By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

In 2025, the RBI lowered its repo rate four times from 6.50% to 5.25%. However, this year, the RBI chose to retain the same amount of reduction in its repo rate of 125 basis points.

FD rates offered by banks have reduced by 30 to 70 basis points since February 2025.

The Repo Rate was cut by the Reserve Bank of India 4 times during the year 2025. The repo rate came down from 6.50% in February to 5.25% in December. SBI provides the highest interest rate through his schemen “Amrit Vrishti.” But SBI decreased its 7.1% to 6.6%. Similarly, the HDFC Bank FD rate declined from 7.25% to 6.6%. As per the research conducted by SBI, the FD interest rates offered by various banks have fallen by 30 to 70 basis points from February 2025 due to four successive rate cuts.

FD offering an interest rate of 8.5% in 2015 is now giving around 6.9%. With a 30% tax deduction, FD return falls way below the inflation level for the investor. Major public sector banks are offering a fixed deposit rate of 6.4% to 6.6% in a tenure of 1 to 2 years as on September 2025.

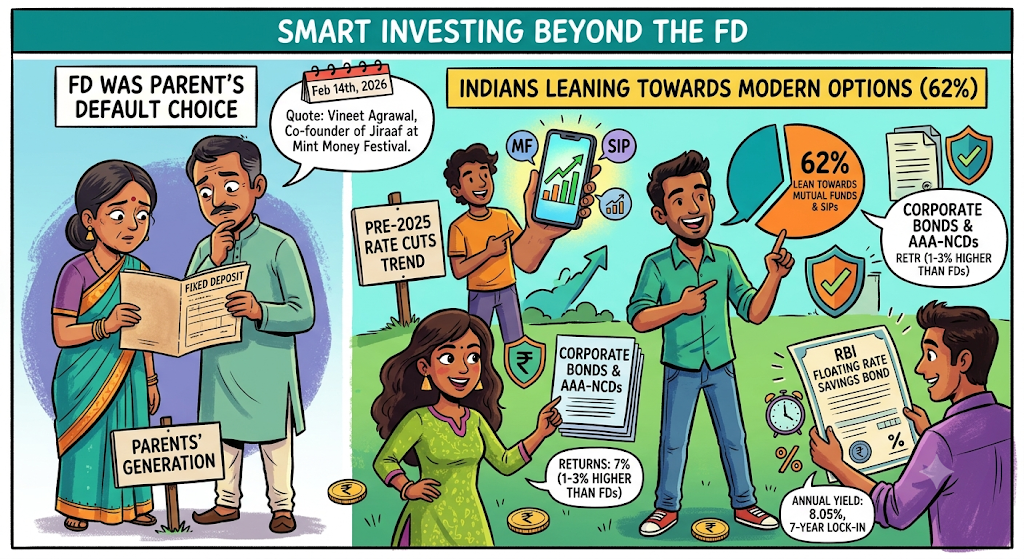

Based on LoansJagat's analysis of fixed deposit and investments, Indians were already leaning towards mutual funds and SIPs over fixed deposits even before the rate cuts of 2025, with 62%. Returns from corporate bonds and AAA rated NCDs are between 7% and 10%, which is 1 to 3 percentage points higher than FDs for the same tenor. RBI Floating Rate Savings Bond provides annual yield at 8.05% with 7 year lock-in period.

In terms of taxation, interest earned from the bond investment, which is over 24 months duration, will be taxed at 12.5% Long Term Capital Gain tax rate, while FD interest is taxed at full slab rate. "FD was the default choice for our parent's generation," stated Vineet Agrawal, Co-founder of Jiraaf at Mint Money Festival, on 14th Feb, 2026.

Adhil Shetty, CEO of BankBazaar, told BusinessToday on December 6, 2025: "Banks have reduced rates across nearly all tenures, with the sharpest cuts in the 1 to 2-year bucket. High-yield FDs have become rare, and another easing cycle will drag peak rates even lower." Ankur Jalan, CEO of Golden Growth Fund, stated that "a 25-basis-point cut raises clear concerns about shrinking returns on fixed-income products".

Shetty advised that senior citizens should lock in longer FD tenures now and can still avail 25 to 50 basis points above standard rates. For general investors, Jiraaf recommends a core-and-satellite strategy, keeping stable FDs for capital protection while allocating a portion to corporate bonds or government securities for yield enhancement. A laddering approach across 3, 5, and 7-year instruments can also reduce reinvestment risk in a falling rate environment.

The RBI's 125 basis point rate cut cycle across 4 moves in 2025 has made FDs a weaker standalone option for wealth creation. SBI and HDFC FD provide you with almost 6.6% return, but at the same time bonds give you 7% to 10% return on your investment. That means bonds give you a good amount of return if compared with the FD.

I have ₹30 lakhs at my disposal for investment purposes. How can I allocate money sensibly?

Allocation of ₹30 lakhs in a sensible way would include allocating ₹9 lakhs in large-cap/ index funds, ₹6 lakhs in mid-cap funds, ₹6 lakhs in debt funds or government securities, ₹6 lakhs in fixed deposit and ₹3 lakhs in gold ETFs. This should be evaluated every 12 months without panic selling during corrections.

How should I invest my ₹3 crores to ensure that my need of ₹1 lakh per month gets satisfied for the next 50 years?

This is the right way to invest; 50% of investments should be in equity mutual funds, 30% in debt funds like bonds and PPF, 10% in REITs and dividend stocks, and 10% in gold ETFs.