By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Key Takeaways

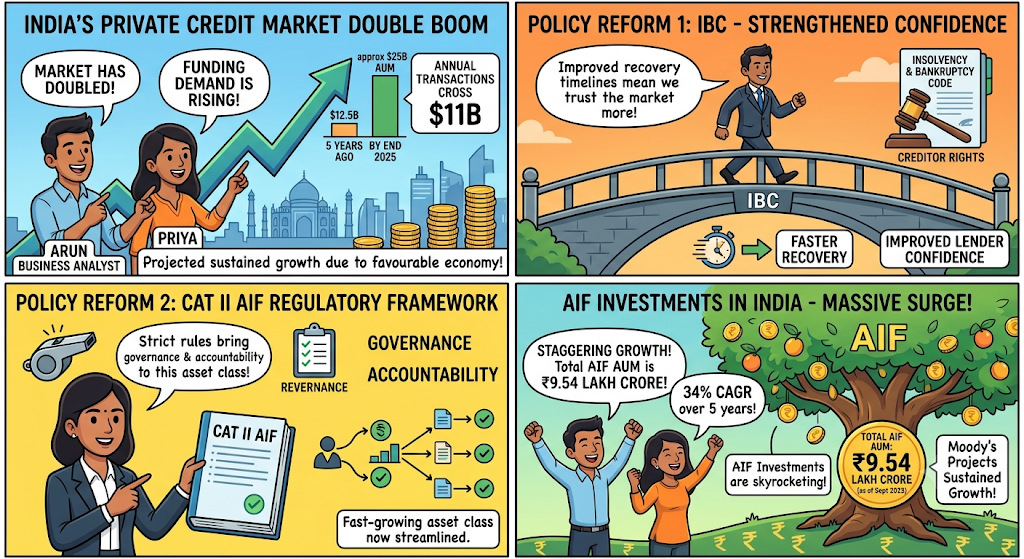

Moody's Ratings published a report projecting sustained growth for India's private credit market, driven by rising funding demand and a favourable economic backdrop. The market has doubled in size over the past 5 years to approximately $25 billion in AUM by the end of 2025, while annual transaction value has already crossed $11 billion.

Moody's highlighted 2 key policy reforms that have strengthened lender confidence in the market. First, the implementation of the Insolvency and Bankruptcy Code has improved creditor rights and recovery timelines. Second, the Category II AIF regulatory framework has brought governance and accountability to a fast-growing asset class. AIF investments in India have grown at a

Moody's expects private credit to grow by filling the gaps that banks and NBFCs cannot address. Both lenders face regulatory constraints on long-tenure, large-ticket or complex structured financing, making private credit a natural fit for mid-market corporates, real estate developers, and infrastructure companies. India's corporate bond market, at just 18-20% of GDP, remains far smaller than comparable economies, leaving a wide financing gap.

For smaller businesses, the formal credit access gap remains large. LoansJagat notes that in 2025, over ₹32,60,000 crore worth of collateral-free loans were disbursed across India under government-backed and NBFC schemes. Yet formal credit still reaches only a fraction of MSMEs, especially in sectors like real estate, infrastructure, and manufacturing, where private credit funds are now stepping in with structured, flexible solutions that banks cannot offer.

Globally, Moody's projects private credit AUM will approach $4 trillion by 2030, driven by ABF lending, M&A activity, and bank-private credit partnerships. Kotak MF analysts note the market “is still at an early stage of penetration rather than a mature, crowded segment,” making structural growth more durable than cyclical.

The RBI has already ring-fenced bank exposure to private credit AIFs under its AIF Investment Directions, effective January 2026, capping individual regulated entity investment at 10% of any AIF scheme's corpus and collective exposure at 20%. This keeps systemic risk low even as the market grows, making India's private credit expansion structurally sounder than what played out in the US, where banks have committed approximately

India's private credit market doubling to $25 billion in 5 years is just the beginning, given its current penetration of just 0.6% of GDP. With IBC, strong AIF regulation, and rising corporate funding demand all pointing the same way, this market is positioned to grow significantly through the rest of the decade.

This statement cannot be considered entirely accurate. According to the head of Moody’s global private credit Marc Pinto, this saying was used by him on October 17, 2025, following the market downturn caused by the loan defaults of mid-sized US banks. Although high yield default rate is below 5%, UBS estimates it to increase to 13% in 2026 due to the AI disruption.

Moody’s has not yet upgraded India’s rating. India's credit rating of Baa3 has been maintained with a stable outlook as recently as September 29, 2025, due to high public debt and low debt sustainability of the country. As per IMF estimates, India’s GDP growth is forecasted at 6.2% in 2026 while Moody’s estimates it to be 6.4%.