Kanika Bali of The Tax Planet Lays Out Saving Goals for People in Their 30s, 40s, and 50s

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

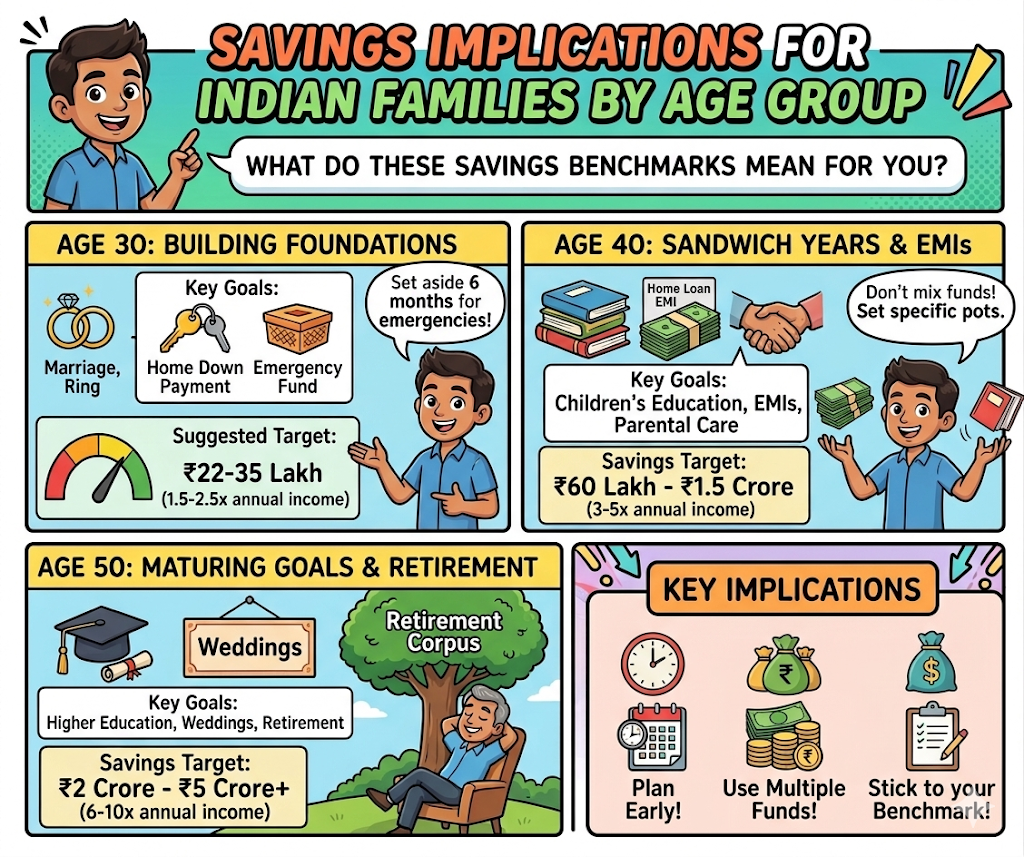

- Kanika Bali, founder of The Tax Planet, states that people in India should aim to save 1.5 to 10 times their yearly income by the ages of 30, 40, and 50, respectively.

- This is to achieve the goals of marriage, housing loans, funding children’s education, medical care for parents, and retirement savings of middle-class Indians.

How Many Indian People Should Save by the Age of 30, 40, and 50?

Kanika Bali, who is the founder of The Tax Planet, revealed savings targets at different ages for the people of India on June 10, 2025, to Hindustan Times.

According to her, there were savings targets that varied from ₹22 lakh to ₹35 lakh at 30 and ₹5 crore or more at 50, respectively. This was based on an income of ₹12 lakh to ₹15 lakh per annum.

According to data collected by LoansJagat, 58% of the applicants for home loans were between the ages of 28 and 35. This means that most young Indians make a huge financial commitment even before having enough savings.

Medical bills, fees for children, and expenses due to living in cities are only increasing. Hence, there’s hardly a chance for Indians to make adequate savings without planning.

What are the Implications of these Saving Benchmarks for Different Age Group Indian Families?

These savings benchmarks are well aligned with the actual financial challenges that Indians face at various age groups. These include the following:

Consider someone in his or her 30s earning ₹14 lakh per annum. For such a person, the savings benchmark will be ₹21 lakh to ₹35 lakh. Emergency funds for six months and health insurance are essential at this age, according to Kanika Bali.

The age of 40 brings all types of bills together. From school fees, home loan EMIs, to taking care of parents. People who do not set up different funds start borrowing from one fund to pay the other. As per Bali, most people find themselves with issues related to reskilling and require money now more than ever before.

What do the experts have to say about preparation for retirement and mid-life savings?

“Age fifty is the point when financial responsibilities rise. This is due to children getting educated, marriages, and high expenses for health care facilities,” said Bali in Hindustan Times. The expert suggests that large loans should ideally be settled before starting to save for retirement.

According to a recent Max Life Insurance report in 2024, just 24% of Indians have plans regarding retirement. This is especially true for salaried professionals as they tend to prioritise their children’s education over their own retirement savings.

According to most advisors, 50% of your money should go on your basic needs, while 30% on goals, and 20% should be saved by the age of 25 to achieve these figures at the age of 50.

Conclusion

The retirement savings milestones mentioned by Bali help Indian families save in an easy, numerical way. It ranges from ₹22 lakhs at the age of 30 years to ₹5 crores by the time you hit 50. Start saving earlier and make lower monthly payments to get each milestone.

FAQs

How much savings do I need at age 30, 40, and 50 in India?

You should have savings between ₹22 lakh and ₹35 lakh at age 30, ₹60 lakh and ₹1.5 crore at age 40, and ₹2 crore to ₹5 crore at age 50, assuming annual income is ₹12 lakh to ₹15 lakh.

How much of my salary do I need to save and invest in India every month?

The advice of most financial experts is that one should follow the 50-30-20 rule. It is where 50% salary must be spent on necessities, 30% on goals, and 20% be saved/invested each month. If you start from age 25, you will be able to achieve your goal of saving ₹2 crore to ₹5 crore at age 50.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article