India's Credit Card Economy Just Hit Rs 23.6 Trillion. Debit Cards Are Fading Out.

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Insights

- According to the RBI's Payment Systems Report, credit card transactions in India grew in number and value by two times and almost three times, respectively, from 2019 to 2024.

- Number increased from 2,087 million to 4,472 million transactions, while the total value increased from ₹7.1 trillion to ₹20.4 trillion.

- Number decreased from 4,953 million in 2019 to 1,738 million in 2024, and value decreased from ₹6.83 trillion to ₹5.15 trillion due to the dominance of UPI for low-value routine payments.

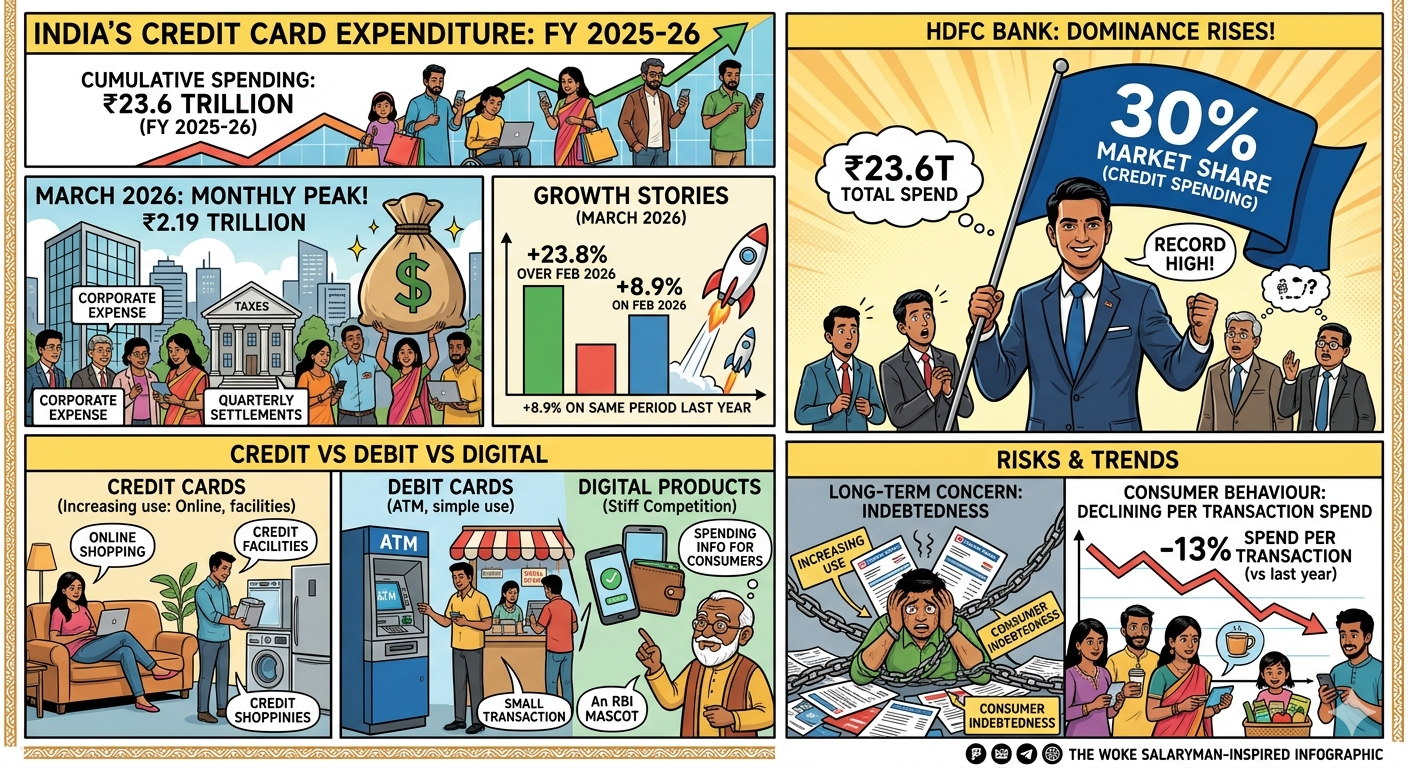

India Is Swiping More, and the Numbers Say So Clearly

The cumulative credit card expenditure in India was ₹23.6 trillion during FY 2025-26.

The expenditure stood at ₹2.19 trillion owing to end-of-year corporate expenditure, payment towards taxes, and quarterly settlements during March 2026.

This was a 23.8% increase over February 2026, although there was an increase of only 8.9% on the same period last year.

HDFC Bank extended its dominance as its market share rose to a record 30% of total credit card spending, which is the highest ever in recent years.

The RBI said that although credit cards are increasingly used for online shopping and credit facilities, debit cards are commonly used for ATM transactions and other simple transactions.

Both cards have been facing stiff competition from digital products. Short-term benefits are seen as better fee earnings for banks and spending information for consumers.

In the long run, the increasing use of credit cards will pose additional risks of consumer indebtedness.

On average, spending per transaction declined 13% compared to last year, implying that consumers are doing more transactions involving lower amounts.

Five Years of Credit Card Growth vs Debit Card Decline

The table below highlights the evolution of credit and debit card usage in India over the past five years, illustrating the significant structural change in consumer payment behaviour.

Read More - Credit Card Spending Moderated 8%

The private sector banks have gained a market share of 70.8% for credit cards, compared to 65.8% in 2020.

Their dominance in digitised and co-branded credit cards, whereas the public and foreign banks have fallen behind.

What India's Credit Card Boom Means for Everyday Users

The credit card revolution for millions of Indian consumers has a double edge. Increased availability of credit is factual and helpful.

As per RBI regulations effective from April 2026, all digital payments, including credit card payments, would need two-factor authentication at the very least.

Transactions using a credit card exceeding ₹10 lakhs in a year would be compulsorily reported to the Income Tax Department under the Statement of Financial Transactions.

Some major banks have reduced rewards and lounge benefits offered with mid-range credit cards due to profitability issues.

This might dampen the enthusiasm of prudent consumers for using cards.

However, credit cards associated with UPI are providing increased reach to areas where traditional credit cards never reached, such as grocery stores, petrol pumps, and small stores.

Analysts Point to Growing Card Stress and a Shifting Market

Unsecured retail segments like credit cards had been growing at an annual rate of 25% between FY21 and FY24.

However, by May 2025, growth had slowed down to 8.5% on a year-on-year basis because of increased stress and reduced demand.

The slowdown in growth can be attributed to not only the maturity of the market but also the emergence of repayment issues among some cardholders.

As of April 2026, credit reports shall reflect all payment information, whether made on time or missed within seven to fourteen days, as compared to earlier, longer periods.

Also Read - Credit Card Spends Rise 13.57% in FY26

The new system of credit reporting would ensure that late payments attract quicker punishments.

For customers who utilise credit cards frequently, on-time payments are no longer just responsible behaviour; they impact their credit ratings much faster now.

Conclusion

The Indian credit card industry is developing very quickly, with transaction volume already crossing ₹23.6 trillion by FY26. While growth is certainly real and widespread, the pressure on borrowers and the faster credit reporting system make responsible credit card use more critical than ever before.

FAQs

Credit card usage in India. Would this be beneficial for the Indian economy?

Increasing credit card usage in India would be both positive and negative for the economy. Although it will help increase short-term GDP and ensure financial inclusion, it will have negative effects on macroeconomic stability because of increasing household debt and NPAs.

What do you think about the Indian economy?

The Indian economy is among the most rapidly growing economies in the world, and it is characterized by high macroeconomic stability, high public capital expenditure, and a nominal GDP of more than ($4) trillion.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article