By continuing, you agree to LoansJagat's Credit Report Terms of Use, Terms and Conditions, Privacy Policy, and authorize contact via Call, SMS, Email, or WhatsApp

Disclaimer: The information published on LoansJagat is intended for general informational and educational purposes only and should not be considered financial, legal, or investment advice. Interest rates, loan terms, statistics, and other data may change over time and may vary by lender or source. Please verify the latest information and consult a qualified financial advisor or the respective Bank/NBFC before making any financial decisions.

Subscribe Now

About the author

LoansJagat Team

Contributor‘Simplify Finance for Everyone.’ This is the common goal of our team, as we try to explain any topic with relatable examples. From personal to business finance, managing EMIs to becoming debt-free, we do extensive research on each and every parameter, so you don’t have to. Scroll up and have a look at what 15+ years of experience in the BFSI sector looks like.

Related Blog Post

Simplify All Your Loans Into One Affordable EMI

Customers Served

Debt Consolidated

1200+ Reviews

Locations in India

Club all Loans & Credit Card Bills into Single EMI

Quick Apply Loan

Consolidate your debts into one easy EMI.

Takes less than 2 minutes. No paperwork.

10 Lakhs+

Trusted Customers

2000 Cr+

Loans Disbursed

4.7/5

Google Reviews

20+

Banks & NBFCs Offers

Other services mentioned in this article

Millions of UK graduates are repaying their student loans through payroll, but interest keeps pushing most Plan 2 balances in the wrong direction.

Key Highlights

Data from The Times on June 29, 2026, cites that only 6% of Plan 2 students managed to decrease their balance. According to data, approximately 4.4 million borrowers gained debt from when their repayment period started in May 2026.

That does not mean they skipped payments. Many have paid every month through their salary. The trouble is fairly basic: the interest added during the year can be far higher than the amount deducted. For graduates trying to save for rent deposits, a house or family costs, a rising statement can be hard to ignore.

Plan 2 borrowers repay 9% of income above £29,385, as stated in HM Revenue and Customs guidance. The payment changes with salary. The size of the debt does not decide the monthly deduction.

Take a graduate earning £40,000. The yearly repayment works out at roughly £955. Interest of 6% on a £50,000 balance adds about £3,000. Even after the payroll deductions, the balance could rise by around £2,045.

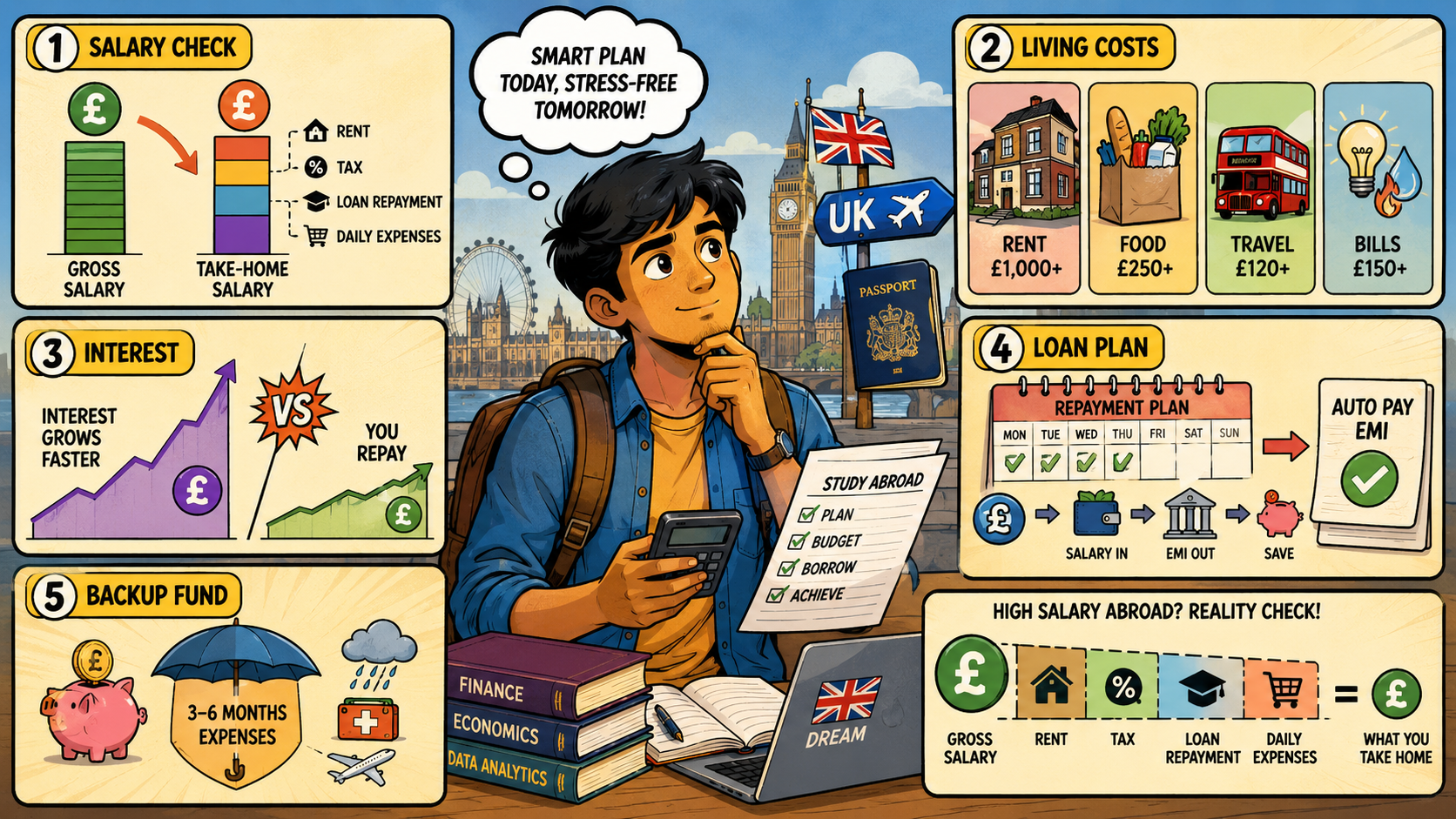

Plan 2 rules do not apply to a standard Indian education loan. Even so, the figures are useful for Indian students considering a UK degree. A large salary figure in pounds can look reassuring before rent, tax, visa charges and interest enter the calculation.

The House of Commons Library reported in June 2026 that borrowers who completed their courses in 2023 owed an average of £47,900 when they entered repayment in April 2026.

According to LoansJagat, an overseas loan should be tested against a modest first salary, not the best campus-placement number. Students should also include moratorium interest and at least 3 months without work. This LoansJagat education loan guide explains the checks families can run before signing.

The government announced on April 7, 2026 that Plan 2 and Plan 3 interest would be capped at 6% from September 1, 2026. The Guardian, Sky News and ITV News covered the decision.

Rethink Repayment campaigner Oliver Gardner welcomed the cap but argued that it did not settle the wider problem. The Institute for Fiscal Studies said the immediate benefit would largely reach higher earners who faced the top interest rate.

The latest figures expose a rough outcome: payment does not always mean progress on a Plan 2 loan. The 6% cap reduces the top rate, but millions may still watch their balances rise.

How much do borrowers repay?

They pay 9% of earnings above the £29,385 annual threshold through payroll deductions.

Why does the balance rise after payment?

The interest added can exceed the total amount deducted from the borrower’s salary.

Should graduates pay extra?

Extra payment may help some high earners. Others may pay more than necessary before the loan is written off.

Should a plan 2 borrower pay off the loan or keep saving for a house?

For many borrowers, saving for a house deposit may come first because Plan 2 repayments depend on income. Extra payments only help when the borrower is likely to clear the loan before write-off.

Why do many plan 2 graduates still owe so much after years of repayments?

Interest can grow faster than compulsory deductions. A graduate may repay every month, yet the balance still rises because payments are based on salary, not on the total debt.

£29,385

About £955