By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

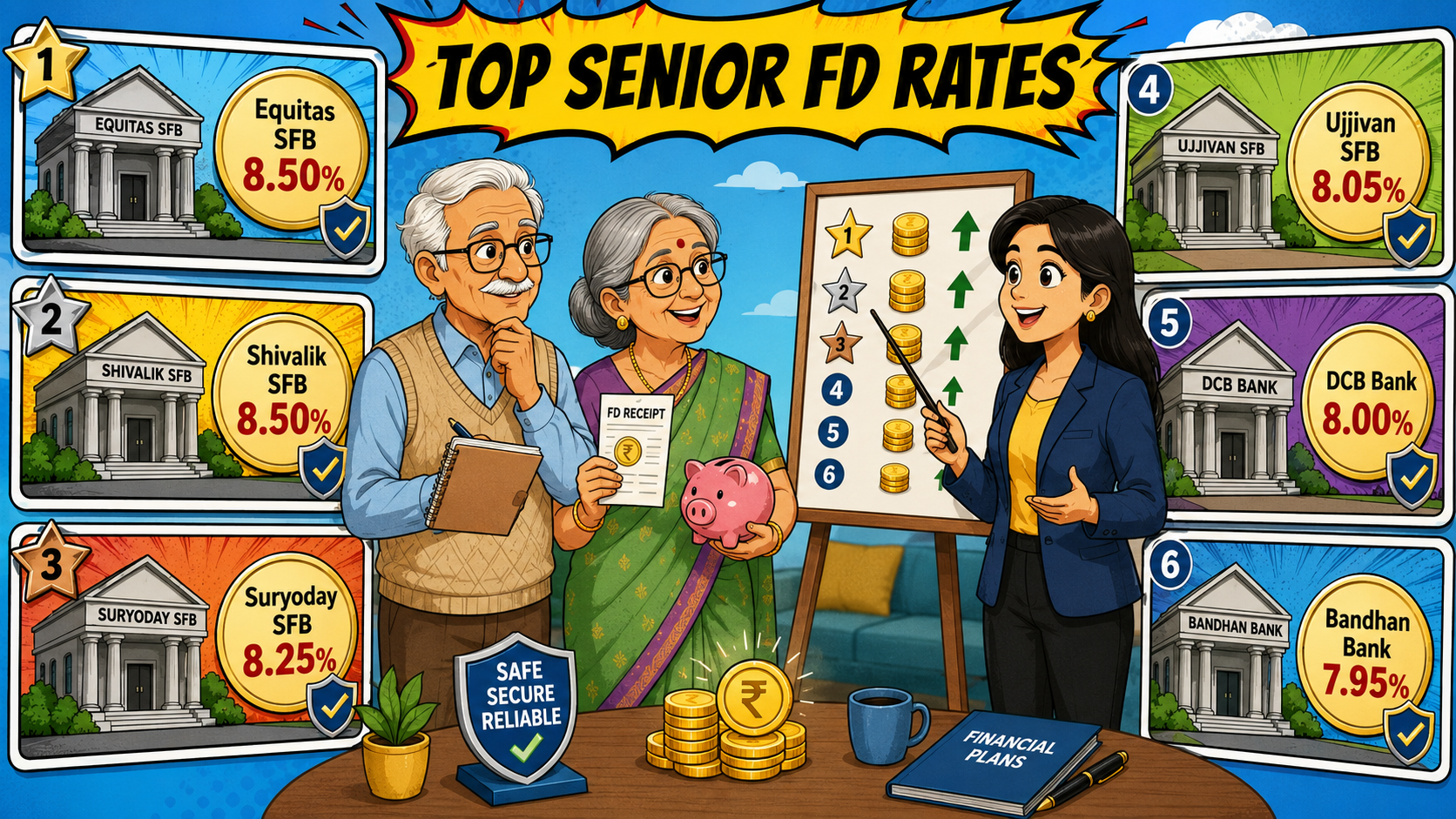

For senior citizens checking fixed deposits before the end of June, banks still offer rates above the 8% mark. The highest current rate is 8.50%, though that is for select deposit tenures.

Key Highlights

A Moneycontrol survey dated June 20, 2026, had Equitas and Shivalik Small Finance Bank at 8.50%, Suryoday at 8.25% and Utkarsh at the same rate.

Those small numbers can help pay bills for dying family members, electricity or insure them. But for funds that may be needed in six months, getting the highest rate possible does not make sense.

Small finance banks held most of the top positions during June. DCB Bank was among the few regular private banks offering 8%.

Bandhan Bank’s revised rates became effective on June 20, 2026. Its 7.95% senior citizen rate applies to deposits running from 2 years to less than 3 years.

A customer asking for a 1-year FD should not expect the same figure. The rate changes with the tenure chosen.

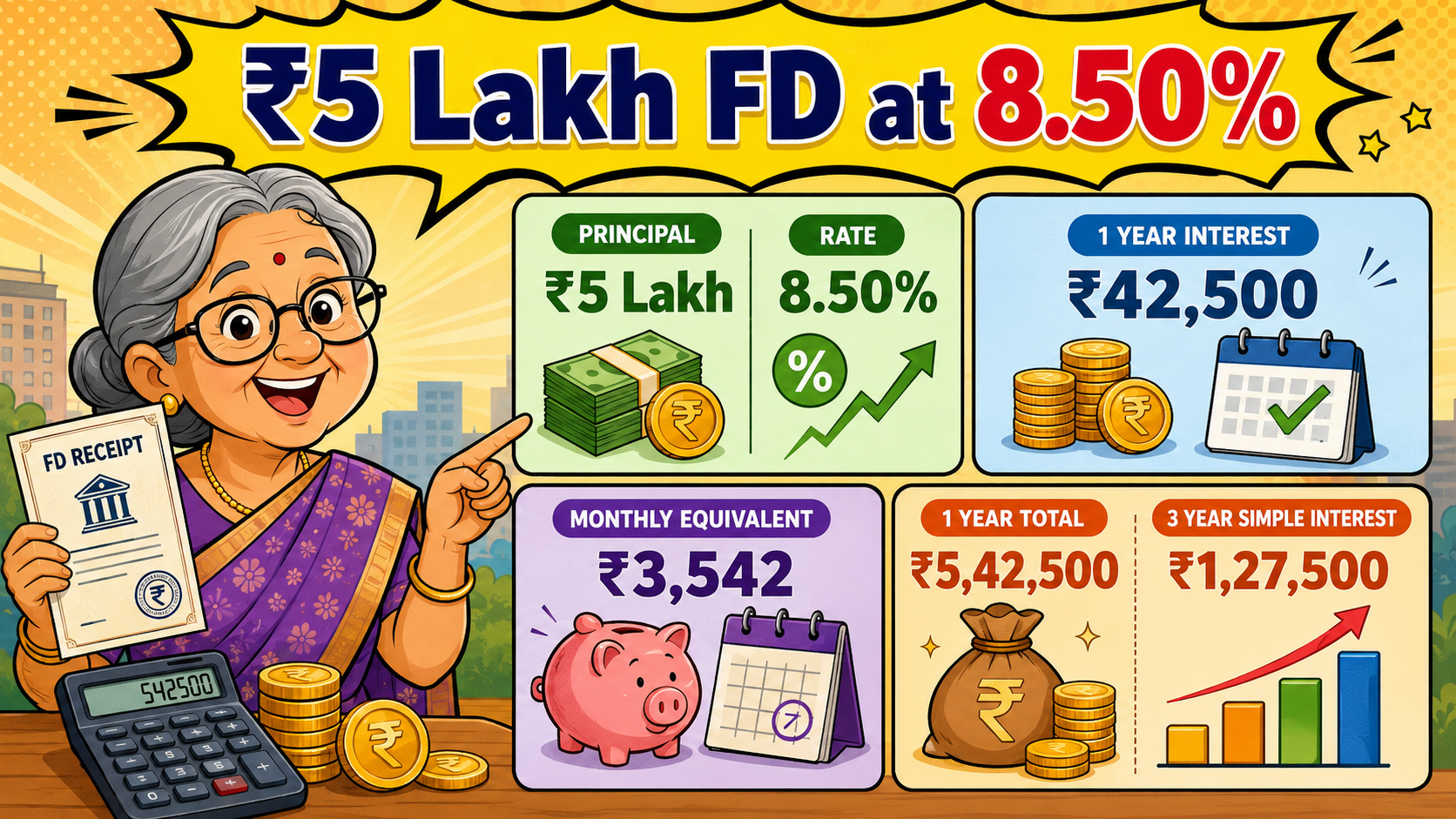

A ₹5 lakh deposit at 8.50% earns ₹42,500 in 1 year before tax, based on a simple annual calculation. At 7%, the same deposit earns ₹35,000. The difference comes to ₹7,500.

For one household, that may cover several electricity bills. For another, it could pay part of a medical insurance renewal.

The monthly value is only an illustration. Banks may credit a slightly lower amount under monthly payout plans because of the way they calculate interest. In a cumulative FD, the interest remains invested until maturity.

Rates looked different during the first half of June.

A LoansJagat report dated June 8, 2026 placed Shivalik Small Finance Bank at 8.30%. ESAF and Suryoday were listed at 8.25%.

A Mint comparison published on June 14 also showed 8.30% as the top rate at that stage.

By June 20, Moneycontrol’s list showed offers reaching 8.50%. This is why depositors should not rely on an old screenshot or forwarded message. Banks can revise one deposit slab without changing every tenure.

For ₹5 lakh, the gap between 8.30% and 8.50% equals ₹1,000 over 1 year before tax.

Tenure comes first. Suppose a retiree has ₹6 lakh reserved for an operation next year. Locking all of it into a 3-year FD for an extra 0.25% could backfire if early closure later reduces the rate.

Withdrawal penalties vary. Some banks lower the applicable interest rate, while others impose a separate penalty. Customers should read the official terms before transferring money.

The LoansJagat comparison also advised depositors to compare tenure, withdrawal terms and payout options instead of ranking banks only by the highest advertised rate.

Monthly interest may suit retirees using the money for regular expenses. A cumulative deposit may work better when immediate income is not required.

The DICGC guide covers eligible deposits up to ₹5 lakh per depositor per insured bank. This limit includes principal and interest.

Placing ₹5 lakh as principal does not mean the complete maturity value stays covered. Interest can push the balance above the insured limit.

A person with ₹10 lakh may divide the money between 2 insured banks. Deposits held in the same name and capacity at one bank are added together for insurance purposes.

Senior citizen FD rates touched 8.50% at selected lenders during June 2026. Several banks also offered rates of 8% or more.

Before booking, check the exact tenure, withdrawal penalty, payout method, tax effect and DICGC-covered amount. A slightly lower rate may work better when easier access to the deposit is required.

Does Every Senior Citizen Receive The Highest Rate?

No. The highest rate normally applies only to one selected deposit tenure.

Is Senior Citizen FD Interest Tax-Free?

No. FD interest remains taxable, though eligible depositors may submit Form 15H.

Are Small Finance Bank FDs Insured?

Yes. Eligible deposits receive DICGC cover up to ₹5 lakh per depositor per bank.

Should Retirees Pick Small Finance Banks Only For Higher Rates?

No. They should also check insurance limits, withdrawal charges, tenure and branch access.

Is An 8.75% FD Better Than A Mutual Fund?

An FD offers fixed returns. Mutual funds carry market risk and may suit longer investment periods.

₹41,250