NPS Rules Changed: Why Your Retirement Savings Could Grow Faster Now?

Check Your Loan Eligibility Now

By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Key Takeaways

- India’s NPS has revised its fee structure, withdrawal rules, and introduced healthcare linkage to improve cost efficiency and long-term retirement planning.

- Earlier, PoP charges were transaction-based, incentivising volume over growth. The new AUM-linked fee model aligns distributor goals with investor outcomes.

NPS Just Got Cheaper and Smarter: Here’s Why It Matters

India’s National Pension System (NPS) is getting a meaningful structural overhaul. The changes touch fees, withdrawals, and even healthcare linkage.

These reforms won’t transform NPS overnight. But for long-term retirement savers, especially in the private sector, even small cost reductions compound significantly over decades.

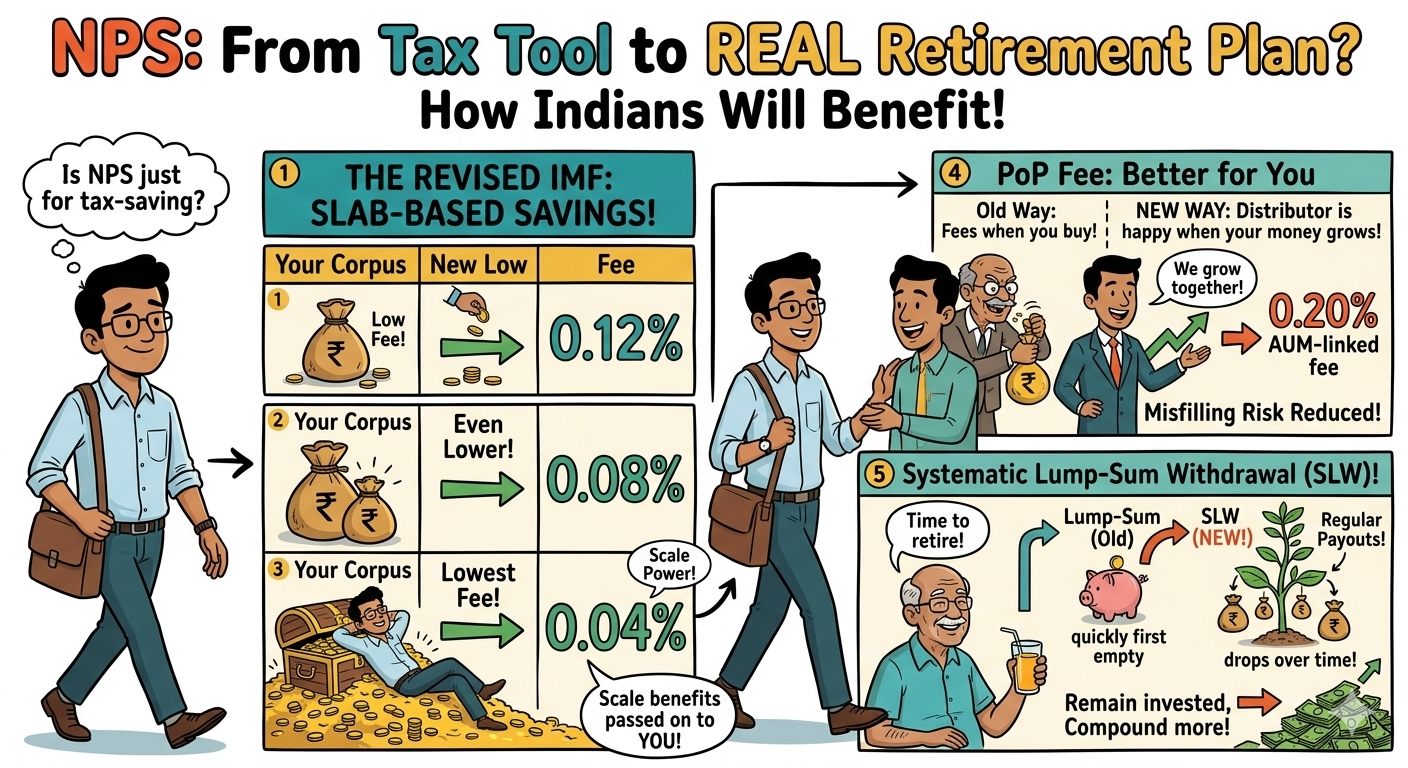

From Tax Tool to Real Retirement Plan: How Indians Will Benefit?

The most impactful change is the revised Investment Management Fee (IMF). It now follows a slab-based structure:

Rajeev Gupta, Head of Third Party Products and eGovernance at Religare Broking, noted that “the revision does not change NPS’s underlying structure. It improves cost efficiency and ensures economies of scale are passed on to subscribers.”

The PoP fee also shifts from transaction-based to 0.20% AUM-linked annually. This means distributors now earn more when your corpus grows, not just when you transact. That directly reduces mis-selling risk.

The new Systematic Lump-Sum Withdrawal (SLW) option lets retirees withdraw in phases. Your remaining corpus stays invested and keeps compounding. This is a practical tool for managing post-retirement cash flow.

Experts Speak: Transparency Builds Trust, But Watch the Gaps

Jyoti Prakash Gadia, Managing Director at Resurgent India, said, “Improved transparency and structured charge frameworks are important for building trust in pension products, especially among private sector and self-employed investors.”

He also pointed out that NPS has long been seen mainly as a tax-saving instrument under Section 80C and 80CCD. Clearer cost structures could help reposition it as a genuine retirement vehicle.

On the healthcare front, the NPS Swasthya initiative links retirement savings with medical expenses. Experts call it a useful but early-stage experiment. Gupta noted it “recognises healthcare costs as a key retirement risk but should be seen as complementary to health insurance, not a substitute.”

Gadia added that structured withdrawal options and financial counselling at the exit stage are necessary. Without guidance, retirees may still make poor decisions despite having flexible tools.

One concern is that long lock-in periods make adoption sensitive to any ambiguity around costs or returns. The reforms address this partially, but more investor education is still needed.

Conclusion

NPS is not being reinvented. It is being refined. Lower fees, better-aligned distributor incentives, phased withdrawal options, and early healthcare integration are all steps in the right direction. These changes quietly improve the deal for salaried professionals and self-employed individuals building a retirement corpus. The key is to stay invested long enough to feel the difference.

FAQs

Are the new NPS changes making retirement planning more flexible in India?

Yes, the latest NPS reforms have made retirement planning more flexible. The new phased withdrawal option, lower charges, and healthcare linkage give investors better control over their retirement savings and post-retirement expenses.

Is NPS now a better long-term retirement investment after the new updates?

NPS has become more attractive for long-term investors due to lower fees and improved withdrawal options. It remains a low-cost retirement product that can help salaried and self-employed individuals build a retirement corpus over time.

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Subscribe Now

Related Blog Post

India's #1 Loan Consolidation Platform

Simplify All Your Loans Into One Affordable EMI

10 Lac

Customers Served

₹2000 Cr+

Debt Consolidated

4.7★

1200+ Reviews

10,000+

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article