By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Senior citizens without health insurance can claim medical expenses under Section 80D, but the old tax regime and proper proof are required.

Key Highlights

As per the Income Tax Department, senior citizens without any health insurance can still claim an exemption up to ₹50,000 for medical expenses under Section 80D of the Income Tax Act. This provision applies when the person is a resident senior citizen at the age of 60 years and, in that year, the health insurance premium is not paid for that person.

The benefit can reduce taxable income for pensioners, salaried children paying parents’ bills, and families handling hospital costs without an insurance policy. The short-term gain comes during ITR filing. The long-term result may be better record-keeping. The negative side is harsh. A real hospital bill may still fail if the taxpayer selects the new tax regime, pays without proper proof, or claims a bill for someone who already has health insurance.

Section 80D outlines a hierarchy of tax deductions pertaining to health insurance and health-related expenses. In cases where senior citizens don’t have health insurance, the deduction law permits the reimbursement of health expenses to ₹50,000. It is worth noting that this is not a reimbursement of ₹50,000. Rather, it reduces taxable income, and the net tax saving will depend on which slab the taxpayer falls into.

Consider the following example. Let’s assume a 68-year-old retired individual has paid ₹64,000 to a hospital and has health insurance. The individual would be able to claim a deduction of ₹50,000 under Section 80D, assuming the individual is a pensioner and the claim is made under the old tax system. However, in the event that the individual opts for the new tax system, the Section 80D claim would not be applicable.

The rule can help 2 common groups. First, senior citizens who pay their own medical bills from pension, savings, rent, or interest income. Second, adult children who pay medical bills for senior citizen parents. Many Indian families fall into the second group, especially where parents do not have active medical claim cover.

The LoansJagat Section 80D guide also explains that taxpayers can claim higher deductions when senior citizen parents are covered under Section 80D. For uninsured senior citizens, the medical bill angle becomes useful because there may be no premium receipt at all. In such cases, hospital bills, pharmacy invoices, diagnostic reports, and bank payment records carry more weight.

For the masses in India, this rule gives relief in cases where insurance is absent. Senior citizens often face high premiums, disease-based exclusions, co-payment clauses, or lapsed policies. Some families do not buy health insurance at all because annual premiums look too costly when monthly expenses are already tight.

The positive side is that genuine medical spending gets some tax recognition. A salaried person in Delhi paying for a parent’s cataract surgery, a pensioner in Kochi paying for cardiac tests, or a son in Pune paying diagnostic bills for his father can all look at this rule. The claim will still depend on documents, tax regime, and eligibility.

The table below gives the filing check in one place. It should be used before submitting ITR, not after a notice or mismatch.

The Income Tax e-Filing Portal states that Chapter VI-A deductions such as Section 80D are not available under the new tax regime, except specified deductions such as Section 80CCD(2), Section 80CCH, and Section 80JJAA. This is the filing step where many taxpayers lose an otherwise valid claim.

The previous policy change came via Budget 2018. As reported on 1st February 2018, by the Press Information Bureau, the limit for senior citizens under Section 80D was increased from ₹30,000 to ₹50,000 concerning the health insurance premium or medical expenses.

This recent claim for filing was based on the recent tax regime. Effective AY 2024-25, the new tax regime shall be the default approach for the ITR process. Taxpayers still have the option to retain the previous tax regime in eligible cases, but they would have to choose this option at the time of filing. That one click may decide whether the medical expense deduction of ₹50,000 is applicable or not.

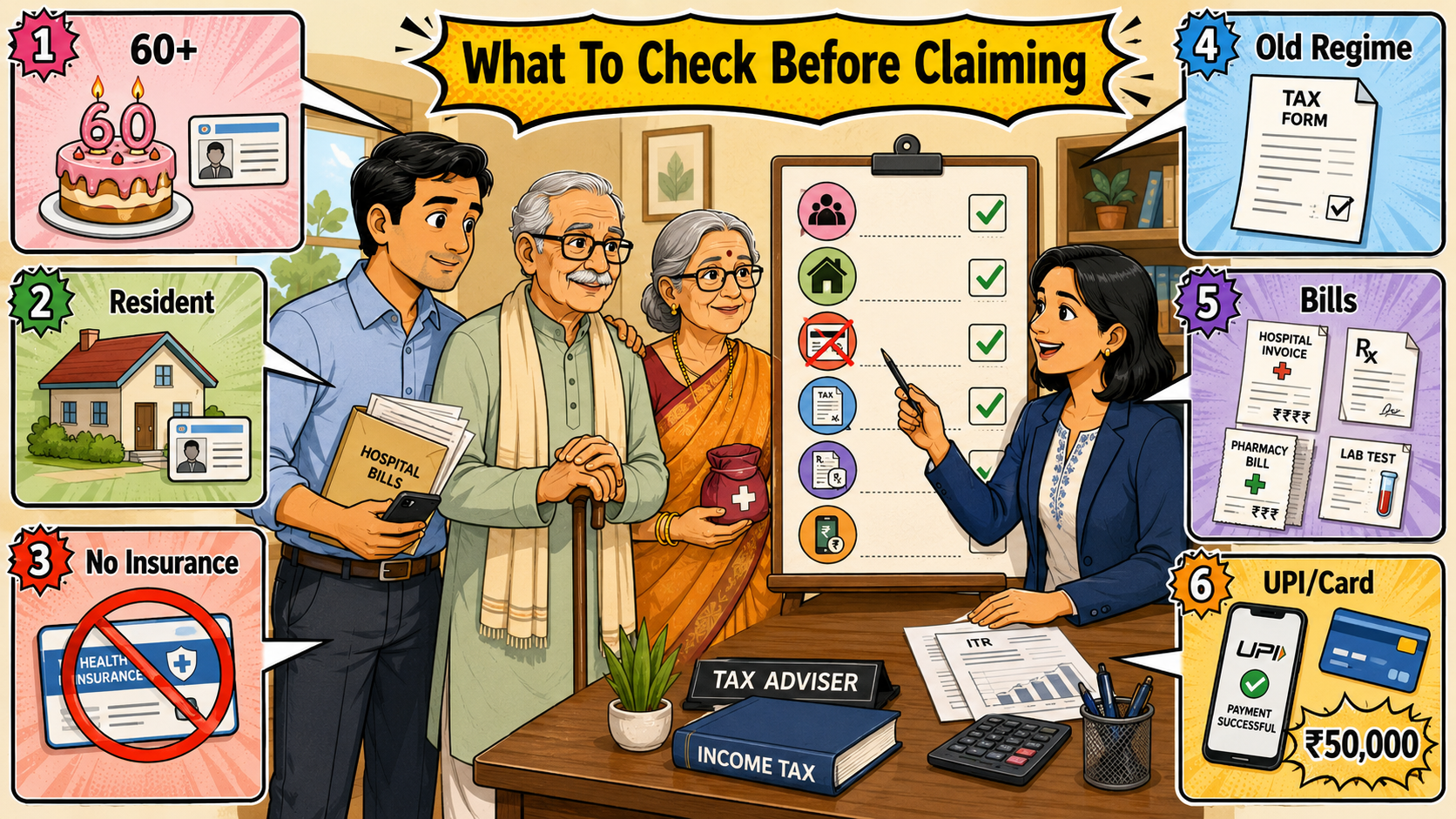

Tax experts usually look for 3 items before treating the claim as safe. The senior citizen should be a resident and aged 60 years or above. The taxpayer should confirm that no health insurance premium was paid for that senior citizen. The medical expense should have bills and payment proof.

The solution is plain paperwork. Families should keep doctor prescriptions, hospital bills, pharmacy invoices, diagnostic receipts, payment screenshots, bank entries, and the senior citizen’s age proof. A short note in the tax file saying “no health insurance premium paid for this person during the year” can also help during future checks.

The biggest trap is not the ₹50,000 limit. It is the difference between health insurance premiums and medical expenditures. If a senior citizen has no policy, there will be no premium receipt. That does not block the claim. The medical bill becomes the main document.

Another common mistake is treating the deduction as automatic. It is not. The taxpayer must choose the old tax regime and enter the Section 80D claim correctly. A person with low taxable income may see little or no tax benefit even with valid bills. A person in a higher slab may get a better saving, but only within the legal cap.

The Income Tax Department says medical expenditure for a senior citizen can be claimed under Section 80D when no amount has been paid to buy or keep health insurance active for that person. The same department also defines a senior citizen as a resident individual aged 60 years or more during the relevant previous year.

The Income Tax e-Filing Portal gives the filing warning. It says Chapter VI-A deductions are not available under the new tax regime, except for the deductions specifically permitted under Section 115BAC. That directly affects Section 80D claims.

The Press Information Bureau gave the policy background in its February 1, 2018, budget note. It said the deduction limit for senior citizens under Section 80D was raised from ₹30,000 to ₹50,000.

Senior citizens without health insurance can still use Section 80D for medical expenses up to ₹50,000. The rule can help families that pay elderly medical bills without any insurance cover, but it needs careful filing.

The taxpayer must check 3 things before submission. The senior citizen should qualify by age and residency; no health insurance premium should have been paid for that person, and the old tax regime should be selected. Without these checks, even a genuine medical bill may not reduce taxes.

Can senior citizens without health insurance claim Section 80D?

Yes. They can claim eligible medical expenses up to ₹50,000 under the old tax regime.

Is this ₹50,000 a direct refund?

No. It is a deduction from taxable income, not a direct payment from the government.

Can children claim medical bills paid for senior citizen parents?

Yes. They can claim eligible expenses for uninsured senior citizen parents under Section 80D.

Which tax deductions apart from Section 80C can help with medical costs?

Taxpayers can check Section 80D, Section 80DD, and Section 80DDB under the old tax regime. Section 80D covers health insurance, preventive check-ups, and eligible senior citizen medical bills. Section 80DD and Section 80DDB apply only in specific disability or disease cases, with conditions attached.

Can an assessee claim both health insurance premiums and medical expenses under Section 80D?

Not for the same insured person in the usual case. Section 80D allows health insurance premium deduction. Medical expenditure is allowed for a senior citizen only when no health insurance premium has been paid for that person. A preventive check-up can still be counted within the overall Section 80D limit.