to fund vacations, education and medical bills.

Are all personal loans available to shop?

No, medical bills, weddings, education, rent, and refinancing also contribute to the personal loans taken.

What’s the best way to avoid EMI stress?

Borrowers should total all EMIs, consider the total payable amount, and prepay the most costly loans first.