RBI Removes IFR Reserve Rule: Will Banks Now Give More Loans?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- The RBI has officially withdrawn the Investment Fluctuation Reserve (IFR) requirement for commercial banks with effect from May 18, 2026. Banks can now move their IFR balance to core capital reserves.

- Earlier, banks were required to set aside a portion of profits as IFR to cover losses from falling bond prices. The RBI first proposed this removal in April 2026 after inviting public comments.

RBI Scraps IFR Rule: What does it mean for your Bank’s Strength?

The Reserve Bank of India (RBI) officially removed the Investment Fluctuation Reserve (IFR) rule for commercial banks on May 18, 2026. Banks no longer need to keep a separate buffer against losses from falling investment values.

This is a long-term positive step. It boosts banks’ core capital and simplifies compliance.

However, in the short term, there is a risk. Banks face more exposure during sharp bond market swings without a dedicated buffer. Investment losses will hit earnings more directly if interest rates rise suddenly.

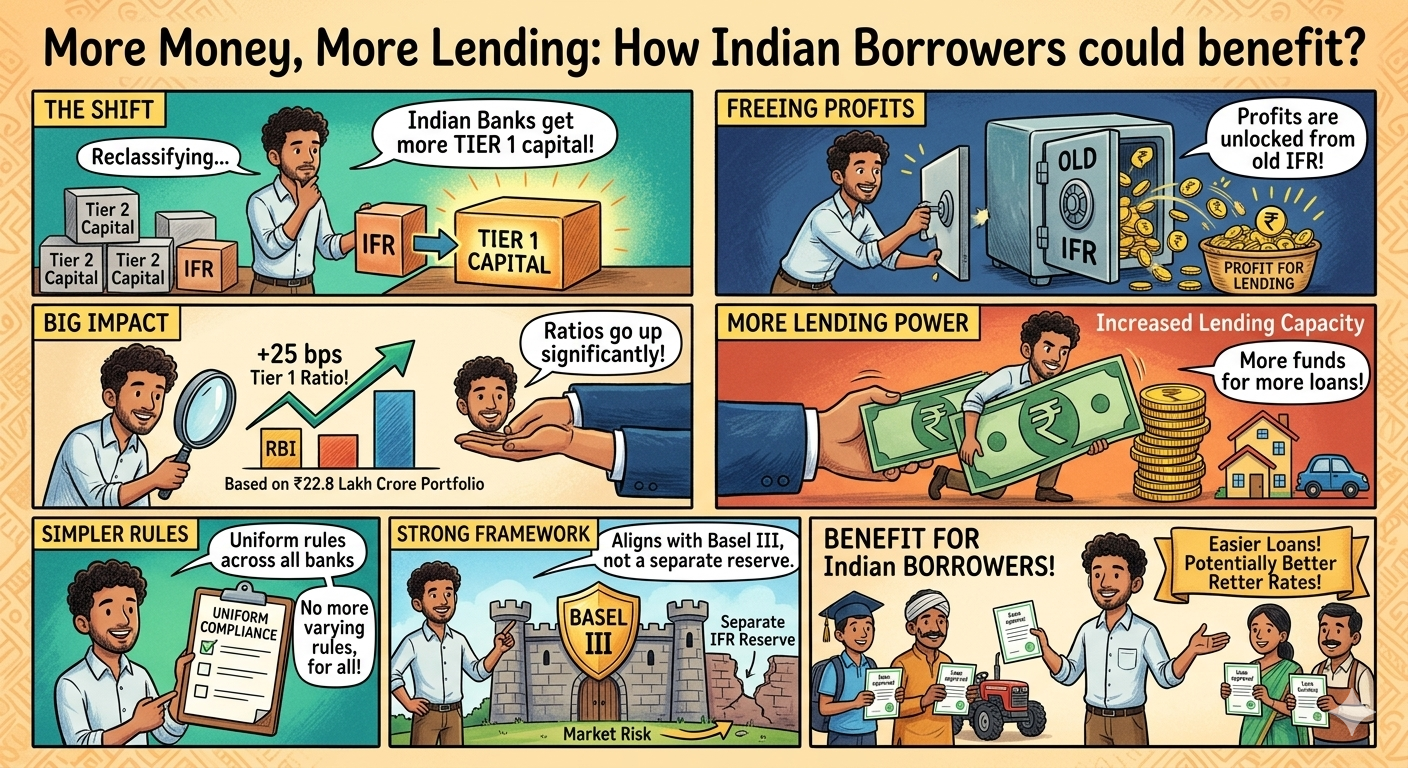

More Money, More Lending: How Indian Borrowers could benefit?

Banks can now reclassify existing IFR amounts into Tier 1 capital. This is the highest-quality capital a bank holds. Previously, IFR was counted as Tier 2 capital.

The shifting it to Tier 1 could raise core capital ratios by nearly 25 basis points across the banking sector, according to RBI estimates based on the system’s ₹22.8 lakh crore FVTPL portfolio as of September 2025.

The added capital cushion would strengthen banks’ lending capacity, potentially improving credit availability for retail customers and small businesses. It also gives banks the flexibility to pay better dividends to shareholders.

Experts Back the Move, But Urge Caution on Volatility

Experts see this as a smart cleanup of an outdated rule. RBI Governor Sanjay Malhotra explained that mark-to-market valuation already reflects the true financial position of banks. The need for a separate fluctuation reserve reduces if investments are valued at market prices.

RBI Deputy Governor Swaminathan J added that IFR had a “checkered history.” It was introduced, then removed, then reintroduced. Compliance levels also varied across banks. Removing it makes the framework simpler and more consistent.

On the impact, Suresh Ganapathy, Head of Financial Services Research at Macquarie Capital, said the capital boost from reversing IFR would be around 20 to 30 basis points for most banks. He added that banks are unlikely to reverse the full balance and may simply stop making fresh IFR contributions each year.

Anil Gupta, Senior VP at ICRA, noted that the increase in Tier 1 capital will not have a material positive impact on overall capital ratios, given that most banks already maintain strong capital buffers.

Conclusion

The RBI’s removal of the IFR rule is a welcome step toward cleaner, simpler banking regulations. It frees up capital, removes compliance burdens, and aligns India with global banking norms. India’s well-capitalised banks are well-placed to manage it while the risk of bond market volatility remains. This move signals that the RBI trusts the existing Basel III framework to handle market risk going forward.

FAQs

Did RBI remove the IFR reserve because banks already have enough capital buffers?

Yes, the RBI believes Indian banks are already well-capitalised under Basel III rules. The RBI felt a separate IFR reserve was no longer necessary since banks now mark investments to market prices regularly.

Why did it allow the IFR safety buffer to be removed if RBI regulates banks?

The RBI removed the IFR rule to simplify banking regulations and free up extra capital for lending. Banks will now rely on existing Basel III capital norms to manage investment-related risks instead of a separate reserve.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article